Imation Said Urgent Need For Board Change at Arlington

Because of underperformance, continued mismanagement and ineffective gedging strategies

This is a Press Release edited by StorageNewsletter.com on May 11, 2016 at 2:56 pmImation Corp., a shareholder of Arlington Asset Investment Corp., sent a letter to Arlington shareholders highlighting the need for significant and immediate Board change at Arlington.

May 11, 2016

Dear Fellow Arlington Asset Shareholder:

The value of your investment in Arlington asset is at risk

Arlington Asset annual meeting of shareholders is less than a month away and you have an important decision to make that will impact the value of your investment. As owners of Arlington’s common stock, we cannot stand idly by and watch Arlington’s board oversee a management team that squanders shareholder resources, consistently underperforms its peer group and broader market benchmarks, and executes ill-conceived strategies that threaten the company’s dividend, all while taking home millions in compensation.

It’s clear to us that Arlington’s incumbent, legacy directors are content with the status quo and incapable – or unwilling – to make the right choices or act in the best interests of all shareholders.

We strongly urge you to help protect value at Arlington by voting on the Gold proxy card for the election of Imation’s five director nominees to the board – Scott R. Arnold, Barry L. Kasoff, Raymond C. Mikulich, Donald H. Putnam and W. Brian Maillian.

Our highly-qualified, independent, shareholder-first nominees have the necessary expertise in the sophisticated and complex mortgage-backed securities and asset management arenas to make changes at Arlington for the benefit of ALL shareholders.

Arlington has underperformed for years an management compensation

is excessive and misaligned

Arlington has underperformed over the last five years both on an absolute and a relative basis and is suffering the consequences of a poorly thought-out and poorly executed hedging strategy. However, management continues to cash big checks.

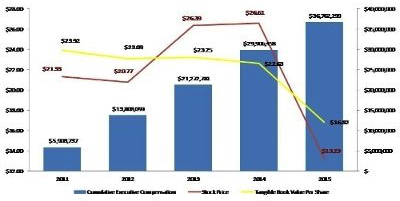

Over the last five years, Arlington’s stock price has plummeted 15.3% on a dividend adjusted basis. By comparison, over the same time frame, Arlington’s self-selected peer group as listed in its 2016 proxy statement had a dividend adjusted performance of positive 40%.

Importantly, even as shareholder value has nosedived, Arlington’s management and the board have been richly compensated. During this same five-year period, total compensation for Arlington’s named executive officers was $36.7 million and total board compensation was $4.9 million. We believe this level of compensation is unwarranted, excessive and misaligned with shareholder interests. Notably, we believe Arlington’s richly paid board and management team have lost faith in their company – the current board has sold nearly $15 million of Arlington stock at prices above $25 per share, and management and the COB have not purchased one share of Arlington stock in the open market in the last five years.

If elected, Imation’s nominees pledge to overhaul the company’s compensation practices with an owner’s eye to create true alignment of interest between management and shareholders. Additionally, unlike Arlington’s current management and Board, we plan to put our money where our mouth is. If we receive a voice in the boardroom and approve the go-forward management structure and strategy at Arlington, we would be prepared to invest up to 15% of the outstanding stock at 1.0x tangible book value[i] to buy out shareholders or improve the balance sheet. This represents an investment of up to $60 million at a premium to current stock trading levels.

Arlington’ edge position is poor and its dividend is not sustainable

For supposedly being ‘experts’ at developing investment strategies, we believe Arlington’s ability to develop proper hedging strategies is laughable. In fact, Arlington’s incumbent slate has no direct MBS investing experience outside of its management representatives. As a shareholder you must ask: How is the incumbent board qualified to oversee management when they lack basic industry expertise? Case in point- Arlington’s current hedged positions are failing miserably. At the end of the third quarter of 2015, Arlington reported a core short in the ten-year sector of the yield curve, as opposed to spreading out its hedging vehicles similar to the sensitivities of the MBS portfolio they were managing.

On the other hand, Imation’s nominees collectively have decades of experience trading, structuring, hedging and investing in MBS, advising government sponsored entities that issue MBS and operating and serving as investment professionals in asset management. We are confident that, if elected, our nominees will be able to diversify Arlington’s portfolio to yield higher returns and recalibrate the hedges to reduce investment losses.

Furthermore, while Arlington’s dividend may appear attractive on its face, a simple close examination reveals that the dividend is in fact unsustainable at current levels. When claiming that the stock has performed well, the company does not take into account dividends reinvested in the company, which is how a long term shareholder evaluates performance. We believe dividends need to be looked at in conjunction with examining tangible book value or even stock price. The company should pay dividends from its operating earnings; dividends should not just be a return of capital. We believe that under the company’s current dividend policy, a portion of the dividend represents a return of capital rather than a distribution from true economic earnings- essentially a strategy of Paul robbing Peter to pay Mary.

Immediate action is required – now is the time for change at Arlington

As a fellow shareholder, we want you to understand the risks presently plague Arlington- leverage is too high, the ongoing dividend appears to be unsustainable and the hedge position has failed, costing you millions. Meanwhile, management continues to get rich with no accountability.

Imation is committed to changing Arlington for the better and investing significant capital for the benefit of all shareholders. We are taking this risk because we strongly believe our nominees have the skillset to reduce the risks that currently haunt Arlington and enhance returns at the company.

As an investor, you are not required to continue to passively accept painful investment losses. Instead, vote the Gold proxy card today to elect Imation’s nominees who pledge to articulate a superior strategy for Arlington to restore shareholder value.

The future of Arlington is in your hands. We urge you to vote the Gold proxy card today to elect Imation’s nominees who we believe will effectively steward your investment at Arlington.

Read also:

Imation and Clinton Group Attempting to Take Control of Arlington’s Board

Despite owning less than 0.05% of company’s shares

2016.05.09 | Press Release

Imation and Clinton Group Intend to Nominate Controlling Slate at Arlington Asset Investment

Despite owning less than 0.1% of shares

2016.04.11 | Press Release

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter