Samsung Electronics: Fiscal 1Q26 Financial Results

Generating KRW 133.9T, up 43% QoQ and up 69% YoY

By Philippe Nicolas | July 9, 2026 at 2:01 pmSamsung Electronics published its 1Q26 earnings but didn’t provide any press release. We spent time to dig and analyze other documents to summarize results below.![]() The company posted its strongest quarter on record in 1Q 2026, driven overwhelmingly by the memory business riding the AI infrastructure buildout.

The company posted its strongest quarter on record in 1Q 2026, driven overwhelmingly by the memory business riding the AI infrastructure buildout.

In details it shows:

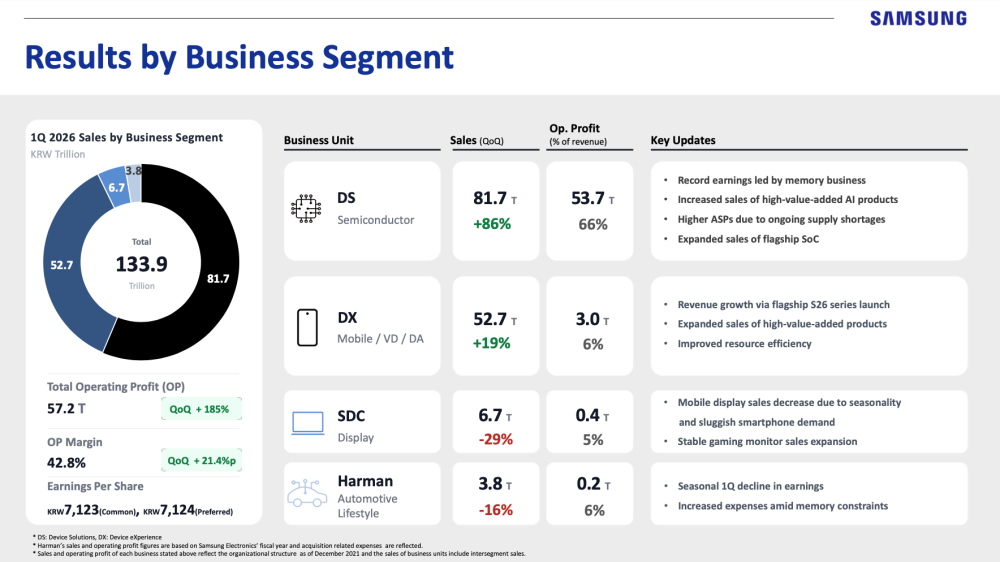

- Consolidated revenue reached KRW 133.9 trillion, up 43% QoQ and 69% YoY

- Operating profit hit KRW 57.2 trillion, up 185% QoQ and a striking 756% YoY, pushing operating margin to 42.8% (from 21.4% in 4Q25 and just 8.4% in 1Q25)

- R&D investment was KRW 11.3 trillion (+4% QoQ, +26% YoY)

- Net profit came in at KRW 47.2 trillion (35.3% of sales), EPS reached KRW 7,123 (common) versus KRW 2,909 in 4Q25 and KRW 1,192 a year earlier, and ROE jumped to 41% from 19% in 4Q25 and 8% in 1Q25

- EBITDA margin reached 51%

Click to enlarge

Samsung attributes the results to AI-driven technology leadership, high-value-added product mix, and disciplined market response amid macro uncertainty.

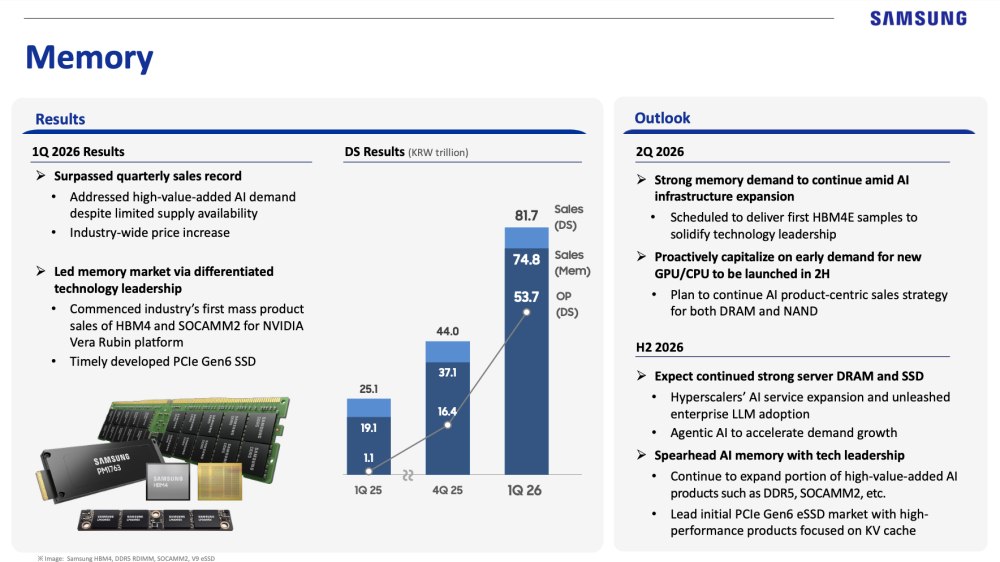

The growth clearly comes from the DS/semiconductor segment. DS sales were KRW 81.7 trillion (+86% QoQ, +225% YoY) with operating profit of KRW 53.7 trillion, a 66% margin and 66% of total group operating profit. Memory alone contributed KRW 74.8 trillion in sales (+101% QoQ, +292% YoY), described as a “record earnings” quarter for the segment.

Click to enlarge

Strong AI-linked demand despite constrained supply, industry-wide price increases, and the start of industry-first mass shipments of HBM4 and SOCAMM2 for Nvidia’s Vera Rubin platform, alongside timely delivery of PCIe Gen6 SSDs. Looking to 2Q26, Samsung expects continued strong memory demand tied to AI infrastructure expansion, plans to sample HBM4E, and intends to capitalize on new GPU/CPU launches in 2H with an AI-centric DRAM/NAND sales strategy. For H2 2026 it expects sustained server DRAM/SSD strength from hyperscaler AI service expansion, enterprise LLM adoption, and agentic AI demand, while expanding high-value-added products (DDR5, SOCAMM2) and targeting leadership in the early PCIe Gen6 eSSD market focused on KV-cache use cases.

Click to enlarge

The quarter underscores that Samsung’s HBM4/SOCAMM2 ramp for Nvidia’s Vera Rubin platform, combined with tight DRAM/NAND supply and rising ASPs, has become the dominant profit driver for the entire group, DS alone generated 94% of consolidated operating profit. This mirrors the broader memory-supercycle narrative playing out across Micron and SK Hynix, with Samsung explicitly flagging PCIe Gen6 eSSD/KV-cache positioning and AI-driven DDR5/SOCAMM2 mix shift as its next competitive battlegrounds through 2026.

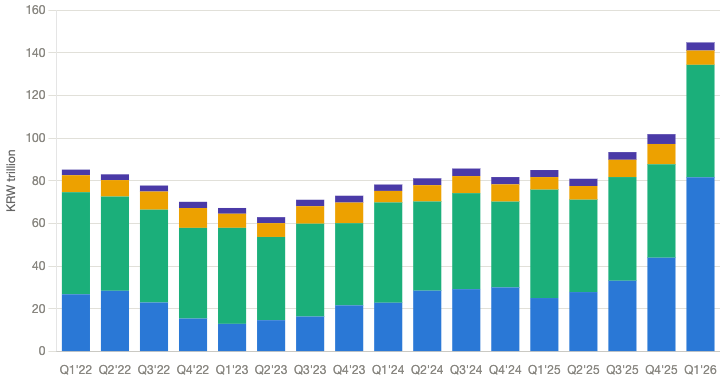

We made the choice to not detail and analyze other Samsung revenue segments but wish to add a historical revenue graph.

The graph above shows 17-quarter trajectory from Q1 2022 to Q1 2026 showing the longest stretch with fully comparable DS/DX/SDC/Harman reporting since Samsung’s DX division reorg took effect.

What the split shows:

- DS (memory/foundry) is the whole story of the last five quarters. It bottomed at ~13tn during the 2023 memory downturn, climbed steadily through 2024-25, then exploded from 25tn (Q1’25) to 81.7tn in Q1’26, an all-time high on HBM4 ramp and AI-driven ASP surges

- DX (mobile, TV, appliances) has stayed remarkably flat, oscillating 38-53tn regardless of the semiconductor cycle, it’s the ballast of the group

- SDC tracks smartphone launch seasonality (spikes in Q4, dips in Q1) in a tight 5.4-9.7tn band

- Harman is the smallest and steadiest line, drifting from ~2.6tn to ~4.6tn as the automotive/audio business has scaled

The net effect: total quarterly revenue went from ~78tn in Q1’22 to ~134tn in Q1’26, almost entirely because DS’s share of the mix roughly tripled while everything else stayed roughly the same size.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter