Imation and Clinton Group Attempting to Take Control of Arlington’s Board

Despite owning less than 0.05% of company's shares

This is a Press Release edited by StorageNewsletter.com on May 9, 2016 at 2:47 pmArlington Asset Investment Corp. has filed and intends to mail a letter to shareholders in connection with the company’s 2016 annual meeting of shareholders to be held on June 9, 2016.

The May 6, 2016 letter urges Arlington shareholders

to protect their investment in the company and highlights the following:

- The Arlington board of directors is composed of highly qualified nominees who have overseen a consistent and clearly articulated strategy that has delivered robust dividends over 25 consecutive quarters;

- Imation Corp. and the Clinton Group, Inc. (collectively the Imation Group) have nominated a controlling slate to Arlington’s board despite owning less than 0.05% of the company’s shares, an action that we believe is being undertaken to extract value from Arlington at the expense of all other shareholders; and

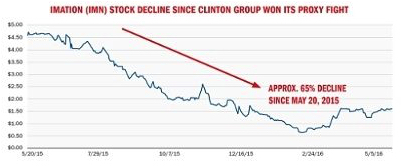

- Since the Clinton Group won its proxy fight at Imation in May 2015, Imation’s stock has lost approximately 65% of its value while Imation has engaged in self-dealing transactions involving more than $50 million, or over 80% of Imation’s current $60 million market cap, all for the benefit of the Clinton Group and other insiders.

- The company believes that the Imation Group would follow the same sham playbook at Arlington that destroyed value at Imation, putting Arlington’s dividend and its shareholders’ investment at significant risk.

The full text of the letter follows:

Dear Fellow Arlington Shareholder:

The Arlington board is dedicated to delivering value. Our performance enabled the company to continue to pay a significant, stable dividend of $0.625 per share for the first quarter of 2016.

Since we began focusing exclusively on our current investment strategy in June 2009, Arlington has delivered a more than 317% total return to shareholders[1], and the company has paid a dividend each quarter to shareholders over 25 consecutive quarters, for a total of $19.40 per share. We believe our strategy and our current leadership are best positioned to continue to deliver a stable, robust dividend to our shareholders.

Protect the value of your investment and your dividend;

vote the white proxy card today

At this year’s annual meeting on June 9, 2016, you and all fellow Arlington shareholders will be faced with a stark choice: to support your board’s highly qualified director nominees, who have deep and relevant industry experience and a long record of commitment to creating value for all shareholders. Or to elect the nominees of Imation Corp., a storage technology company with no experience in our sector, and the New York City-based hedge fund, Clinton Group, who we believe would advance their own self-interest and risk the value of your investment, including the continuation of our quarterly dividend.

Despite owning less than 0.05% of the company’s shares, the Imation Group has nominated a controlling slate of five individuals to stand for election to our board at the annual meeting. Given its track record and extremely small investment in the company, we believe that the Imation Group has nominated this controlling slate to extract value from Arlington at the expense of all other shareholders.

Imation Group’s track record is littered with self-dealing for the benefit of Clinton Group and other insiders

After initially winning three seats through a proxy contest at Imation’s 2015 annual meeting, the Clinton Group’s nominees quickly took control of Imation’s board and the executive suite, appointing themselves as Imation’s COB, interim CEO, interim president, interim CFO and chief restructuring officer.

Once the Clinton Group nominees gained control of Imation, their board promptly caused Imation to engage in numerous highly questionable, self-dealing transactions, involving more than $50 million or over 83% of Imation’s current approximately $60 million market cap[2], including:[3]

- Authorizing an investment of up to $35 million of Imation’s cash into a hedge fund managed by Clinton Group.

- Imposing on Imation shareholders a lucrative off-market fee deal with Clinton Group in connection with this investment.

- Clinton Group obtained a 25% quarterly performance fee from Imation, payable in Imation shares. Until your board recently publicly criticized this deal, these shares were to be issued to the Clinton Group at a fixed value of $1.00 – less than two thirds of the current market value of Imation’s stock.

- According to Imation’s public filings, the Clinton Group will be paid quarterly for any gains – whether realized or not – with no disclosed ‘high-water mark’ or ‘clawback’ for annual investment losses. In other words, Clinton Group can make money even if Imation shareholders lose value. And Imation shareholders bear all the risk of loss.

- Entering into a consulting agreement with a restructuring firm founded and led by Barry Kasoff, an Imation officer and board member. Kasoff and his firm received a total of more than $6 million in compensation from Imation, which included fees of $3 million in 2015 for less than 5 months of work, and up to approximately $2.2 million in Q1 2016. In 2015, he also received $679,000 in direct compensation for 4.5 months of employment at Imation in addition to director fees of $137,057.

- Kasoff appears to have been paid multiple times for the exact same services – in his capacity as a director, officer, and simultaneously for the provision of consulting services to Imation, via the firm he founded and leads.

- Kasoff is now an Imation Group nominee to Arlington’s board.

- Reimbursing Clinton Group $600,000 for its proxy fight expenses at Imation, at the expense of Imation’s shareholders.

- Acquiring a business founded and led by Imation director Geoff Barrall for $6.7 million at closing, plus an additional $5 million in future contingent payments. Director Barrall also received $200,000 in consulting fees (in addition to board fees) from Imation in 2015 for six weeks of work. He recently resigned from the board and is serving as CTO of Imation.

- Paying $300,000 in consulting fees to Imation director Robert Fernander – a Clinton Group nominee to Imation’s board – for six weeks of work in addition to being paid $150,387 in director fees in 2015. Thereafter, Fernander was appointed CEO of Imation and received $1.3 million in direct compensation for approximately 3 months of employment at Imation in 2015.

All of these transactions were approved by a board dominated by the beneficiaries of these deals – Clinton Group nominees and its chosen directors. None of these transactions appear to have included receipt of independent fairness opinions or independent financial advice. Importantly, none of these transactions were approved by Imation shareholders.

$1 invested in Imation on May 21, 2015, the day after Clinton got on the Imation board, was worth 35 cents on May 5, 2016, a decline of approximately 65% pver less than one year

You will hear the Imation Group claim that they have completed a transformation at Imation.

Here is what they are not telling you about the value destructive changes

that they have caused in less than one year:

- Since the Clinton Group won its proxy contest on May 20, 2015, Imation’s stock has lost approximately 65% of its value. In fact, Imation stock has traded so low since that time that the New York Stock Exchange has informed Imation it is in jeopardy of being de-listed from its exchange.

- Despite promising that they would evaluate returning excess capital to Imation shareholders by December 1, 2015, Clinton Group nominees have failed to return any value to Imation shareholders since taking control – no dividends and no disclosed open market share repurchases – instead authorizing a $35 million investment in Clinton Group funds.

The only people who have not lost money at Imation since May 20, 2015 are the Clinton Group nominated directors, thanks to millions of dollars in insider deals.

Now, the Clinton Group is using Imation as its platform to run multiple simultaneous proxy fights at other companies, including at Arlington. The Clinton Group is saddling Imation’s shareholders with the expense of running proxy contests in pursuit of what we believe to be its own self-serving agenda.

Learn from the mistakes of Imation’s shareholders

The Imation Group has disclosed only hints of its plans for Arlington, which sound frighteningly familiar to its self-serving and value-destroying agenda at Imation:

- If it is successful in its proxy contest, the Imation Group intends to have Arlington repay the Imation Group’s total proxy contest fees – which it currently anticipates to be approximately $1,000,000. This reimbursement would be at the expense of Arlington shareholders.

- It appears that the Imation Group will solicit an external manager for Arlington, which they would hand-pick with a majority of Arlington’s board. Given their track record at Imation, we believe that the Imation Group’s ‘process’ will result in a self-serving, related party transaction with either the Clinton Group or Imation serving as the external manager of Arlington.

- We believe the Imation Group would follow the same sham playbook at Arlington that destroyed value at Imation, putting your dividend and investment at significant risk.

Do not let the Imation Group’s nominee take control of your company and repeat the disaster at Imation; vote ‘For’ all of the Arlington board nominees on the white proxy card today

We urge shareholders to avoid the excessive risk posed by the Imation Group’s proposal. Your board is committed to building value for all Arlington shareholders and continuing to deliver a stable, robust dividend. Vote ‘For’ your board of directors’ experienced and highly qualified director nominees by telephone, over the internet, or by signing, dating and returning the enclosed WHITE proxy card today.

On behalf of your board of directors and management team, we thank you for your continued support.

Sincerely,

The Arlington board of directors

Eric F. Billings

J. Rock Tonkel, Jr.

Daniel J. Altobello

Daniel E. Berce

David W. Faeder

Peter A. Gallagher

Ralph S. Michael, III

Anthony P. Nader, III

[1]percentages if dividends not reinvested.

[2] Based on May 5, 2016 closing price.

[3] Source: Imation SEC filings, including preliminary proxy statement filed on April 29, 2016

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter