History (1998): Over 130 Million HDDs Shipped in 1997

For $25 billion revenue

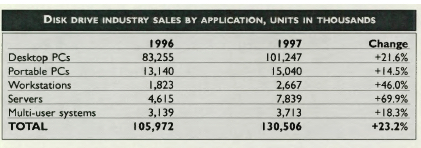

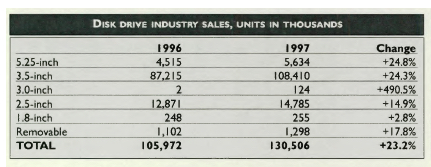

By Jean Jacques Maleval | December 23, 2021 at 2:01 pmDespite a late-year slowdown brought on by oversupply, the HDD drive industry shipped a record 130.5 million units in 1997, according to industry totals just compiled by Trendfocus, a Palo Alto, CA-based market research firm.

Strong PC shipments and growing sales of network servers and workstations were the main factors in the 23.2% growth.

“The disk drive industry grew, but at a price: oversupply in 2H97 destroyed pricing models and profit margins,” stated John Donovan, VP, Trendfocus. “This situation will only worsen in the first quarter of 1998 before rebounding in the second half of the year. Average storage capacities skyrocketed during the year.”

“Entering 1997, the average disk drive for desktop PCs stored 1.4GB. At year’s end, the average capacity was over 2.2GB, a growth of 60%,” he added. “Concurrently, prices collapsed, offering end-users the most economical price-per-megabyte ratio in the history of the HDD business.”

However, the research firm’s statistics indicated the shifting demand patterns will slow the rate of growth in capacities. Desktop PCs consumed the bulk of HDDs in 1997, but the emergence of the sub-$1,000 PC will force profound changes in desktop pricing and supplier strategies in 1998.

The enterprise/server sector’s demand patterns for drives began a dramatic shift in 1997, with the average number of drives per server dropping markedly. At the same time, the supply of drives to this area mushroomed, leading to severe price erosion and market share changes.

The portable market struggled through 1997. Prices for notebook PCs remained much higher than those for desktops, thereby limiting the growth potential. 2.5- inch drives won out, beating the threat from the 3.0-inch size.

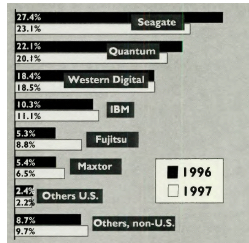

Market shares changed in 1997. Seagate maintained the top market position, but found its leadership post in the enterprise/server market under assault. Quantum was again the second largest supplier, and Western Digital third. Maxtor and Fujitsu made the largest share gains in the year.

“And while US suppliers dominate, non-US suppliers made impressive gains for the third year running,” stated Donovan. “Fujitsu, Toshiba, Hitachi, and Samsung are all investing hundreds of millions of $s annually, and are once again threatening US suppliers across the product spectrum. Since 1994, there has been a four-fold increase in non-US market share.“

The outlook for 1998 is for slower unit growth and lower industry profitability.

“The disk drive industry has dug itself a hole, one which will take at least half the year to climb out of,” asserted Donovan. “Our initial forecast is for 147 million drives to ship this year, with revenue flat or slightly down. Fundamentally, the rules of the game have changed. With the cheap PC forcing the industry into new design and price models, capacity growth slowing as areal densities rise, the competitive gap closing, and no new, pervasive, storage hungry application due immediately, cost will be king.”

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter