Imation Letter To Arlington Shareholders

Underscoring "abysmal performance" under incumbent board

This is a Press Release edited by StorageNewsletter.com on May 18, 2016 at 2:51 pmImation Corp., a shareholder of Arlington Asset Investment Corp., sent a letter to Arlington shareholders highlighting the failed strategy undertaken by the company’s incumbent board of directors, led by executive chairman Eric Billings, and CEO Rock Tonkel.

Under their watch, Arlington has had persistent poor performance, while executive compensation has soared.

Imation urges all Arlington shareholders to read the letter below and watch the video, which underscores the fact that the company’s dividend is unsustainable and is at risk.

Imation encourages shareholders to vote the Gold proxy card to elect its nominees to create a sustainable enterprise and lasting value for all shareholders.

The full text of the letter:

May 17, 2016

Dear Fellow Arlington Shareholder:

You have a choice: stick with a ‘do nothing’ incumbent board or vote ‘for’ for Imation nominees who are committed to acting in your best interests.

We believe Arlington Asset Investment Corp.’s board of directors has failed as fiduciaries to shareholders for years. The company’s financial performance over the past five years has been awful, both on an absolute and relative basis, despite the company’s claims to the contrary.

The facts are clear – for years Arlington has been a poor investment relative to its peers. From 2011 to 2015, one dollar invested in Arlington’s peers is worth $1.40 whereas a dollar invested in the company is worth less than $0.85. Even with such woeful under performance, since 2011 management has paid itself $36.7 million, and the board has earned close to $5 million, both amounts in excess of peers and contrary to shareholder value creation over the same time period. Since Rock Tonkel was named CEO in June of 2014, Arlington’s stock price is down 38.5% on a dividend adjusted basis, yet he has earned an estimated $6.4 million over the same period, of which $5.1 million was cash bonuses and performance stock units. This misalignment of performance and executive compensation is simply unacceptable and the incumbent board needs to be held accountable.

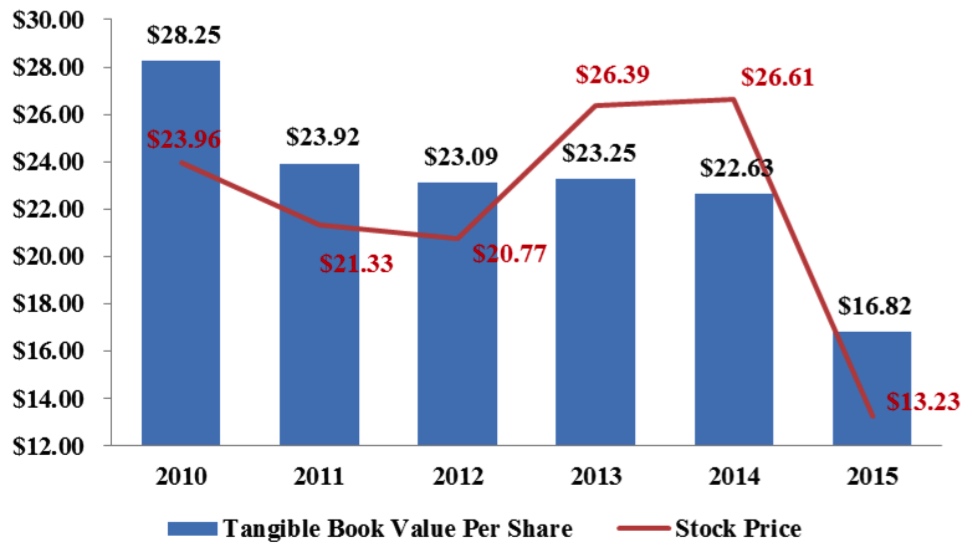

Historical perfomance of Arlington

Imation and its nominees, on the other hand, are proposing a sensible, level-headed approach to capital allocation and executive compensation that is based on share price performance and tangible book value creation. We also see numerous ways to lower overhead expenses.

Unfortunately, the incumbent board and management are doing everything in their power to obstruct our attempts to have a free and open dialogue about the future direction of the company in order to protect their incumbency and the millions of dollars they pay themselves. Disturbingly, they have refused to provide us with a copy of the company’s shareholder list in order to try to obstruct us from contacting you directly. As shareholders we all should ask – what are they are so afraid of? Meanwhile, the company has engaged in a robust outreach program, at significant shareholder expense, to ensure you only hear one side of the story – theirs.

Don’t be foolded: Arlington current dividend is unsutainable and leverage has soared

Arlington is trying to paint a rosy picture of its financial performance and health. Do not take the bait. While the company has paid a healthy dividend yield for years, it comes at a significant cost that could render those dividends unsustainable in the near-term.

A closer examination reveals some very disturbing trends:

- Arlington has been masking its poor financial health by funding its dividend from capital reserves and capital raises versus from operating profit. This is one of the least fiscally responsible actions a company can take and mimics tactics employed in the run-up to the financial crisis that crippled the world economy. We believe the board continues to pursue this reckless strategy simply in an effort to win this proxy fight and justify the millions of dollars they pay themselves.

- The company’s financial leverage has soared to 9.6x, up from 4.2x in the past two years.

- Arlington conjures up convenient Non-GAAP figures as the basis for its compensation and dividend ratio. According to the company’s metrics and methodology, since the onset of 2010, there was cumulative core operating earnings of $442 million. In reality, since the onset of 2010, operations have yielded only $129 million in value creation to the enterprise. Since 2014, operating losses have totaled $22 million.

- Arlington’s recently announced first quarter 2016 earnings results revealed the continued strategic failures of the company – tangible book value declined $2.37 per share, or 14%, in the past three months. And, in the last month alone, Arlington’s hedges lost $100 million. Meanwhile, compensation expense was up 6.3% year-over-year.

Is the board aligned with shareholders? Is Eric Billings a ful time employee? Why is he selling his stock. We have questions and we need answers.

- The average tenure of the current board members is over 11 years, and approximately two-thirds of the Board have served since the reorganization and value destruction of Friedman, Billings, Ramsay Group Inc.

- Did you know that Arlington’s executive chairman, Eric Billings, has made more than $15 million in compensation from 2011 through 2015? Did you know that Billings is also senior managing partner at his eponymous hedge fund, Billings Capital Management? How much is he making at his other full-time job? Did you know that after he stepped down as CEO in June 2014, his compensation did not change? As shareholders, we have the right to know how he spends his time.

- Did you know that since 2010, incumbent directors and officers have sold $14.5 million in stock at an average price of $25.39 per share, a premium of 75.7% to the company’s tangible book value, and that Billings personally has accounted for 99.6% of total sales in the open market during this period?

- Did you know that open market divestitures among insiders have accelerated as the company’s book value has decreased? Yet, why aren’t insiders buying the stock when it is down 38% in the past year? If the company is in fact being kept on the right track, we believe Arlington must explain why its insiders are not buying stock in their own company.

Imation’s slate has a focused goal: increase shareholder vaue for all sharehoders and proper from increases in long-term tangible book value

Imation’s nominees are capable, poised and 100% prepared to execute a turnaround at Arlington. We believe that new thinking and new people are required to fix old problems plaguing the company.

We believe Imation’s nominees, together with three continuing directors, would constitute a better board, and that our outlined plans will create a stable enterprise and lasting value for all shareholders. In fact, upon our successful proxy solicitation and our satisfaction with the go-forward management team and strategy, we are prepared to make a cash investment of $60 million at 1.0x tangible book value ($14.45 as of 3/31/2016), which represents a $2.07 premium based off the $12.38 share price at market close on May 13, 2016.

The future of Arlington is in your hands. We urge you to vote the Gold proxy to elect Imation’s nominees who we believe will effectively steward your investment at Arlington.

Your vote Is important. No matter how many shares of Arlington you own, we urge you to vote your Gold proxy today, to ensure that your instructions are received in a timely manner. Please vote by telephone or Internet by following the instructions on the enclosed Gold proxy card or by signing, dating and mailing your card in the enclosed envelope.

If any of your shares of common stock are held in the name of a brokerage firm, bank, bank nominee or other institution, they can only vote your shares upon receipt of your specific instructions.

Thank you for your support,

Joseph A. De Perio

Chairman, Imation Corp.

Imation’s presentation of Arlington to shareholders

Read also:

Imation Said Urgent Need For Board Change at Arlington

Because of underperformance, continued mismanagement and ineffective gedging strategies

2016.05.11 | Press Release

Imation and Clinton Group Attempting to Take Control of Arlington’s Board

Despite owning less than 0.05% of company’s shares

2016.05.09 | Press Release

Imation and Clinton Group Intend to Nominate Controlling Slate at Arlington Asset Investment

Despite owning Less than 0.1% of shares

2016.04.11 | Press Release

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter