Marvell: Fiscal 1Q22 Financial Results

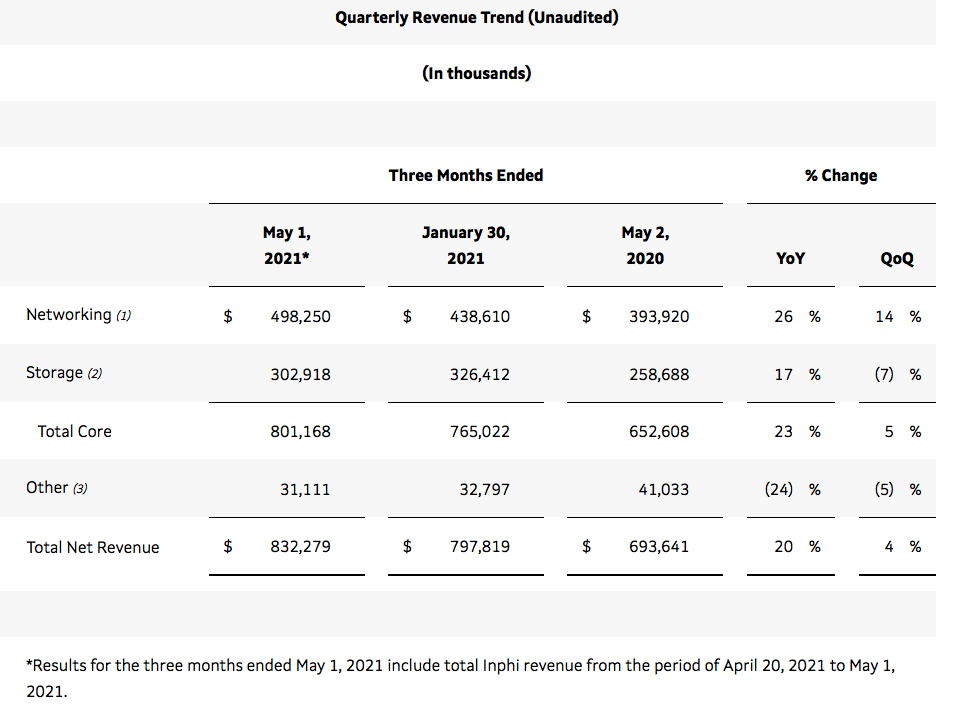

Storage at $303 million, up 17% Y/Y and down 7% Q/Q, representing 36% of global revenue

This is a Press Release edited by StorageNewsletter.com on June 9, 2021 at 2:32 pm| (in $ million) | 1Q21 | 1Q22 | Growth |

| Revenue |

693.6 | 832.3 | 20% |

| Net income (loss) | (108.0) | (116.0) |

Marvell Technology, Inc. reported financial results for the first quarter of fiscal year 2022.

It completed the acquisition of Inphi Corporation on April 20, 2021 approximately 10 days before the end of 1FQ22. Results for this quarter include the results of Inphi from the acquisition date.

Net revenue for 1FQ22 was $832 million, GAAP net loss (88) million, or $(0.13) per diluted share, non-GAAP net income of $202 million, or $0.29 per diluted share.

“We began FY22 on a strong note, with stand-alone Marvell revenue growing 17% Y/Y for the first quarter. The acquisition of Inphi increases and accelerates our growth opportunity in the data center, Marvell’s largest end market by revenue,” said Matt Murphy, president and CEO. “Marvell’s outlook for strong revenue growth in the second quarter highlights robust demand across all our key end markets. I have never felt stronger about our prospects and believe that we are at the beginning of a multi-year growth cycle.”

The financial outlook for 2FQ22 2022 includes expected results of Inphi for the full quarter.

• Net revenue is expected to be $1.065 billion +/- 3%.

• GAAP gross margin is expected to be 34.8% to 37.5%.

• Non-GAAP gross margin is expected to be approximately 64%.

• GAAP operating expenses are expected to be $633 million to $643 million.

• Non-GAAP operating expenses are expected to be $370 million to $375 million.

• Basic weighted average shares outstanding are expected to be 822 million.

• Diluted weighted average shares outstanding are expected to be 835 million.

• GAAP diluted loss per share is expected to be $(0.37) +/- $0.04 per share.

• Non-GAAP diluted income per share is expected to be $0.31 +/- $0.03 per share.

Comments

Revenue for this quarter was $810 million, up 20% Y/Y and 4% Q/Q. Its the fourth straight quarterly period of double-digit Y/Y revenue growth.

But the company is back to huge losses compared to $16.6 million net profit in 4FQ21.

Storage products, comprised primarily of storage controllers and FC adapters, reached $303 million, growing 17% Y/Y and declining 7% Q/Q, and representing 36% of total revenue vs. 41% last quarter and 37% in 1FQ21.

Storage results were better than expected as the firm benefited from stronger demand for SSD controllers. The stellar Y/Y results were driven by ramps in custom DIY SSD controller programs and ongoing growth in cloud demand for nearline drives. The 7% sequential decline was primarily due to FC business.

Looking to 2FQ22, Marvell expects storage to deliver another strong performance driven by the nearline HDD and data center SSD markets. It is projecting revenue to grow Y/Y in the mid-teens and in the double-digits sequentially on a percentage basis.

In HDD business, data center has become the largest revenue contributor relative to other markets. Preamplifier business is now ramped up to an annualized run rate of over $50 million, and the company believes that it can more than double this run rate.

The firm is forecasting revenue to be in the range of $1.065 billion, plus or minus 3%. At the middle point of this outlook, it expects approximately $250 million of revenue contribution from the Inphi business.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter