Silicon Motion: Fiscal 4Q23 Financial Results

Silicon Motion: Fiscal 4Q23 Financial Results

Sales up 17% Q/Q and 1% Y/Y at $202 million

This is a Press Release edited by StorageNewsletter.com on March 8, 2024 at 2:02 pm| (in $ million) | 4Q22 | 4Q23 | FY22 | FY23 |

| Revenue | 200.8 | 202.4 | 945.9 | 639.1 |

| Growth | 1% | -32% | ||

| Net income (loss) | 23.5 | 21.1 | 172.5 | 52.9 |

Business Highlights

• 4FQ23 sales increased 17% Q/Q and increased 1% Y/Y

• SSD controller sales: 4FQ23 increased 15% to 20% Q/Q and increased 0% to 5% Y/Y

• eMMC+UFS controller sales: 4FQ23 increased 25% to 30% Q/Q and increased 20% to 25% Y/Y

• SSD solutions sales: 4FQ23 decreased 5% to 10% Q/Q and decreased 45% to 50% Y/Y

• Announced annual cash dividend of $2.00 per ADS

Silicon Motion Technology Corporation announced its financial results for the quarter ended December 31, 2023.

For 4FQ23, net sales (GAAP) increased sequentially to $202.4 million from $172.3 million in 3FQ23. Net income (GAAP) increased to $21.1 million, or $0.63 per diluted American Depositary Share of the Company (ADS) (GAAP), from net income (GAAP) of $10.6 million, or $0.32 per diluted ADS (GAAP), in 3FQ23.

For 4FQ23, net income (non-GAAP) increased to $31.3 million, or $0.93 per diluted ADS (non-GAAP), from net income (non-GAAP) of $21.1 million, or $0.63 per diluted ADS (non-GAAP), in the 3FQ23.

4FQ23 Review

“Our fourth quarter results exceeded expectations as demand across the majority of our products increased sequentially, driven by holiday season demand and normalizing channel inventory,” said Wallace Kou, president and CEO. “Both eMMC+UFS and SSD controller demand grew strongly in the quarter. We are confident that our teams’ ongoing commitment to deliver controller solutions that enable our customers to service a broader range of markets will continue to drive share gains for us and be the foundation for strong growth in 2024 and beyond.”

Acquisition Update

On May 5, 2022, Silicon Motion and MaxLinear, Inc. entered into a merger agreement, pursuant to which Silicon Motion agreed to be acquired by MaxLinear, with (a) holders of Silicon Motion ordinary shares, par value $0.01, to receive $23.385 in cash and 0.097 shares of MaxLinear common stock, par value $0.0001 for each share that they hold (other than certain customary excluded Shares), and (b) ADS holders to receive $93.54 in cash and 0.388 shares of MaxLinear Common Stock for each ADS that they hold (other than ADSs representing certain customary excluded Shares), in each case, with cash in lieu of any fractional shares of MaxLinear common stock .

On August 31, 2022, shareholders at Silicon Motion’s extraordinary general meeting of shareholders approved the transaction.

On July 26, 2023, the 2 companies received antitrust approval from the State Administration for Market Regulation of the People’s Republic of China. Shortly after receiving SAMR Approval, Silicon Motion received notice from MaxLinear of its purported termination of the merger agreement. MaxLinear did not provide any factual basis for its purported termination, and Silicon Motion believes its actions constituted a willful and material breach of the merger agreement.

Silicon Motion has filed a claim in the Singapore International Arbitration Centre, which is the venue for dispute resolution under the merger agreement, and is pursuing payment of the termination fee of $160 million, together with further substantial damages, interest and costs.

Business Outlook

“We expect sustained growth across our business in 2024, driven by wins with our module maker customers and significant design wins and share gains with our flash maker customers, as they look to outsource more controllers to effectively address a broader range of end-markets,” said Kou. “We are confident that our strong backlog and project ramps will be the foundation for strong growth this year. These new wins for our eMMC+UFS and SSD controllers will grow our relationship with our flash maker partners this year and increase revenue from these customers by approximately 50%.“

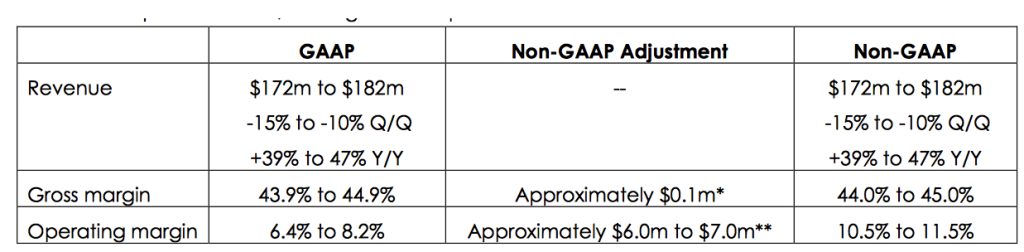

For 1FQ24, management expects:

* Projected gross margin (non-GAAP) excludes $0.1 million of stock-based compensation.

** Projected operating margin (non-GAAP) excludes $6.0 million to $7.0 million of stock-based compensation and dispute related

expenses.

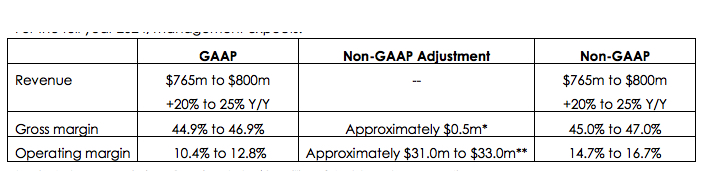

For FY24, management expects:

* Projected gross margin (non-GAAP) excludes $0.5 million of stock-based compensation.

** Projected operating margin (non-GAAP) excludes $31.0 million to $33.0 million of stock-based compensation and dispute related expenses.

Comments

Net sales in 4FQ23 reached $202.4 million, up 17% Q/Q and 1% Y/Y, above what was expected last quarter (between $190 million and $198 million or +10% to +15% Q/Q).

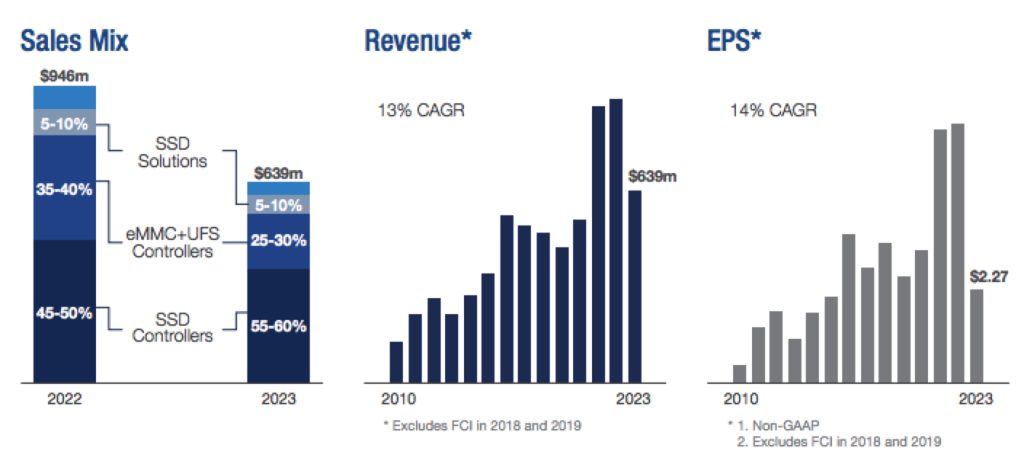

The company has 3 businesses:

- SSD controllers

- eMMC & UFS controllers

- Customized specialty SSD solutions

It is pleased by the steady recovery across its business throughout 2023. It benefited in 4FQ23 from stronger demand from both SSD and eMMC+UFS controllers and saw pricing and mix improved to drive stronger gross margin improvement for its business than originally expected.

Its technology leadership in controller and its unwavering engagement with its customers, both flash makers and module makers, has laid the foundation for strong 2024 growth despite only modest growth expecting in the PC and smartphone device markets, driven largely by firm's ongoing share gains with its customers.

SSD controller sales grew 15% to 20% sequentially. eMMC and UFS controller sales grew 25% to 30% sequentially and SSD solution sales decreased 5% to 10% sequentially.

The manufacturer said that pricing for NAND flash has been steadily increasing and expected to continue to improve throughout 2024 and into 2025. NAND makers are being disciplined in their production and limiting output, resulting in higher NAND flash prices.

Revenue from flash maker is expected to grow approximately 50% this year, a design win across its controller program meaningfully throughout 2024.

For 1FQ24, Silicon Motion expects revenue to be down 10% to 15% sequentially but up 39% to 47% Y/Y to $172 million to $182 million. It expects SSD controller sales will decline slightly and eMMC and UFS controller sales will decrease. Gross margin is expected to be in the range of 44% to 45%. Operating margin will be in the range of 10.5% to 11.5%. Effective tax rate will be approximately 19% and stock-based compensation and dispute-related expenses will be in the range of $6 million to $7 million.

For FY24, revenue will increase yearly 20% to 25% to $765 million to $800 million. Gross margin is expected to be in the range of 45% to 47%. Operating margin should be in the range of 14.7% to 16.7%, and effective tax rate for the year is expected to be approximately 19%. Full year stock-based compensation dispute and related expenses will be in the range of $31 million to $33 million.

Company expects its revenue from all of its flash maker customers will grow in 2024 and to increase approximately 50% this year.

| Period | Revenue | Y/Y growth | Net income (loss) |

| FY22 | 945.9 | 3% | 172.5 |

| 1FQ23 | 124.1 | -49% | 10.2 |

| 2FQ23 | 140.4 | -44% | 11.0 |

| 3FQ23 | 172.3 | 31% | 11.0 |

| 4FQ23 | 200.8 | 1% | 23.5 |

| FY23 | 639.1 | -32% | 52.9 |

| 1FQ24 (estim.) | 172-182 | 39-47% | NA |

| FY24 (estim) | 765-800 | 20-25% | NA |

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter