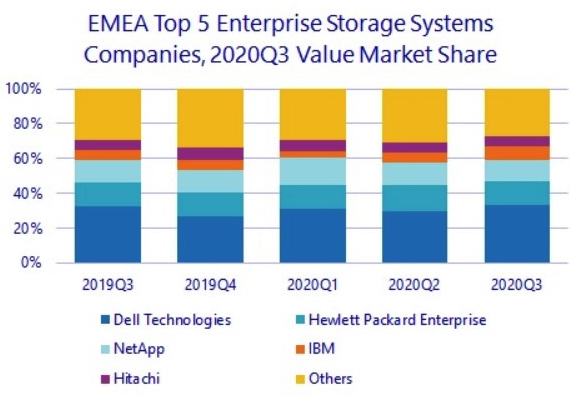

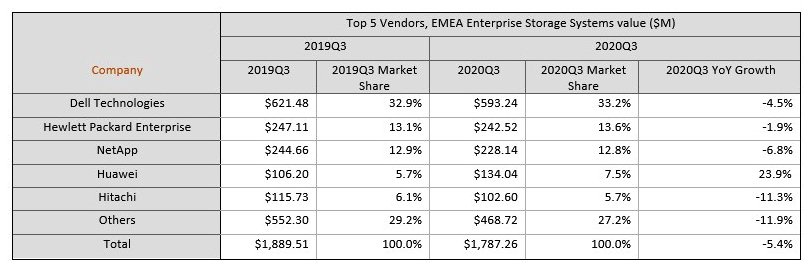

EMEA External Storage Market Down 5% Y/Y in 3Q20

But +8% for AFAs with 45% of global market share up from 39% Y/Y, all biggest companies down but Huawei

This is a Press Release edited by StorageNewsletter.com on January 7, 2021 at 2:18 pmThe EMEA external storage systems market was down 5,4% Y/Y in dollars and 10% in euros in 2020Q3, according to IDC Corp.‘s EMEA Quarterly Disk Storage Systems Tracker.

Once again, the quarter saw marked differences across subregions, with Western Europe down 8,3% Y/Y and CEMA up 2,3% (both in dollars).

On a brighter note, the AFA segment remained resilient at a positive 7.9% Y/Y, bringing its share of external storage market value to 44,7%, up from 39,2% in the same quarter a year ago. This increase was at the expense of both hybrid flash arrays and HDD-only arrays, both down by about 14% Y/Y.

“Softness in investments and budget freezes are still common across EMEA and above all in Europe,” says Silvia Cosso, associate research director, storage systems, IDC Western Europe. “However, the need to adapt to the new normal is bringing about an appetite for transformative investments in modernizing datacenters. The multicloud paradigm, increased interest in as-a-service consumption models, and the need to move IT infrastructure close to the end user is expected to push investments once economic activity resumes normal levels.”

Western European external storage market value was down 8,3% in dollars (-12.7% in euros), remaining in negative territory for the 6th quarter in a row. AFAs, however, proved buoyant, jumping to 45,5% of total value from 40,5% a year ago, recording a 3% increase Y/Y.

Overall, it seems that the worst is over for Western Europe, which went from double-digit declines in the past 2 quarters to a high single-digit decline. The outlook for 4Q20 remains cautious due to the new restrictions in force just before the festive period.

“Signs of recovery and appetites for investment are coming from businesses and the public sector alike across the region, propelled by the need to accelerate digital transformation projects, which are expected to drive a rebound in the market over the course of the next year. However, the short-term double threat of Brexit and further economic shocks from the pandemic could still hinder demand,” says Cosso.

Market growth in Central and Eastern Europe, and particularly the performance of the HCI and PBBA segments (at 20% of the total), managed to sustain the small growth in CEMA in the 3Q20. Y/Y value for the region increased 2,3% to reach $525,8 million.

While large projects were put on hold in CEE, the mid-range benefited from the relaxation of pandemic measures in the summer and was the main driver behind growth. MEA saw increased storage spending by the government, military, healthcare, and MSPs, but this was unable to compensate for the general slowdown of market activity.

AFAs continued to grow at double-digit rates (22.5%), convincingly dominating the market with 43% of total value.

“2020 proved to be more optimistic than expected for the storage market, which could be explained by a combination of delayed impact on business of the imposed COVID-related measures and their subsequent removal in most countries during the summer,” says Marina Kostova, research manager, storage systems, IDC CEMA. “The second wave will mostly likely shift the more substantial market recovery to 2H21. End users surveyed by IDC confirm this, but the magnitude of recovery could vary depending on the severity of new outbreaks of the new virus, the speed of mass vaccination, and government flexibility in supporting businesses.”

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter