WW Converged Systems Revenue Up 9.4% Y/Y in 2017 at $ $12.5 Billion – IDC

4Q17 ranking in hyperconverged systems: 1/VMware, 2/Nutanix, 3/Dell, 4/HPE

This is a Press Release edited by StorageNewsletter.com on April 6, 2018 at 2:14 pmAccording to IDC Corp.‘s Worldwide Quarterly Converged Systems Tracker, worldwide converged systems market revenue increased 9.1% year over year to $3.6 billion during 4Q17.

Full-year sales surpassed $12.5 billion, representing a 9.4% increase over the previous year and the first time the market surpassed $12 billion in a calendar year.

“The number of organizations deploying converged systems continued to expand through 2017,” said Eric Sheppard, research VP, enterprise servers and storage. “This drove the total market value past $12.5 billion for the year. While not all market segments increased during the year, those that did grow were able to provide considerable benefits related to the most core infrastructure challenges facing today’s data centers.”

Converged Systems Segments

IDC’s converged systems market view offers three segments: certified reference systems and integrated infrastructure, integrated platforms, and hyperconverged systems.

Certified reference systems and integrated infrastructure are pre-integrated, vendor-certified systems containing server hardware, disk storage systems, networking equipment, and basic element/systems management software.

Integrated platforms are integrated systems that are sold with additional pre-integrated packaged software and customized system engineering optimized to enable such functions as application development software, databases, testing, and integration tools.

Hyperconverged systems collapse core storage and compute functionality into a single, highly virtualized solution. A key characteristic of hyperconverged systems that differentiate these solutions from other integrated systems is their scale-out architecture and their ability to provide all compute and storage functions through the same x86 server-based resources.

Market values for all three segments includes hardware and software but excludes services and support.

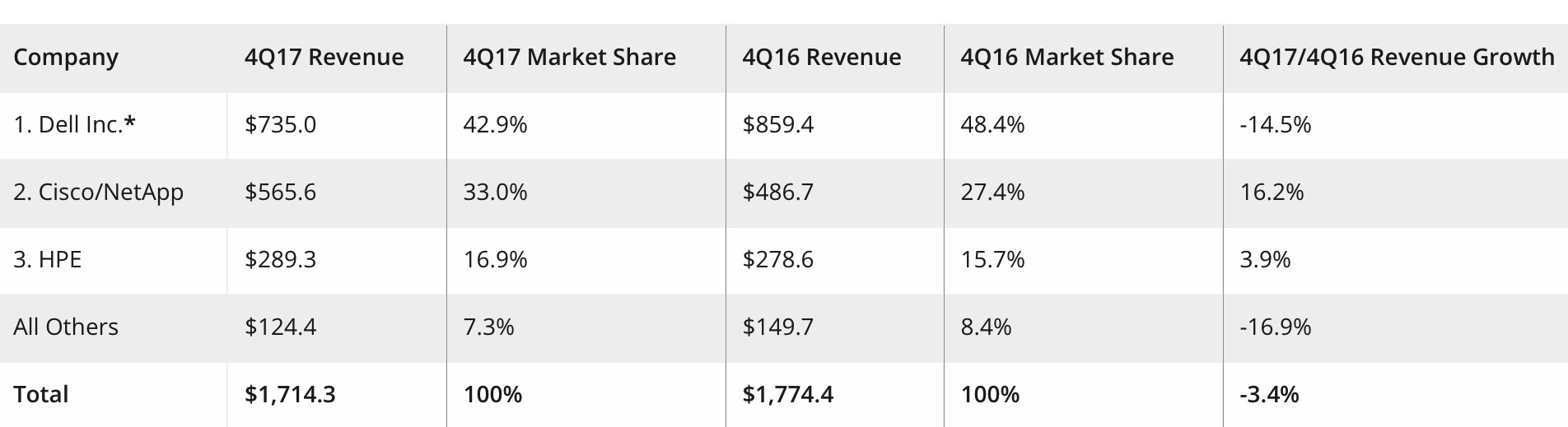

The certified reference systems and integrated infrastructure market generated $1.7 billion in revenue during 4Q17, which represents a 3.4% Y/Y decline and 47.1% of the total converged systems market value. Dell Inc. was the largest supplier in this market segment with $735.0 million in sales and a 42.9% share. Cisco/NetApp generated $565.6 million in sales, which was the second largest share at 33.0%. HPE generated $289.3 million in sales and captured 16.9% market share.

Top 3 Companies, WW Certified Reference Systems and Integrated Infrastructure, 4Q17

(revenue in $million)

Click to enlarge

Revenue from hyperconverged systems sales grew 69.4% year over year to $1.25 billion during the fourth quarter of 2017. This amounted to 34.3% of the total converged systems market. Full-year sales of hyperconverged systems surpassed $3.7 billion in 2017, up 64.3% from 2016.

IDC offers two ways to rank technology suppliers within the hyperconverged systems market: by the brand of the hyperconverged solution or by the owner of the software providing the core hyperconverged capabilities.

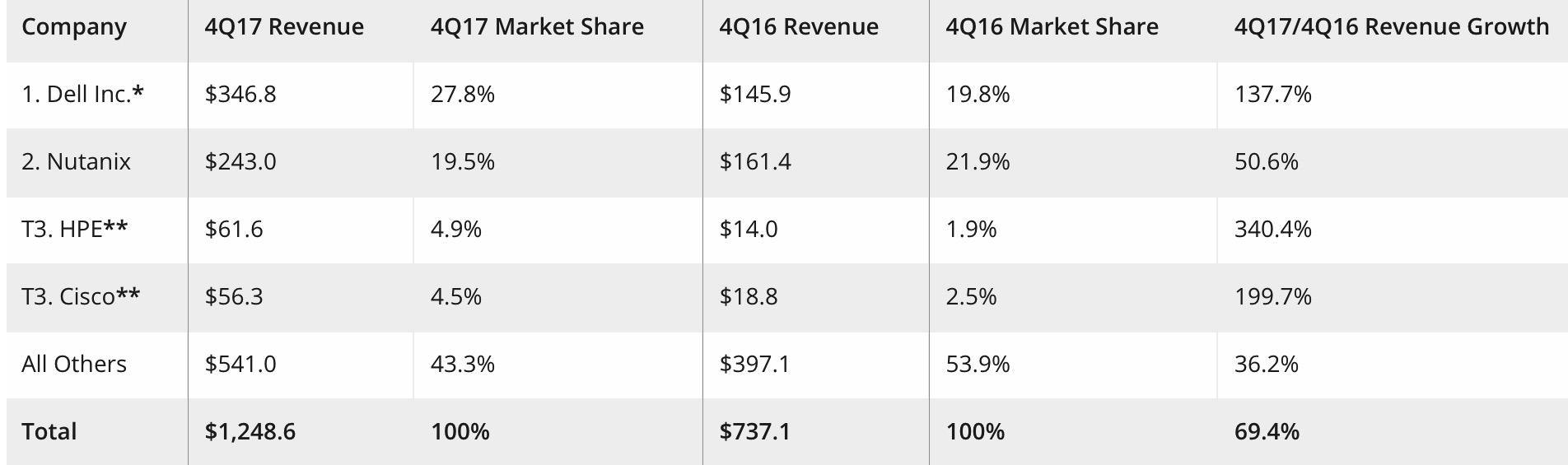

In the branded solution view, Dell Inc. was the largest supplier in this market segment with $346.8 million in revenue and a 27.8% share. Nutanix generated $243.0 million in revenue with the second largest share of 19.5%. HPE and Cisco were statistically tied** for the quarter, with $61.6 million and $56.3 million in revenue and 4.9% and 4.5% market share, respectively.

Top 3 Companies, WW Hyperconverged Systems, Based on Brand of HCI Solution, 4Q17

(revenue in $million)

Click to enlarge

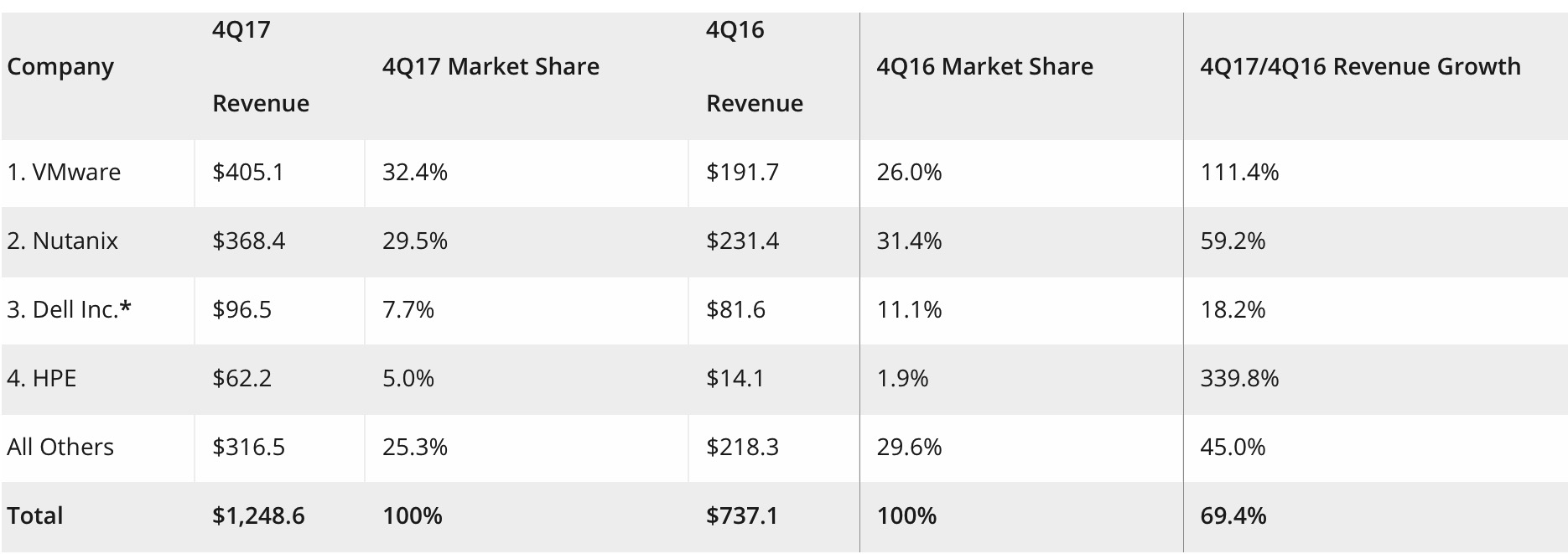

On the basis of HCI software, systems running VMware’s hyperconverged software represented $405.1 million in fourth quarter vendor revenue, or 32.4% of the total market segment. Systems running Nutanix’s hyperconverged software represented $368.4 million in fourth quarter vendor revenue, or 29.5% of the total market segment. Both values represent all software and hardware, regardless of how it was ultimately branded.

Top 4 Companies, WW Hyperconverged Systems, Based on Owner of HCI Software, 4Q17

(revenue in $million)

Click to enlarge

Notes:

* Dell Inc. represents the combined revenues for Dell and EMC sales for all quarters shown.

** IDC declares a statistical tie in the worldwide converged systems market when there is a difference of 1% or less in the revenue share of two or more vendors.

Integrated platforms sales declined 18.1% year over year during 4Q17, generating revenues of $675.5 million. This amounted to 18.6% of the total converged systems market value. Oracle was the top-ranked supplier of integrated platforms during the quarter, generating revenues of $360.5 million and capturing a 53.4% share of the market segment.

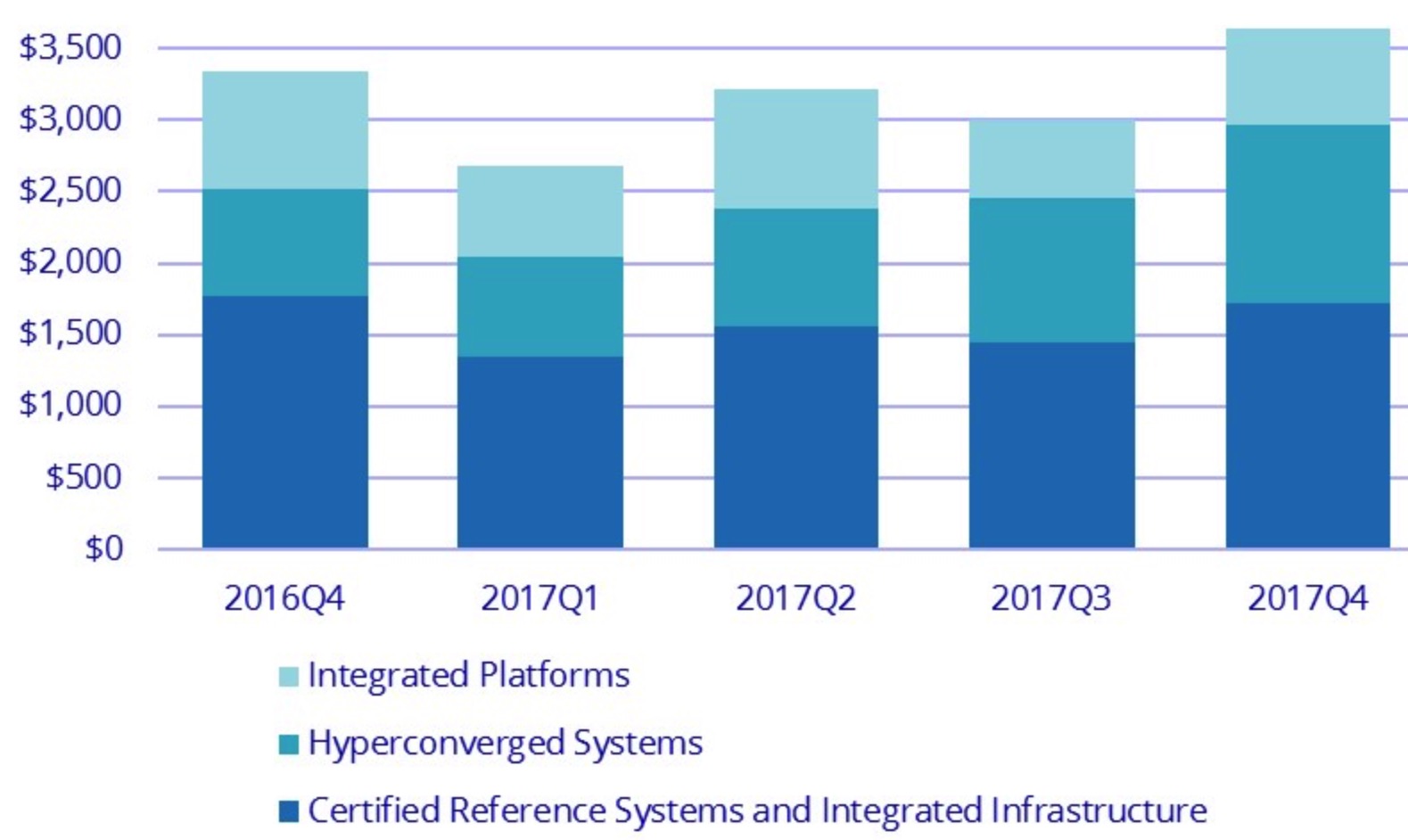

WW Converged Systems Market by Product Category, 4Q17 Vendor Revenue

Taxonomy Notes

IDC defines converged systems as pre-integrated, vendor-certified systems containing server hardware, disk storage systems, networking equipment, and basic element/systems management software. Systems not sold with all four of these components are not counted within this tracker. Specific to management software, IDC includes embedded or integrated management and control software optimized for the auto discovery, provisioning and pooling of physical and virtual compute, storage and networking resources shipped as part of the core, standard integrated system. Numbers in this press release may not sum due to rounding.

Read also:

WW Converged Systems Revenue Increased 11% Y/Y in 3Q17 at $3 Billion – IDC

Top vendors: Dell, Nutanix, Cisco and HPE

2017.12.26 | Press Release

WW Converged Systems Revenue Increased 6.2% Y/Y in 2Q17 – IDC

Vendor sales at $3.15 billion, HPE sharply down

2017.09.29 | Press Release

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter