2Q24 NAND Flash Contract Prices Expected to Rise by 13-18%

Enterprise SSDs to see highest increase

This is a Press Release edited by StorageNewsletter.com on April 11, 2024 at 2:02 pm

Published on March 28, 2024, this market report was written by Bryan Ao, analyst, Trendforce Corp.

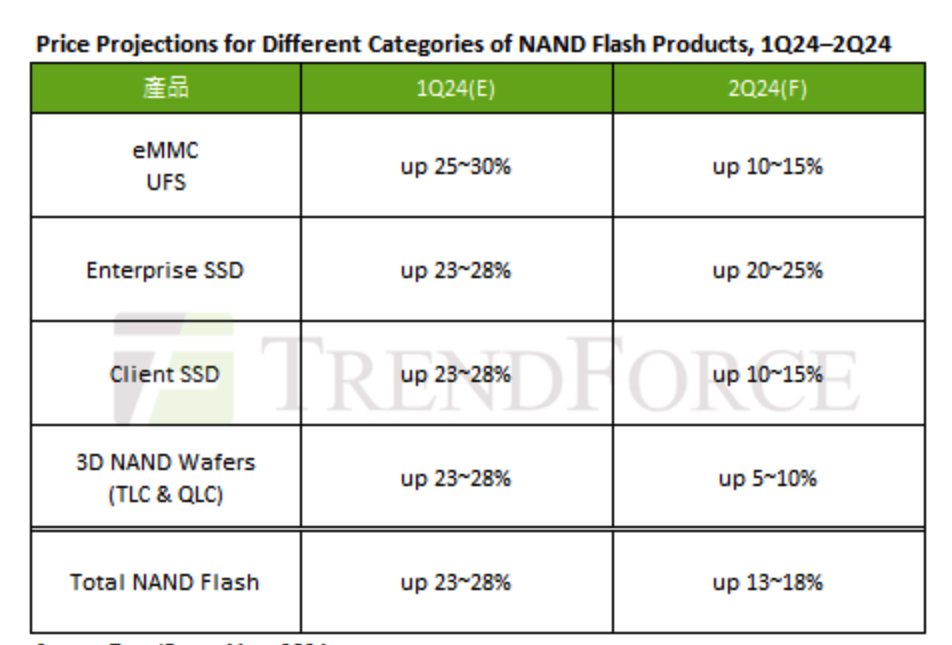

The report projects a strong 13–18% increase in 2Q24 NAND flash contract prices, with enterprise SSDs expected to rise highest. Despite Kioxia and WDC boosting their production capacity utilization rates from 1Q24, other suppliers have kept their production strategies conservative. The slight dip in 2Q24 NAND flash purchasing – compared to 1Q24 – does not detract from the overall market’s momentum, which continues to be influenced by decreasing supplier inventories and the impact of production cuts.

eMMC demand is predominantly driven by Chinese smartphone brands, leading to a substantial boost in shipments from Chinese module makers as some suppliers have reduced their supply. Buyers are increasingly adopting solutions from module makers to meet production needs, enhancing the technological advancement of Chinese module factories and their outreach to premier clients. This trend is likely to increase the penetration of eMMC products among smartphone customers, with a projected 10–15% rise in eMMC contract prices in 2Q24 due to a sharp rebound in NAND flash wafer prices.

The UFS market is buoyed by significant smartphone demand in India and Southeast Asia, supporting strong order momentum for UFS in the second quarter. Chinese smartphone brands are increasing their Q2 orders to ensure adequate inventory levels, bolstering demand. Suppliers aiming to reach their break-even targets promptly are expected to push UFS contract prices up by 10–15% in Q2.

Enterprise SSDs benefit from rising demand from CSPs in North America and China, with purchasing volumes expected to grow Q/Q in 1H24. With large-capacity SSD orders experiencing low order fill rates, suppliers continue to influence price trends, likely forcing buyers to accept higher prices. As some buyers attempt to increase their inventory levels before the peak season in 2H24, enterprise SSD contract prices are forecast to jump by 20–25% in 2Q24 — marking the highest rise across all product lines.

Client SSDs are seeing a more cautious buying strategy due to the off-season in-end sales, with some PC OEMs cutting their 2Q24 orders. The rapid price rebound will likely curb the growth of orders in 2H24, with PC client SSD 2Q24 contract price increases projected to be less than those of enterprise SSDs, at about 10–15%.

Post-Lunar New Year sales have continued to decline for NAND flash wafers as downstream customers show no need for stockpiling. However, the price increase has led suppliers to fail to meet orders from Chinese smartphone brands, causing a shift to module makers. As a result, Chinese module makers continue to maintain high inventory needs to expand cooperation with smartphone brands. With manufacturers keen on reaching profit targets quickly, NAND flash wafer contract prices continue to rise. Still, the increase is expected to be significantly more moderate than in 1Q24, estimated at 5–10% due to subdued demand in the retail market.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter