Oracle: Fiscal 4Q26 and FY26 Financial Results

Generating $67.4 billion, up 17% YoY

This is a Press Release edited by StorageNewsletter.com on June 12, 2026 at 2:01 pmSummary:

- Record Remaining Performance Obligations grew $85 billion in Q4 from $553 billion to $638 billion

- Record Q4 Earnings per Share GAAP up 21% USD to $1.45, non-GAAP up 24% USD to $2.111

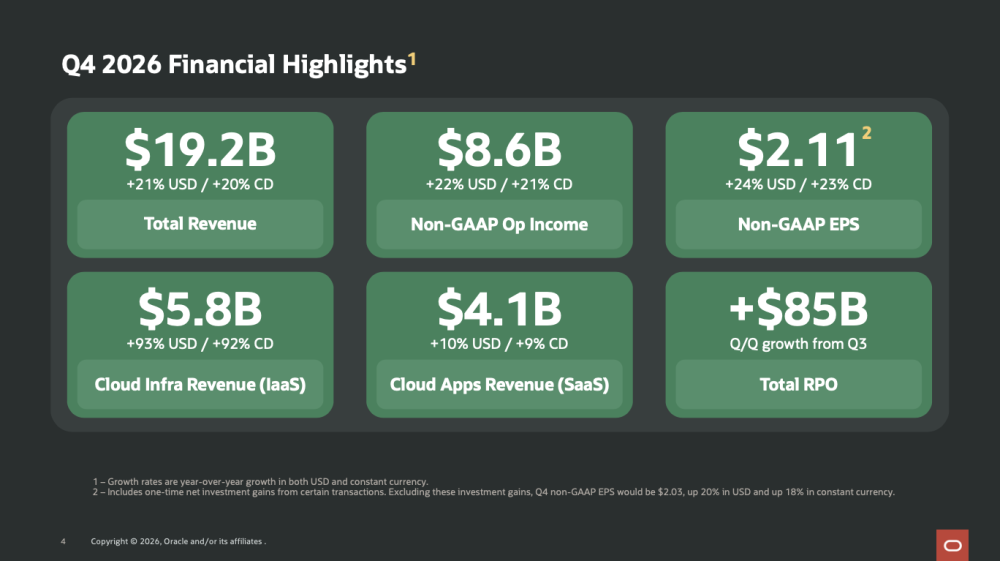

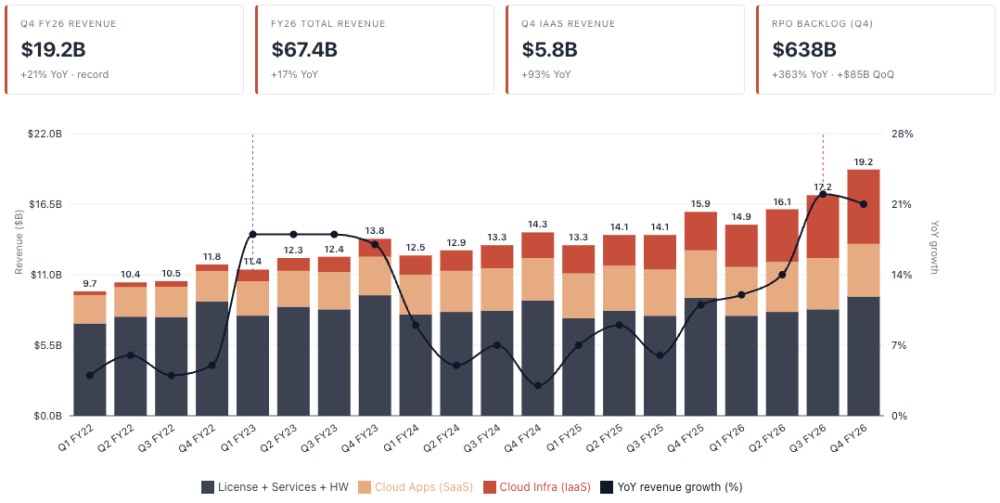

- Record Q4 Total Revenues $19.2 billion, up 21% USD, and up 20% constant currency

- Record Q4 Total Cloud Revenues $9.9 billion, up 47% USD, and up 46% constant currency

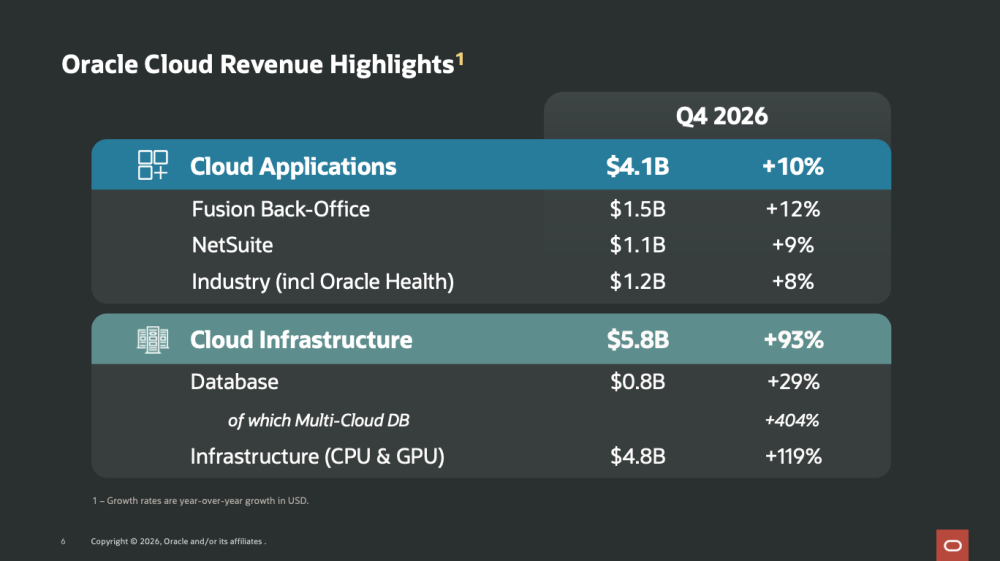

- Q4 Cloud Infra (IaaS) Revenue $5.8 billion, up 93% USD, and up 92% constant currency

- Q4 Cloud Apps (SaaS) Revenue $4.1 billion, up 10% USD, and up 9% constant currency

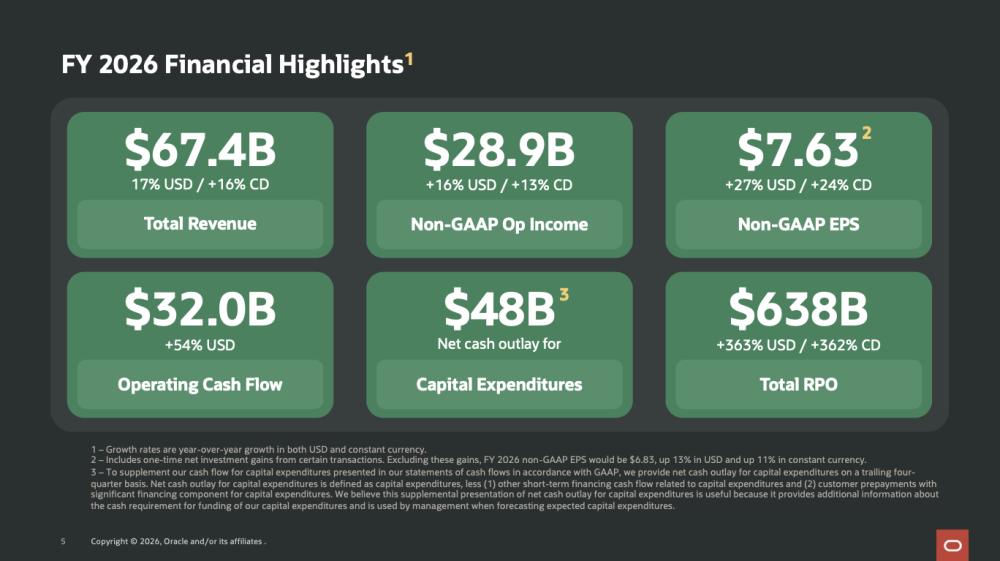

- Record FY 2026 Earnings per Share GAAP up 34% USD to $5.83, non-GAAP up 27% USD to $7.631

- Record FY 2026 Total Revenues $67.4 billion, up 17% USD, and up 16% constant currency

- Record FY 2026 Total Cloud Revenues $34.0 billion, up 39% USD, and up 37% constant currency

- FY 2026 Cloud Infra (IaaS) Revenue $18.1 billion, up 77% USD, and up 75% constant currency

- FY 2026 Cloud Apps (SaaS) Revenue $15.9 billion, up 11% USD, and up 10% constant currency

Oracle Corp. announced another record quarter with strong revenue growth across its Cloud Infrastructure and Cloud Applications businesses.![]() Total quarterly revenues increased 21% to $19.2 billion, reflecting broad-based demand for Oracle’s industry-leading cloud technology and applications suites. Cloud revenues (IaaS + SaaS) increased 47% to $9.9 billion driven by 93% growth in Cloud Infrastructure (IaaS), and 10% growth in Cloud Applications (SaaS). Software revenues were down 2% to $6.8 billion, reflecting our customers’ continuing migration from on-premise software to the Cloud. Services revenues were $1.5 billion, up 13%, and Hardware revenues were $0.9 billion, up 9%.

Total quarterly revenues increased 21% to $19.2 billion, reflecting broad-based demand for Oracle’s industry-leading cloud technology and applications suites. Cloud revenues (IaaS + SaaS) increased 47% to $9.9 billion driven by 93% growth in Cloud Infrastructure (IaaS), and 10% growth in Cloud Applications (SaaS). Software revenues were down 2% to $6.8 billion, reflecting our customers’ continuing migration from on-premise software to the Cloud. Services revenues were $1.5 billion, up 13%, and Hardware revenues were $0.9 billion, up 9%.

Oracle generated Q4 GAAP operating income of $6.1 billion, up 20%, while non-GAAP operating income rose to a record $8.6 billion, up 22%, driven by strong revenue growth and operating efficiency actions taken during the quarter. GAAP net income available to common shareholders reached $4.2 billion, up 23%, and non-GAAP net income available to common shareholders grew to $6.2 billion, up 26%. Q4 GAAP earnings per share increased to $1.45, up 21%, and non-GAAP earnings per share climbed to $2.111, up 24%.

Click to enlarge

Financial Results for FY 2026

Fiscal year 2026 total revenues were up 17% to a record $67.4 billion. Cloud revenues increased 39% to $34.0 billion. Software revenues were down 1% to $24.5 billion. Services revenues were $5.7 billion, up 10%, and Hardware revenues were $3.1 billion, up 5%.

Fiscal year 2026 GAAP operating income was $20.6 billion, up 17%, and non-GAAP operating income rose to a record $28.9 billion, up 16%. GAAP net income available to common shareholders reached $17.0 billion, up 36%, while non-GAAP net income available to common shareholders grew to $22.2 billion, up 29%. GAAP earnings per share increased to $5.83, up 34%, while non-GAAP earnings per share climbed to $7.631, up 27%.

Oracle’s strong operating income translated to record fiscal year operating cash flow of $32.0 billion, up 54%. Free cash flow was negative $23.7 billion for fiscal year 2026 as Oracle continued to execute on investments to support the growth of its Cloud Infrastructure business.

Click to enlarge

Click to enlarge

Remaining Performance Obligations

Remaining Performance Obligations, or RPO, ended the quarter at $638 billion, up 363% USD year-over-year and up $85 billion sequentially from the end of Q3.

Most of the RPO increase in both Q3 and Q4 were large scale AI contracts where the customer prepaid Oracle for the purchase of the GPUs, or the customer bought and supplied the GPUs to Oracle. The prepaid and customer supplied hardware portions of our large AI contracts now total $75 billion. This substantially reduces the amount of capital Oracle must raise to build out our AI datacenters.

Capital Investment Program and Capital Funding

Oracle’s capital investment program supports the pursuit of unprecedented opportunities in AI Cloud Infrastructure as described at our most recent Financial Analyst Meeting. In fiscal year 2026, Oracle raised $43 billion in debt financing and $5 billion in equity financing. In fiscal year 2027, Oracle expects to raise approximately $40 billion through a combination of debt and equity financing including its previously announced $20 billion at-the-market equity issuance. Oracle does not expect to issue additional debt in calendar year 2026.

Guidance for Q1 FY 2027

Oracle is providing the following forward-looking guidance for Q1 FY 2027:

- Total Revenues are expected to grow from 27% to 29% in both constant currency and USD

- Total Cloud revenue is expected to grow between 57% and 63% in constant currency and is expected to grow between 58% and 64% in USD

- Non-GAAP earnings per share is expected to grow between 16% and 19% and be between $1.71 and $1.75 in constant currency and grow between 17% and 20% and be between $1.72 and $1.76 in USD

Guidance for Full FY 2027

For fiscal year 2027, we confirm our prior revenue guidance of $90 billion total revenue and raise our non-GAAP EPS guidance to $8.05, which is growth of 18%1 after adjusting for the one-time events of selling our Ampere chip business and Bloom Energy warrants in fiscal year 2026.

AI Market and Technology Evolution

The large increases in Oracle’s RPO and revenue are driven by the growing demand for cloud infrastructure for AI training and inferencing. Oracle is building datacenters that are intended to use clean energy from natural gas fuel cells to generate electricity with minimal emissions. Other innovations in the areas of high-performance networking, advanced security and autonomous software have made Oracle the world’s fastest growing provider of cloud datacenters.

Our database and applications businesses are both benefiting from Oracle’s early adoption of AI. The Oracle Multicloud AI Database grew 404% in Q4—making it our fastest growing business ever. The Oracle Health application suite will soon include a completely new AI version of the Cerner hospital and clinic patient care management system. We expect this new AI patient care management system to push the growth rate of the overall Oracle Health business to double-digits in fiscal year 2027. And this is just the beginning of the expansion of the Oracle Health business.

We believe AI is about to completely revolutionize healthcare. Improvements in patient care are expected to yield much better patient outcomes, while dramatically lowering the cost of healthcare throughout the world. Oracle Health AI systems will allow doctors to spend less time with computers and more time with patients. AI molecular design models are expected to enable researchers to accelerate the development of life-saving drugs. Oracle’s new AI clinical trial system is designed to enable regulators to rapidly review and approve clinical trial test results enabling patients to get access to new drugs sooner. AI will make healthcare better, more accessible, and less expensive.

Common Stock Quarterly Dividend

The board of directors declared a quarterly cash dividend of $0.50 per share of outstanding common stock. This dividend will be paid to stockholders of record as of the close of business on July 10, 2026, with a payment date of July 24, 2026.

Footnotes

1 Q4 and FY 2026 results include one-time net investment gains from certain transactions. Excluding these investment gains, Q4 non-GAAP EPS would be $2.03, up 20% in USD and up 18% in constant currency and FY 2026 non-GAAP EPS would be $6.83, up 13% in USD and up 11% in constant currency. Excluding these same investment gains, FY 2027 non-GAAP EPS growth would be 18%.

Comments

Always interesting to see the trajectory of Oracle as Larry Ellison was against the Cloud for several years arguing and promoting on-premise IT first model during famous keynote during Oracle conferences. For obvious reasons, the cloud impacted seriously its database license revenue. Oracle today is far away from the company image we had in our head for decades.

Oracle closed fiscal year 2026 on June 10, 2026 with a quarter that crystallized its transformation from database-and-applications incumbent into a top-tier AI infrastructure provider, and simultaneously illustrated the financial cost of that transformation. The headline numbers were strong enough to beat consensus on both revenue and EPS, yet the stock fell roughly 7% after-hours and closed down about 5% the following session, as investors digested capex that overshot guidance, a 48% surge in total liabilities, and a renewed funding round.

Total Q4 revenue reached $19.2B, up 21% sequentially, driven almost entirely by cloud. Total cloud revenue (IaaS + SaaS) grew 47% to $9.9B, with the split heavily skewed toward infrastructure:

- Cloud Infrastructure (IaaS): $5.8B, +93%, including CPU & GPU revenue of $4.8B, up 119% YoY, and database revenue of $0.8B, of which multicloud DB grew an extraordinary +404%

- Cloud Applications (SaaS): $4.1B, +10%, Fusion Back-Office $1.5B (+12%), NetSuite $1.1B (+9%), Industry (incl. Oracle Health) $1.2B (+8%).

Software revenue declined 2% to $6.8B (continued migration to cloud); Services $1.5B (+13%); Hardware $0.9B (+9%), the image below summarizes all revenue segments.

Remaining Performance Obligations grew $85B sequentially in Q4 alone, from $553B to $638B, up 363% YoY. Oracle's AI backlog now exceeds those of Microsoft, AWS, and Google individually, a remarkable repositioning for a company that wasn't considered a hyperscaler eighteen months ago. What a shift.

Oracle added 1.2GW of incremental data center capacity in FY26 and signaled nearly another 1GW coming in Q1 FY27, with major sites at Abilene, TX; Shackleford, TX; Doña Ana, NM; Saline, MI; and Port Washington, WI. The Abilene flagship, the centerpiece of the Stargate joint effort with OpenAI and SoftBank, has reportedly delivered 42% of contracted capacity, with another 35% due in the next quarter. The earnings presentation shows impressive photos of the progress of these DCs implementations and developments.

Two operational metrics, extracted from the presentation associated with the earnings PR, are worth flagging for storage and infrastructure readers: AI infrastructure utilization: 97.5% and AI data center capacity already under contract: 98%.

Some additional points that bring our attention: total liabilities, including debt, jumped 48% to $218.7B, the sharpest surge on record. Oracle's high-grade corporate bond stack is now estimated at roughly $117B, making it the largest non-financial issuer in the Bloomberg US investment-grade index. Five-year credit default swaps remain at elevated levels, and Moody's previously flagged a trajectory toward 4x EBITDA leverage. At the FY27 capex high end, capital spending could roughly equal Oracle's projected $90B in revenue, an extraordinary ratio for a company at this scale. Again what a change for a historical giant ISV...

Click to enlarge

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter