Silicon Motion: Fiscal 1Q24 Financial Results

Silicon Motion: Fiscal 1Q24 Financial Results

Sales decreased 6% Q/Q and increased 53% Y/Y

This is a Press Release edited by StorageNewsletter.com on May 8, 2024 at 2:02 pm| (in $ million) | 1Q23 | 1Q24 | Growth |

| Revenue |

124.1 | 189.3 | 53% |

| Net income (loss) | 10.2 | 16.0 |

Sales decreased 6% Q/Q and increased 53% Y/Y in 1FQ24.

- SSD controller sales: in 1FQ24 increased 0% to 5% Q/Q and increased 35% to 40% Y/Y

- eMMC+UFS controller sales: in 1FQ24 decreased 10% to 15% Q/Q and increased 235% to 240% Y/Y

- SSD solutions sales: in 1FQ24 decreased 5% to 10% Q/Q and decreased 30% to 35% Y/Y

Silicon Motion Technology Corporation announced its financial results for the quarter ended March 31, 2024.

For 1FQ24, net sales decreased sequentially to $189.3 million from $202.4 million in 4FQ23.

Net income (GAAP) decreased to $16.0 million, or $0.48 per diluted American Depositary Share of the company (ADS) (GAAP), from net income (GAAP) of $21.1 million, or $0.63 per diluted ADS (GAAP), in 4FQ23. For 1FQ24, net income (non-GAAP) decreased to $21.6 million, or $0.64 per diluted ADS (non-GAAP), from net income (non-GAAP) of $31.3 million, or $0.93 per diluted ADS (non-GAAP), in 4FQ23.

1FQ24 Review

“Our business remained strong in 1FQ24 as demand was stronger than expected and improving ASPs continued to drive better profitability,” said Wallace Kou, president and CEO. “Our client SSD revenue increased again for the 4th consecutive quarter as end-market demand stabilized and programs with our flash maker customers continue to scale. This was a strong start to 2024, and we are confident that we have the right products and the right customers to continue to grow our business and profitability throughout this year.”

During 1FQ24, the company had $10.7 million of capital expenditures, including $5.0 million for the routine purchase of testing equipment, software, design tools and other items, and $5.7 million for building construction in Hsinchu, Taiwan.

Business Outlook

“Our new programs with our flash maker customers are expected to continue to scale throughout this year as the move to increase outsourcing continues to build the foundation for long-term growth of our business,” said Kou. “Our highly differentiated controller solutions enable PC and smartphone OEMs to utilize high performance, higher density and lower cost solid state storage to enable cutting edge applications such as AI-at-the-edge. Based on our strong start to the year and our increasing backlog, we are increasing our full-year outlook. We expect our business will continue to improve steadily throughout 2024 as we continue to scale new SSD and eMMC+UFS controller programs that will also improve our ASPs and profitability steadily throughout this year.”

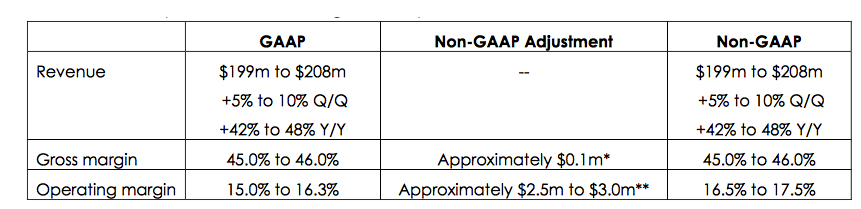

For 2FQ24, management expects:

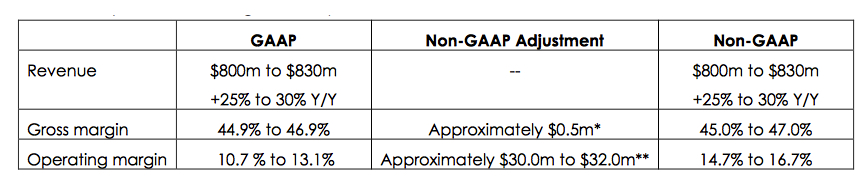

For FY24, management expects:

* Projected gross margin (non-GAAP) excludes $0.1 million of stock-based compensation.

* Projected gross margin (non-GAAP) excludes $0.1 million of stock-based compensation.

** Projected operating margin (non-GAAP) excludes $2.5 million to $3.0 million of stock-based compensation and dispute related expenses.

Comments

CEO Kou commented: "We had a good start to 2024. We delivered sequential revenue growth ahead of expectations, achieved gross margin in the high end of our guidance range, and exceeded our operation margin outlook. Our SSD controller business was better than expected, primarily driven by demand from 2 of our flash maker customers."

In 1FQ24, sales decreased 6% Q/Q to $189 million. SSD controller sales increased slightly by zero to 5% Q/. eMMC and UFS controllers declined 10% to 15% Q/Q. SSD solutions sales decreased 5% to 10% Q/Q. Gross margin increased to 45%, reflecting both better mix and higher ASPs. Operating expenses were $62.5 million, $1 million higher than 4FQ23 primarily due to higher R&D expenses to support company's technology leadership.

The firm continues to improve its pricing in 1FQ24, which is driving the steady improvement in its gross margin and profitability. Its results reinforce its leadership position in controller technology and its product continues to be in high demand as some customers recognize how important its technology innovation and service are to their business.

Silicon Motion has seen NAND flash prices continue to increase since late last year and more recently have seen flash makers gradually increase utilization in their fabs, but a more meaningful capacity increase from the build-out of next gen NAND flash isn’t expected until next year. Demand remains robust, especially with Chinese handset OEMs as well as with enterprise and data center storage markets.

The firm is seeing strong traction with its new PCIe Gen 5 8-channel controller released last year. This is the first 6 nanometer 8-channel PCIe Gen 5 controller available in the market and the firm is winning with virtually every top module maker in addition to its 3 flash maker customers. The result from early testing has been very good. This is a product that will be suited for high end notebook and desktop AI PC, as well as for gaming and workstation PC that offer performance with low power consumption. In addition, the firm has a strong pipeline of design activity with several flash makers for PCIe Gen 4 SSD, building their next gen QLC and QLC NAND.

The manufacturer also continues to see stronger than ever demand for its UFS 3.1 and 2.2 controllers, especially to support a new gen of low-cost NAND. In addition to several top module makers serving the smartphone market, it started ramping up a new flash maker customer for UFS 3.1 and 2.2 this quarter.

| Period | Revenue | Y/Y growth | Net income (loss) |

| FY22 | 945.9 | 3% | 172.5 |

| 1FQ23 | 124.1 | -49% | 10.2 |

| 2FQ23 | 140.4 | -44% | 11.0 |

| 3FQ23 | 172.3 | 31% | 11.0 |

| 4FQ23 | 200.8 | 1% | 23.5 |

| FY23 | 639.1 | -32% | 52.9 |

| 1FQ24 | 189.3 | 53% | 16.0 |

| 2FQ24 (estim.) | 199-208 | 42-48%% | NA |

| FY24 (estim) | 765-800 | 20-25% | NA |

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter