Western Digital: Fiscal 2Q19 Financial Results

Sales down sharply: -16% Q/Q and -21% Y/Y

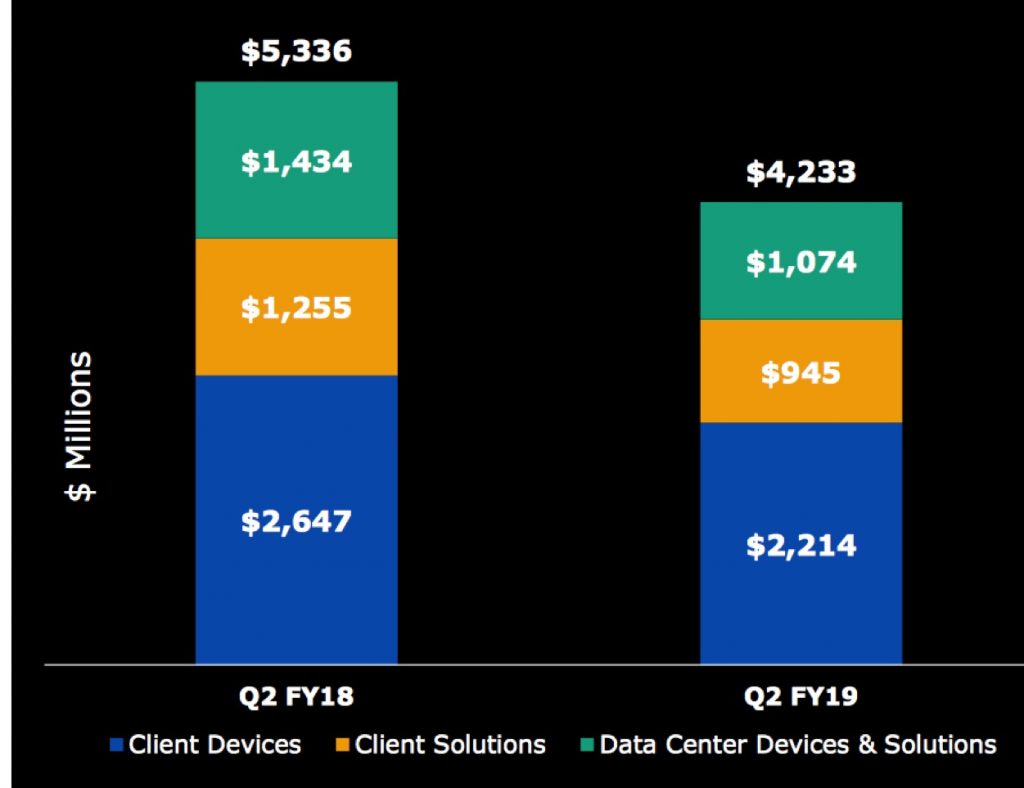

This is a Press Release edited by StorageNewsletter.com on January 28, 2019 at 2:16 pm| (in $ million) | 2Q18 | 2Q19 | 6 mo. 18 | 6 mo. 19 |

| Revenue | 5,336 | 4,233 | 10,517 | 9,261 |

| Growth | -21% | -21% | ||

| Net income (loss) | (823) | (487) | (142) | 24 |

Western Digital Corp. reported revenue of $4.2 billion for its second fiscal quarter ended December 28, 2018.

Operating income was $176 million with a net loss of $487 million, or ($1.68) per share. Excluding certain non-GAAP adjustments, the company achieved non-GAAP operating income of $589 million and non-GAAP net income of $424 million, or $1.45 per share.

In the year-ago quarter, the company reported revenue of $5.3 billion, operating income of $955 million and net loss of $823 million, or ($2.78) per share. Non-GAAP operating income in the year-ago quarter was $1.4 billion and non-GAAP net income was $1.2 billion, or $3.95 per share.

The firm generated $469 million in cash from operations during the second fiscal quarter of 2019, ending with $4.1 billion of total cash, cash equivalents and available-for-sale securities. It returned $144 million to shareholders through dividends and repaid the outstanding balance on its revolver of $500 million. On November 7, 2018, it declared a cash dividend of $0.50 per share of its common stock, which was paid to shareholders on January 14, 2019.

“Despite a softening business environment, our fiscal second quarter results were generally within our guidance ranges,” said Steve Milligan, CEO. “We are taking actions to better align our cost and expense structure to near-term business conditions while continuing to deliver innovative solutions to drive our future success. We enter calendar 2019 with the strongest product portfolio in our history and confidence in our ability to capitalize on the long-term opportunities associated with data growth.”

Comments

Revenue mix

Revenue declined strongly (-21% y/y and Q/Q to $4.23 billion) but it was expected by the company saying last quarter that it will be between $4.2 billion to $4.4 billion, so finally at the lower end of the guidance range and missing Wall Street's estimates of $4.26 billion.

But for next quarter, it will be worst as guidance of WD is between $3.6 and $3.8 billion (-15% to -11%)

Why this large decline in 2FQ19? Two reasons: weakness in NAND pricing and decline in HDD volumes.

HDD and SSD revenue

| in $ million | 1Q18 | 1Q19 | 2Q19 |

Y/Y % Growth |

| HDD |

2,610 | 2,494 | 2,060 | -22% |

| SSD |

2,571 | 2,534 | 2,173 | -15% |

Flash

Revenue was $2.2 billion with a sequential bit growth of 5% and a sequential ASP per gigabyte declined of 18%.

HDD

Revenue was $2 billion. The vendor shipped 75.9EB, a 17% sequential decline and the lower figure since 3FQ17, and 30.2 million HDDs, lower result since at least 2FQ15, with ASPs falling $5 Q/Q to $67.

But WD forecasts robust long-term demand for storage with capacity enterprise exabyte growth at ~40% CAGR.

For client solutions, there was an aggressive pricing environment for both flash and HDD products but a strong Y/Y increase in average capacities for both of them.

For client devices the firm recorded a strong growth in SSD revenue but a weak demand for mobility and embedded applications as well as flash pricing pressure.

For the third fiscal quarter demand for WD's products is expected to be affected by many factors including reduced demand for mobile handsets, a continued slowdown investments by hyperscale customer’s inventory adjustments at certain customers, and geopolitical volatility.

What's doing WD in face of these bad trends? CEO Steve Milligan said: "We are taking actions to better align our cost and expense structure to near-term business conditions while continuing to deliver innovative solutions to drive our future success."

Volume and HDD Share for Fiscal Quarters

(units in million)

| Client compute units (1) |

Non-compute units (2) |

Data centers units (3) |

Total HDDs (4) |

Exabyte Shipped |

ASP (5) |

|

| 2Q18 |

21.1 | 14.4 | 6;8 | 42.3 |

$63 | |

| 3Q18 |

17.6 | 11.2 | 7.6 | 36.4 |

$72 | |

| 4Q18 |

17.8 | 13.7 | 7.5 | 39.0 |

$70 | |

| 1Q19 | 16.3 | 11.2 | 6.6 | 34.1 | 103.3 | $72 |

| 2Q19 |

14.0 | 11.1 |

5.1 |

30.2 |

75.9* |

$67 |

(1) Client compute products consist primarily of desktop and notebook HDDs, excluding those sold through retail channels.

(2) Non-compute products consist of retail channel and consumer electronics HDDs.

(3) Data center products consist of enterprise HDDs (high-capacity and performance) and enterprise systems.

(4) HDD unit volume excludes data storage systems and media.

(5) HDD ASP is calculated by dividing HDD revenue by HDD units. Data storage systems are excluded from this calculation, as data storage systems ASP is measured on a per system basis rather than a per drive basis.

Abstract of the earnings call transcript:

Steve Milligan, CEO:

"In flash, we continue to lead the industry's transition to 96 layer BiCS4 technology. We expect broad implementation of this technology across our product portfolio in calendar 2019. We have 96 layer products in customer hands today.

"In the December quarter of calendar 2019, we expect BiCS4 to achieve BiCS mix crossover with the BiCS3 from a supply standpoint.

"We will be shipping our mainstream client SSD based on BiCS4 in the March quarter.

"We have had an exceptionally smooth qualification process for our 14TB helium drive and expect customer qualification activities for this industry-leading offering to be completed at virtually all of our customers in the current quarter. We've already commenced revenue shipments for several customers.

"In flash, we are executing on the previously announced changes to our wafer output levels to reduce our bit supply growth for calendar 2019.

"We have accelerated the closure of our Kuala Lumpur HDD manufacturing facility by almost 3 quarters."

Mike Cordano, president and COO:

"For the data center we began qualifications of our NVMe SSD product in the December quarter and due to stronger customer pull we expect to ramp this product for the meaningful revenue by the middle of this calendar year.

"We previously announced the reduction to wafer starts for a proportion of the flash joint venture (with Toshiba) along with the way deployment of the capital equipment. The magnitude of these actions is a planned reduction of 10% to 15% of our bid output in calendar 2019.

"We grew up presence in client SSDs during the quarter and delivered solid performance on differentiated form factor devices such as iXpand.

"We achieved excellent momentum in our client SSD portfolio in the quarter. Average capacity for client SSD grew over 60% Y/Y in the December quarter of fueled by an increase mix of our 512GB SSD at our key customers. For the first time our client compute SSD revenue exceeded client compute HDD revenue.

"We are pleased to have commenced product sampling of our first generation energy-assisted 16TB drive and we are on-track to begin revenue shipments of this 8-platter solution later this calendar year.

"In terms of the exabyte growth rate for capacity enterprise, as we previously stated we are seeing a moderation in the first half of calendar 2019. Based on our customer discussions we continue to forecast Y/Y growth to resume in the second half of calendar 2019.

"In data center systems we experienced excellent momentum with record quarterly bookings and new customer acquisitions in our IntelliFlash and ActiveScale portfolios. We also had record revenue in our Ultrastar portfolio of storage platform and servers."

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter