SK hynix: Fiscal 2Q25 Financial Results

Revenue at ₩22.232 trillion, + 26% Q/Q and + 35% Y/Y

This is a Press Release edited by StorageNewsletter.com on July 25, 2025 at 2:02 pmSummary:

- Reports revenues of 22.232 trillion won, operating profit of 9.2129 trillion won, net profit of 6.9962 trillion won

- Both revenues, operating profit at all-time highs following brisk sales of AI memory

- Company to provide best-in-class AI products timely for customer satisfaction, market expansion

SK hynix Inc. announced that it has recorded 22.232 trillion won in revenues, 9.2129 trillion won in operating profit (with an operating margin of 41%), and 6.9962 trillion won in net profit(with a net margin of 31%) in the second quarter. Both revenues and operating profits stood at all-time highs, beating the previous best results in the fourth quarter of last year.

Both revenues and operating profits stood at all-time highs, beating the previous best results in the fourth quarter of last year.

The company said that an aggressive investment by global big tech companies into AI led to a steady increase in demand for AI memory. Shipments of both DRAM and NAND flash were higher than expected, helping the company log the best quarterly results.

SK hynix expanded sales of 12-high HBM3E in the DRAM space, while registering a growth in sales of NAND for all applications. With the competitiveness in AI memory and profitability-first management discipline, the company has maintained a positive earnings trend.

With the latest financial results, the company’s cash and cash equivalents increased to 17 trillion won at the end of June, up by 2.7 trillion won a quarter earlier. Its debt ratio and net debt ratio stood at 25% and 6%, respectively, as net debt fell by 4.1 trillion won, compared with the previous quarter.

In the second quarter, the inventory level was kept steady as customers increased both memory orders and production of their finished products. Demand for memory is expected to continue to grow as customers plan to launch new products in the second half.

Particularly, SK hynix foresees that increasing competition among big tech companies to enhance inference of AI models would lead to higher demand for high-capacity memory products. Ongoing investments by nations to build sovereign AI(1) would also help generate long-term demand for memory.

(1)Sovereign AI: a nation’s ability to build an independent AI system with its own infrastructure, data, talent and business network

The company expects the solid performance of its products and mass-production capabilities to help double HBM, compared with a year earlier, to generate stable earnings. It will also ensure timely provision of HBM4 in accordance with customers’ requests to remain competitive.

SK hynix will start provision of an LPDDR-based module for servers within this year, and prepare for GDDR7 products for AI GPUs with an expanded capacity of 24Gb from 16Gb in a bid to enhance its leadership in the AI memory market with product diversification.

For the NAND business, the company will maintain a prudent stance for investments considering demand conditions and profitability-first discipline, while continuing with product developments in preparation for improvements in market conditions. Particularly, it will expand sales of QLC-based high-capacity eSSD and build 321-high NAND-based product portfolio to enhance its market leadership.

Song Hyun Jong, president and head of corporate center, said that SK hynix will carry out part of the planned investments preemptively this year for smooth provision of major products with visible demand for next year including HBM: “We are on track to meet our goal as a Full Stack AI Memory Provider satisfying customers and leading market expansion through timely launch of products with best-in-class quality and performance required by the AI ecosystem.“

2Q25 Financial Results (K-IFRS)

")

– Financial information of the earnings is based on K-IFRS

– Please note that the financial results discussed herein are preliminary and speak only as of July 24, 2025. Readers should not assume that this information remains operative at a later time.

Resource:

Additional information with charts and financial tables

Comments

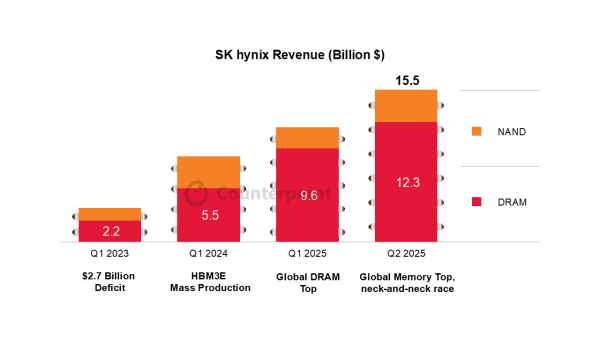

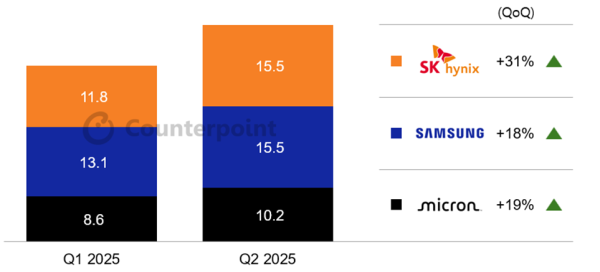

SK hynix announced a positive revenue trajectory that confirms the effect of AI especially on the HBM segment but also DRAM and NAND areas. And beyond AI training, the AI inference now plays a key role and requires high-performance plus optimized energy consumption high bandwidth memory aka HBM for various "forms" of AI. This strategic development angle pushed and promoted by the firm received strong market consideration with real adoption as the growth rate stated. It appears that a momentum is set on this aspect and we expect more details during the coming SK hynix keynote at FMS 2025 early August, being a top sponsor there.

We also wait competition reactions or just concurrent news regarding this HBM, DRAM and NAND aspects especially from Samsung and Micron, during their keynotes at the conference. The 2 images in the comment part come from Counterpoint Research and illustrate market positions and SK hynix growth.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter