NAND Flash Contract Prices Forecast to Rise 15-20% in 1Q24

Thanks to supplier-led pricing

This is a Press Release edited by StorageNewsletter.com on January 16, 2024 at 2:01 pmThis market report was written by TrendForce Corp. on January 9, 2025.

NAND Flash Contract Prices Forecast to Rise 15-20% in 1Q24

Thanks to Supplier-Led Pricing

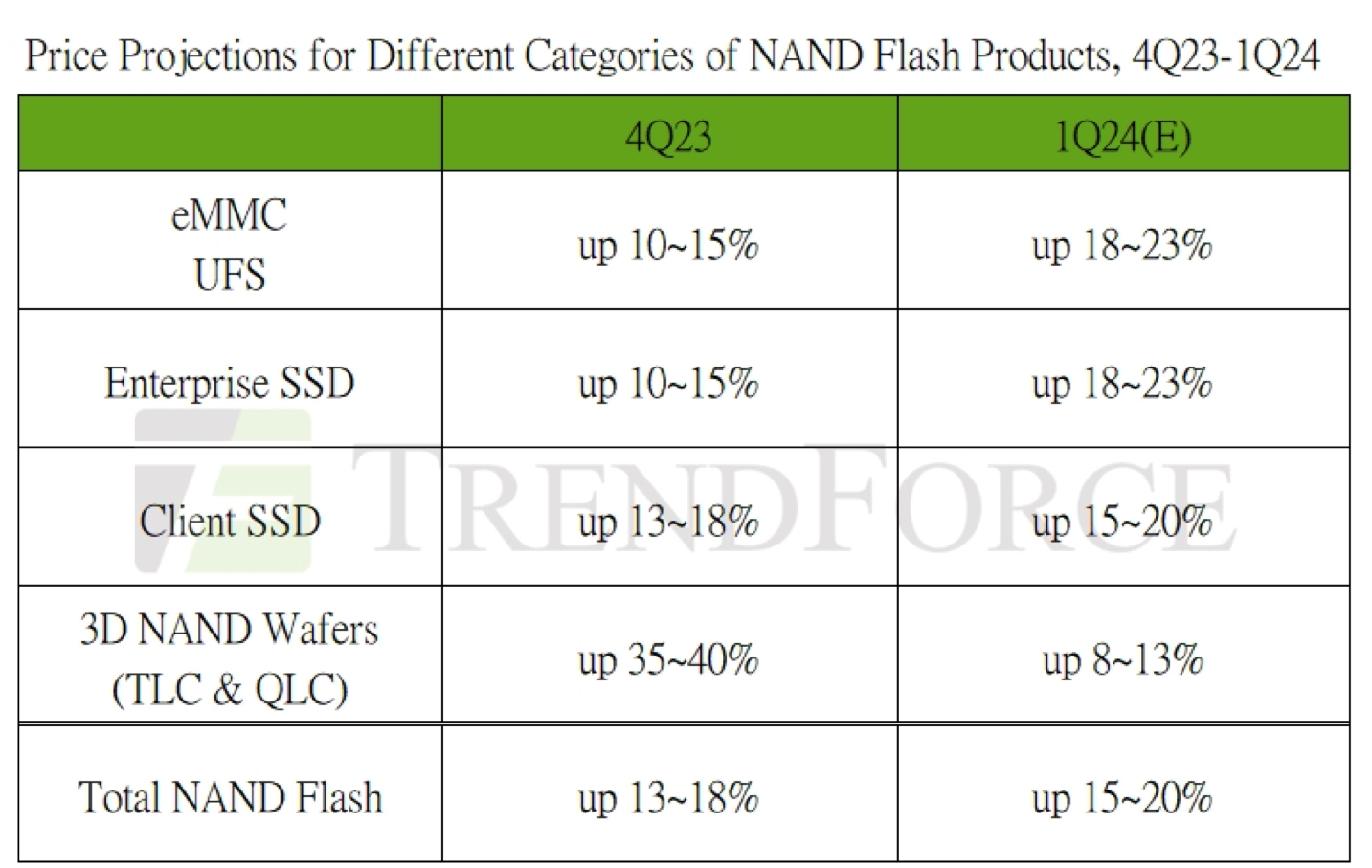

This research indicates that despite facing a traditional low-demand season, buyers are continuing to increase their purchases of NAND Flash products to establish safe inventory levels. In response, suppliers, aiming to minimize losses are pushing for higher prices, leading to an estimated 15-20% increase in NAND flash contract prices in 1Q24.

A key point to note is the aggressive price hike initiated by NAND flash manufacturers to offset losses. But, with demand struggling to keep pace with these rapid increases, future price escalations hinge on the resurgence of enterprise SSD procurement. The 1Q24 will see varied production strategies among suppliers, with some ramping up output early. This could lead to added pressure if anticipated demand growth falls short, potentially moderating price hikes in 2H24.

Client SSDs: PC OEMs are expected to hit a purchasing peak in 1Q24. As PCIe 4.0 SSDs gain traction, suppliers are upgrading processes and locking in sizeable bit orders. In a bid to balance their books, they’re markedly raising prices for PCIe 4.0 products, making acceptance of these new rates more likely for notebook clients. This sets the stage for a projected 15-20% jump in PC client SSD contract prices.

Enterprise SSD: Demand from North American CSPs has yet to spike, but Chinese CSPs and server brands are filling in the gap, keeping 1Q24 market unexpectedly buoyant. Overall, buyers’ rush to beef up their orders and suppliers’ firm pricing strategies are expected to catapult enterprise SSD contract prices by about 18-23% for 1Q24.

eMMC: The eMMC sector is also witnessing a price revolution, with demand from smartphones and Chromebooks stabilizing. Manufacturers and fabs are boldly hiking eMMC prices. Persistent production cuts have tightened the supply of smaller capacity products, forcing buyers to accept these price increases to prevent shortages. Consequently, eMMC prices are skyrocketing, with increases across all capacities and applications anticipated to exceed 20%. 1Q24 is set to see an eMMC contract price hike of about 18-23%.

UFS: Manufacturers are throttling supply and aggressively raising prices, leading to critically low smartphone client inventories, especially for the highly sought-after UFS 4.0. To counteract this scarcity, smartphone OEMs are expanding their orders to ensure robust inventory levels. With a limited number of suppliers for UFS 4.0 and a significant spike in wafer contract prices in late 2023, manufacturers are eager to reach a breakeven point swiftly. Despite sufficient seller inventory to meet market needs, all UFS series products are witnessing price jumps over 30%, leading to a forecast 18-23% increase in UFS contract prices for 1Q24, with the smartphone sector spearheading the rise.

NAND Flash Wafer: Due to a high short-term price surge and uncertain recovery in demand, module makers are offloading their wafer inventory to secure profits and sustain cash flow, diminishing buyers’ enthusiasm to pursue higher prices. Even though manufacturers plan to increase prices to boost profits, only a moderate increase of approximately 8-13% for NAND flash wafer contract prices is expected for 1Q24.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter