Some NAND and DRAM Pricing Impacts

Experiences from recent visits in Taipei and Tokyo

By Philippe Nicolas | May 12, 2026 at 2:01 pmDuring a recent trip to Taiwan and Japan, I visited several well-known electronics retail districts where consumer devices and components are sold.

What struck me was the visible impact AI demand is having on both DRAM and NAND markets, and by extension, on memory stick and SSD pricing at the retail level. The photos below offer a glimpse of this. You’ll notice that some prices aren’t even displayed; you have to ask for them, and they can shift between one inquiry and the next, even within a few hours.

Click to enlarge

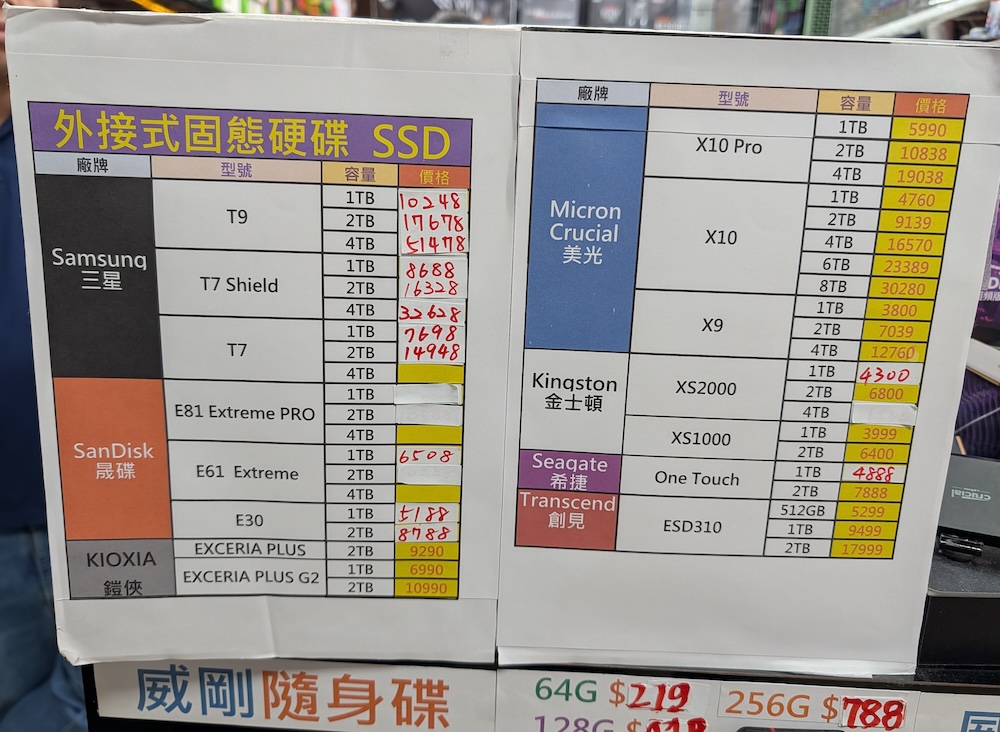

To put this in perspective, I purchased a Samsung T7 2TB in Paris for €150 back in September 2022. The photo below shows the Samsung T7 priced at TWD 7,698 for the 1TB and TWD 14,948 for the 2TB, with the 4TB model not even listed. The Samsung T9 runs slightly higher for the 1TB and 2TB, but the 4TB jumps dramatically to TWD 51,478. Converted into €/TB and $/TB, that works out to €207 or $244 for the 1TB, €202 or $237 for the 2TB, and €350 or $408 for the 4TB.

Given the NAND and SSD pricing trajectory prior to 2022, one would have expected the Samsung T7 2TB to have dropped to somewhere around €51–65 by now. Instead, it sits at €403 or $473 — 2.69× what I paid nearly four years ago, and between 6.2× and 7.9× the price we might have anticipated. It’s a striking illustration of the extraordinary pricing environment we’re currently living through. And if we look at the Samsung T9 4TB, the listed price comes to €1,390 or $1,632. I’m not even factoring in currency fluctuations over that period.

We’ll let you explore the other prices visible in the accompanying images where available.

Click to enlarge

Click to enlarge

On the DRAM side, prices for 8GB, 16GB, and 32GB modules are staggeringly high when measured against pre-crisis levels.

Click to enlarge

Since AI has permeated virtually every sector, enterprises are finding that project components and other critical infrastructure elements have become extraordinarily expensive. Several vendors are clearly capitalizing on this environment, posting stellar revenues and remarkable margins. One notable side effect is an accelerating shift toward cloud adoption, as major cloud providers had already secured massive volumes of hardware and built out football-field-sized data centers well ahead of the current squeeze.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter