NAND Flash Contract Prices Projected to Climb 8~13% in 4Q23

As suppliers scale back production

This is a Press Release edited by StorageNewsletter.com on October 23, 2023 at 2:03 pmPublished on October 17, 2023, this market research was written by Bryan Ao and Sean Lin, analysts at TrendForce Corp.

Suppliers Scale Back Production

Q4 NAND Flash Contract Prices Projected to Climb 8~13%

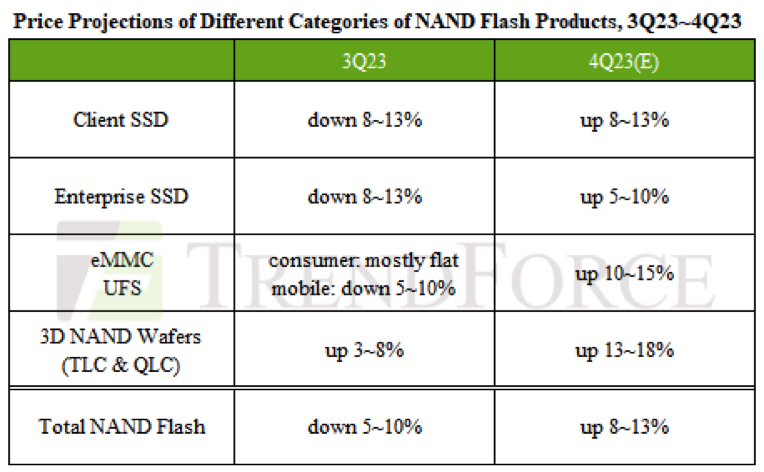

This research indicates a significant rise in NAND flash contract prices in 4Q23, with an anticipated hike of approximately 8~13%.

This increase has been largely attributed to stringent production controls exercised by suppliers. However, the outlook for 2024 suggests challenges in maintaining this upward price trajectory. The continuation of this rising trend hinges on persistently reducing output and the resurgence of demand for enterprise SSDs within the server market. Without solid demand, the momentum of this price surge could falter.

Client SSD

Active price increases by suppliers and module makers have motivated PC OEMs to stock up at relatively lower price points, leading to procurement volumes higher than actual demand. Suppliers aiming to expand bit shipments have launched promotions in 3Q23, leaving little room for further price declines for client SSDs. Meanwhile, reduced production of mainstream processes and fewer suppliers for high-end client SSDs have endowed suppliers with better bargaining power. Consequently, both high-end and low-end products are expected to increase concurrently, with 4Q23 PC client SSD contract prices projected to rise by 8~13%.

Enterprise SSD

North American CSPs still hold significant amounts of inventory, but demand from some server brands has recovered compared to 1H23, gradually increasing stocking momentum. In China, orders have picked up as CSPs’ inventories have dropped to reasonable levels, coupled with increased demand during the peak season for second-tier e-commerce vendors. Overall, procurement demand for enterprise SSDs in the fourth quarter is expected to grow. With NAND wafer prices leading the increase since August and suppliers adopting a firmer stance in negotiations, 4Q23 enterprise SSD contract prices are projected to rise by approximately 5~10%.

eMMC

The 2H23 primarily relies on TV shipments and certain smartphone demand for support, yet actual purchasing momentum is not vigorous. Amid suppliers’ aggressive price-hiking stance – extending from wafers to finished products – module makers have also raised quotes to reflect increased costs. Buyers, with relatively low inventory, have no choice but to procure in advance, thereby driving up eMMC prices, with suppliers increasing targets for size, capacities, and applications. Concurrently, due to production costs extending to mainstream processes for eMMC, availability is dwindling, and clients may not fully receive their requested volumes. Therefore, eMMC contract prices in 4Q23 are expected to grow by approximately 10~15%.

UFS

The stage is set for a procurement boost in 4Q23, thanks to a trifecta of new releases, seasonal stocking, and some brands playing market share defense. Smartphone OEMs, wary of a changing tide, are scrambling to bump up component reserves to safe levels. UFS 4.0 has experienced the most significant price increase due to its limited supply as well as the product’s reliance on advanced manufacturing processes. While other mature UFS products have ample stock and numerous suppliers, OEMs are unwilling to continue selling at low prices for a loss. Instead, they have chosen to adjust and increase prices. It’s estimated that UFS contract prices will see a quarterly increase of 10~15% in 4Q23.

NAND flash wafer

After Samsung reduced its production by a staggering 50%, other suppliers have followed suit, adopting a conservative approach to wafer investment. This reduction in production – ongoing for over 6 months for specific processes and capacities – has led to a pronounced, structural tightness in supply across the market. This development positions suppliers favorably, granting them significant leverage over pricing. Observations for 4Q23 indicate a dearth of affordable supplies available for purchase, yet buyers are persisting in maintaining substantial inventory levels, continuing their procurement efforts unabated. In light of these conditions, suppliers are presently vying to elevate prices swiftly beyond cash costs. Projections for 4Q23 suggest an uptick in NAND flash wafer contract prices of approximately 13~18%.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter