SK hynix: Fiscal 3Q19 Financial Results

Sales down 40% Y/Y and up 6% Q/Q

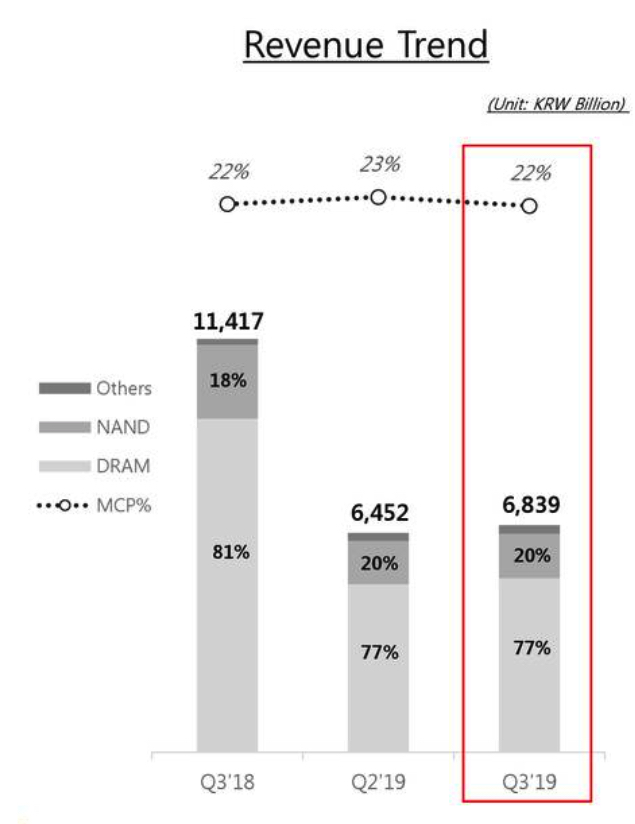

This is a Press Release edited by StorageNewsletter.com on October 28, 2019 at 1:38 pm| (in KRW billion) | 3Q18 | 3Q19 |

| Revenue | 11,417 | 6,839 |

| Growth | -40% | |

| Net income (loss) | 4,692 | 495 |

SK hynix Inc. announced financial results for its third quarter 2019 ended on September 30, 2019.

The consolidated third quarter revenue was 6.84 trillion won while the operating profit amounted to 473 billion won and the net income 495 billion won. Operating margin and net margin for the quarter was 7%.

The revenue in the third quarter increased by 6% Q/Q as demand began to pick up. However, the operating profit fell by 26% Q/Q as DRAM unit cost reduction was not enough to offset the price drop.

DRAM bit shipments increased by 23% Q/Q as the company responded to the new products in the mobile market and purchases from some data center customers also increased. DRAM prices remained weak during the quarter, leading to a 16% drop in the ASP, with the decline smaller than the previous quarter.

Although the company responded to the solution market, such as high-density mobile products and SSDs, where demand continues to recover, NAND flash bit shipments decreased by 1% Q/Q because the company cut back raw NAND sales that was temporarily increased in the last quarter. It also resulted in a 4% increase in the ASP as raw NAND is relatively cheap.

SK hynix plans to develop production and investment strategy to meet growing customer demands as well as effectively deal with demand fluctuations due to external uncertainties.

The company is converting part of the DRAM production lines of its M10 FAB in Icheon, Korea, to CMOS image sensor (CIS) mass production lines, while reducing 2D NAND flash wafer capacity. As a result, both DRAM and NAND flash capacity will decrease next year compared to this year, and the amount of investment is expected to shrink considerably next year as well.

SK hynix will continue to focus on technology migration and expand sales of high-density, high-value-added products in order to achieve greater growth when the market improves.

The company intends to increase the proportion of 1Ynm DRAM in the product portfolio to early 10% by the end of this year and prepare for mass production of the recently developed 1Znm DRAM products. In addition, the company plans to actively respond to the LPDDR5 and HBM2E markets, both of which are expected to be increasingly adopted by customers next year.

For NAND flash, SK hynix will increase the proportion of 96-layer 4D NAND products to more than mid-10% by the end of this year, while preparing for mass production and sales of 128-layer 4D NAND flash. As the company will focus on the high-end smartphone and SSD markets, SSD is expected to account for around 30% of the company’s NAND flash sales next quarter.

Comments

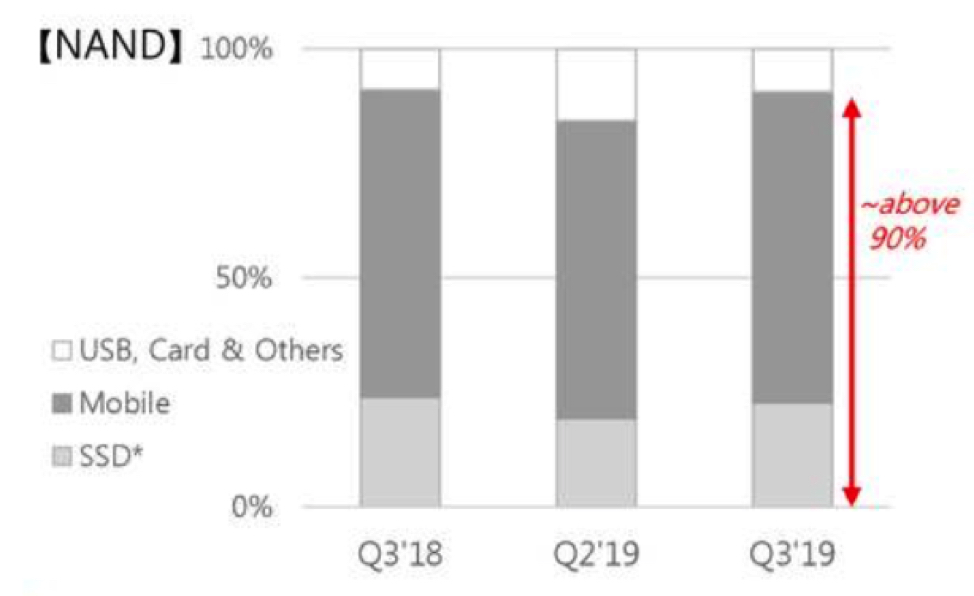

For NAND

Sales grew for both DRAM and NAND driven by signs of demand recovery and slowdown in the price decline.

In the NAND market, there is shipment growth in PC and smartphone and elastic demand recovery is speeding in 3Q19 grew nearly 50% Y/Y. As the firm saw mid 20% growth Y/Y in SSD shipment for PCs, an increase in the average NAND content in the SSD with a high 20% adoption of 500GB or a higher content.

SK hynix will focus on the high-density NAND market such as high-end smartphones and PCIe SSDs, which is likely to raise its SSD revenue mix to 30% in 4FQ19.

In light of the current environment, where demand continues to grow DRAM bit shipment in 4FQ19, the vendor expects to increase by mid-single-digit percentage and NAND bit shipment is expected to increase by around 10% level.

For the company's FY19, DRAM bit shipment is expected to grow by high 10% level, thanks to the higher than planned performance in 3Q19. NAND bit shipment growth is expected to reach around 50% level.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter