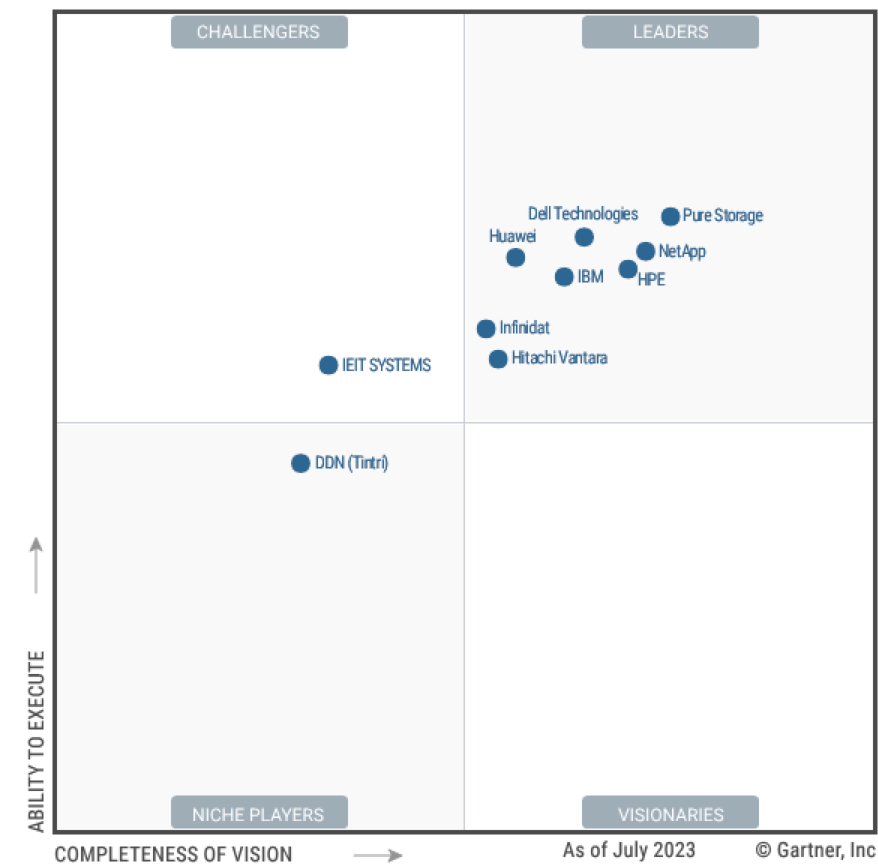

Magic Quadrant for Primary Storage

Leaders Dell, Pure Storage, Huawei, NetApp, IBM, HPE, Infinidat and Hitachi Vantara deeply analyzed

This is a Press Release edited by StorageNewsletter.com on October 6, 2023 at 2:02 pmPublished on September 18, 2023, this market report was written by Jeff Vogel, Joseph Unsworth and Chandra Mukhyala, analysts at Gartner, Inc.

Gartner Magic Quadrant for Primary Storage

Primary storage users are embracing infrastructure consumption-based services for hybrid, multidomain, mission-critical applications, and to align costs to business demands. I&O leaders should use this research to automate operations, reduce complexity and churn, and transform IT operations.

Strategic Planning Assumptions

- By 2026, storage consumption-based platform SLA guarantees will replace over 50% of traditional on-premises IT capacity management, budgeting, assessment, sourcing and fulfillment activities, up from less than 10% in 2023.

- By 2027, less than 30% of the IT storage infrastructure budget will be spent on hardware management and support IT skills, down from 85% in 2023.

- By 2028, consumption-based STaaS will replace over 35% of enterprise storage capital expenditures (Capex), up from less than 10% in 2023.

Market definition/description

Gartner’s view of the primary storage market is focused on innovative storage technologies and hybrid platform initiatives, IT cloud operating models, and as-a-service deployment and fulfillment methods that will shape the future needs of end users. It is not focused on the market as it is today. As outlined in Leverage Storage as a Service Platform SLAs and Capabilities To Transform IT Outcomes, the primary storage market is entering a period of accelerated innovation. End users are shifting away from traditional Capex financing and budgeting to the adoption of a hybrid platform strategy that embraces the on-premises cloud operating model and new vendor storage asset financing and management methods. Vendors’ advancements in platform capabilities, data and cyberresilience, and new storage OS architectures provide on-premises I&O leaders with SLAs targeted at IT operating model outcomes. The most fundamental question facing I&O leaders is how to gain access to cloud-like benefits while preserving high levels of resiliency and control over central-services-based IT operations infrastructure.

Gartner defines the primary storage market as vendors that offer dedicated products or services that pool capacity across storage media devices to present logical unit numbers (LUNs) to business applications over block interface protocols like FC or iSCSI. At the same time, the vendors provide high availability and data protection. Primary storage products can be delivered as solid-state arrays (SSAs), SDS or hybrid storage arrays. SDS software abstracts storage resources from the dependency to the underlying vendor’s hardware appliance for improved flexibility, cost-effective and efficient scalability, and linear performance in scaling to dozens of storage-compute nodes across the hybrid platform. It is designed to operate on industry standard hardware, either on-premises, via hybrid cloud or on the public cloud. Hybrid storage arrays include both SSD and HDD configurations. SSA products are 100% solid-state-technology-based systems that cannot be combined or expanded with HDDs. SSAs and hybrid storage arrays must have both a dedicated product name and associated model number.

A primary storage product’s foremost purpose is to support response time and IO/s-sensitive structured data workloads. Additionally, primary storage functionality will integrate with and support the independent use of a centralized control plane for automated infrastructure management, data services and data movement, and for storage-as-a-service hybrid infrastructure platform offerings. Typical use cases include:

Mission- and business-critical database workloads

Application consolidation

- Support for virtualization and virtual desktop infrastructure environments

- Persistent storage and data protection for container environments

- Hybrid cloud IT operations that span on-premises, colocation, edge and public cloud infrastructure

Core Capabilities

The core capabilities of the primary storage market include:

- Host interface protocols that are block-based, such as FC; iSCSI; Serial Attached SCSI (SAS); file-based, such as NFS and Server Message Block; or a combination of block and file protocols.

- Data services to pool capacity across storage media devices (HDD or Flash) and present LUNs to business applications.

- Data services that conserve capacity utilization, deliver high levels of efficiencies and resilience, protect vs. data loss and ransomware, and enable recovery via local and remote replication.

- Block-based STaaS offering that is available as service-provider-managed in partnership with the end-user client as an IT-managed offering.

- AIOps software that includes operational monitoring for prescriptive health, customer support, and support for proactive capacity management, nondisruptive workload simulation, data placement and migration, storage asset utilization cost optimization, performance optimization, and both full- and cross-stack and fleetwide telemetry observability, alerting and reporting.

- An SDS product architecture that separates the vendor’s storage hardware from the storage operating software. The SDS product supports on-premises storage, and/or one or multiple public cloud platform(s) that is accessible via a marketplace. It integrates with cloud provider’s server, storage and networking hardware, and deploys the same storage operating system as found in its on-premises appliance solution. It is also integrated with vendor AIOps functionality.

- Nondisruptive migration of data from current array to future array with a 100% data availability guarantee.

- Cyber storage protection and resilience, including support for ransomware detection, data protection and recovery capabilities.

Optional Capabilities

Additional primary storage capabilities include:

- SSAs with NVMe-oF as a host interface to provide support for both FC and Ethernet connectivity.

- Advanced AIOps real-time event streaming capabilities in support of monitored SLA threshold conditions that require automated, system-level (for example: nonhuman intervention) actions to critical IT operational situations, such as storage asset management, cyber liability resilience, and productivity.

- A multi-infrastructure domain and a hybrid-platform-wide, central control plane with multitenant, multivendor AIOps for ITOps-as-a-service capabilities, in support of advanced IT operating model SLA outcomes.

- Multiprotocol, disaggregated storage-compute architecture that supports nondisruptive, asymmetrical elastic scaling of capacity and compute, independent of each other, by maintaining performance through the addition of storage nodes from a small number of compute and storage nodes to dozens.

- Hybrid infrastructure platform offerings that integrate, manage, and support centralized IT data services infrastructure solutions, including but not limited to backup as a service, disaster recovery as a service, ransomware recovery or protection as a service, and database as a service.

- Published carbon emissions, as measured by total kilograms of CO2 per terabyte per year, of a fully loaded system, as measured in at least 2 major geographies.

- Special-purpose SSD or captive NVMe SSD drive for enhanced performance, endurance, management and data services.

- An array form factor that can be scale-out and based on SSDs or HDDs, or a combination of them.

Vendor Strengths and Cautions

DDN (Tintri)

Tintri by DDN is a Niche Player in this Magic Quadrant. It is operated as a subsidiary of DDN. Its products include the VMstore T7000 Series all-NVMe drive platform and TCE1000 VMstore, the SDS version of VMstore. The TCE1000 VMstore runs on public cloud or on-premises. The company offers a partially populated drive expansion array that allows clients to acquire additional capacity after initial procurement in the same array for growth purposes. The firm is geographically diversified in the SMB to midsize enterprise segments. Over the past 12 months, it added SSO support, NFS 4.1, Direct Upgrade, Tintri Cloud Engine (TCE) and upgrades to its Tintri storage OS.

Strengths

- Application-level AIOps capabilities provide proactive workload classification and resource optimization that allows customers to substantially reduce storage administration costs.

- Offers a patented drive-by-drive expansion unit to minimize upfront Capex and support costs, allowing customers to pay as they grow their capacity with very fine granularity.

- Tintri Global Center provides a common provisioning and management capability that integrates its on-premises VMstore storage array with the TCE1000 SDS in Amazon Web Services, providing customers with a hybrid cloud modernization plan.

Cautions

- It lags the primary storage market leaders in supporting as-a-service consumption plans with SLA guarantees, due to its lack of a product and set of offerings for an on-premises hybrid platform for centralized IT operations.

- It lags market competitors in not offering or supporting ransomware detection capabilities, only recovery from integrated backup support.

- Its TCE1000 SDS cloud engine lags leading competitive offerings in its breadth of public cloud options that it supports.

Dell Technologies

It is a Leader in this Magic Quadrant. Its PowerMax product is positioned in the high-end primary storage market, and its PowerStore is in the midrange storage market. PowerFlex is a scale-out SDS offering that is also available in the AWS Marketplace as APEX Block Storage. Dell APEX Data Storage Services offers block, file and data protection STaaS. The vendor’s operations are geographically diversified. Its clientele ranges from small to very large global enterprises, with a presence in all vertical markets. During the last 12 months, all 3 products were updated with new hardware models for increased performance and capacity, along with software updates focused on security and storage management. PowerFlex added support for NAS), multisite replication and FIPS 140-2 certification.

Strengths

- It is one of the few vendors in this market that can offer a full stack of infrastructure solutions, along with a comprehensive set of product capabilities to address all primary storage market segments.

- APEX Data Storage Services provides flexibility in deployment locations, and offers either self-managed or Dell-managed operations with support for all major use cases.

- Firm’s cyber vault enables customers to do forensics, analysis and surgical recovery from a secured copy in an operational, air-gapped vault in case of a cyberattack.

Cautions

- The company has 4 different block storage products with different feature sets, drive types (all-flash or hybrid) and types of cloud support, making it complex for Dell prospects to select the right product.

- Its block storage presence in the public cloud is presently limited to AWS and is based on PowerFlex, which does not currently have as large of an installed base as PowerMax or PowerStore.

- The firm lags the leading vendors in supporting QLC flash, which can enable higher capacities of SSD with lower costs and to reduce energy and carbon emissions.

Hitachi Vantara

It is a Leader in this Magic Quadrant. Its storage portfolio consists of Hitachi Virtual Storage Platform (VSP) and Hitachi Virtual Storage Software Block, which include some industry-specific applications with a common NVMe-optimized storage OS. Hitachi EverFlex offers a managed pay-per-use STaaS consumption model solution. Company’s operations are geographically diversified, and its clients tend to be global enterprise, open systems and mainframe customers, and are in the large and midsize enterprise segments. Over the past 12 months, Hitachi launched Hitachi Cloud Connect for Equinix for fast access to the public cloud without moving data into the public cloud. In addition, it added many enhancements to Hitachi Ops Center and Al Ops software for simplicity in management.

Strengths

- VSP and VSS Block offerings can withstand multiple simultaneous hardware failures without disruption to data services, and offers a written 100% availability guarantee.

- VSP offerings are certified under the Carbon Footprint of Products (CFP) program and the VSP 5600 product has one of the lowest carbon footprint of only 4 kilograms of CO2 per terabyte per year.

- The vendor bundles Lumada software with its storage arrays to provide customers with a digital innovation platform that works with business data and IT field assets to collect, catalog, analyze, visualize and relay digital information.

Cautions

- AIOps lacks the ability to perform predictive workload simulations and placements.

- Support for public cloud hosted storage is currently limited to AWS Japan.

- It does not have support for NVMe-oF over TCP, which will limit certain use case deployment options for customers who have made strategic investments in NVMe technologies.

Hewlett Packard Enterprise

It is a Leader in this Magic Quadrant. It’s storage portfolio includes Alletra 9000 and Primera for mission-critical applications, as well as Alletra 6000, Alletra 5000 and Nimble Storage for business-critical and general-purpose applications. HPE’s operations are geographically diversified, and its clients tend to be in enterprise and small to midsize enterprise markets. In the past 12 months, the company enhanced GreenLake for Block Storage with SDS combined with a disaggregated architecture using Alletra MP for different storage protocols, including block and file storage, and the Alletra 5000 series for HPE Nimble Storage Hybrid Array clients.

Strengths

- GreenLake users have expressed high customer satisfaction, and the company is recognized among IT clients as a platform provider that leverages AIOps to deliver advancements in hybrid IT platform management that simplify onboarding, provisioning and storage asset life cycle management for STaaS.

- InfoSight is an integrated, application-centric, full-stack AIOps tool that provides proactive and predictive telemetry-based capabilities that underpin advanced IT SLA guarantees, including a standard written 100% data availability guarantee.

- HPE Financial Services (HPEFS) provides flexible investment solutions, financing and storage asset management programs to free up capital and to streamline the transition to an as-a-service platform.

Cautions

- GreenLake managed services will face operational challenges as it scales and as HPE supports a growing volume of large-scale IT platform demands.

- There is the potential for confusion among channel partners and customers with HPE pricing as the vendor shifts from selling products through traditional Capex transaction methods to GreenLake consumption-based, as-a-service offerings.

- Primera and Alletra 9000 series arrays do not support NVMe-oF over TCP, which will limit deployment options from customer investments in NVMe technologies over Ethernet.

Huawei

It is a Leader in this Magic Quadrant. Its product portfolio consists of the all-flash and hybrid OceanStor Dorado Series and SDS OceanStor Pacific Series. The firm mainly operates in China, Latin America, Europe, the Middle East and Africa, and its clients tend to be in the large enterprise and public clouds in China. Its products target a range of entry-level, midrange and high-end storage array use cases. In the past 12 months, the firm released a highly reliable, 4-data-center, active-active storage, support for NVMe-RDMA, a NAS ransomware detection solution, and ElasEver to satisfy STaaS requirements.

Strengths

- It has simplified and accelerated client onboarding through use of a discovery and AIOps tool that digitally discovers critical infrastructure elements for improved IT control.

It provides the capability to schedule, dynamically adjust and maximize replication bandwidth in alignment with host workload activities, therein maximizing infrastructure benefits.

- Ransomware detection solution includes a storage-network approach that integrates a rule-based AI model with frequent updates to the ML analysis, reducing overall threats within the storage environment.

Cautions

- It lags other industry leaders in providing storage asset financing and management capabilities that simplify and streamline STaaS onboarding and time to value.

- It lacks a competitive SDS offering that enables hybrid cloud storage use cases with the following cloud infrastructure platforms: AWS, Microsoft Azure and Google Cloud Platform (GCP).

- OceanStor Dorado array series products do not support NVMe-oF over TCP, which will limit specific deployment options for customers who have made strategic investments in NVMe technologies over Ethernet.

IBM

It is a Leader in this Magic Quadrant. Its Storage Virtualize is the common storage controller software on FlashSystem solid-state array (SSA) and hybrid appliances. Storage Virtualize for Public Cloud is available on AWS, IBM Cloud and Microsoft Azure. The DS8900F platform is focused on the company’s mainframe infrastructure market and all offerings are available as STaaS. Big Blue offers a global reach and positions its products primarily in midsize to very large enterprises. During the last 12 months, it introduced improved asynchronous replication, snapshot management capabilities, NVMe-over-TCP support and block storage as a service.

Strengths

- Unique FlashCore Module technology enables leading price/performance and security advantages for the FlashSystem SSA portfolio.

- Storage Virtualize software data management flexibility extends across on-premises, in public cloud or in colocation to enable a standardized customer experience and services across platforms.

- Storage Sentinel’s advanced scanning abilities for detection and prevention of ransomware provides a more cyber-storage-resilient capability beyond standard protection and recovery methods.

Cautions

- Storage offerings, core technology capabilities and STaaS solution are relatively unknown outside of its customer base, making it difficult to assess the competitive value of its offerings for non-IBM customers.

- Without Storage Expert Care coverage, older products may see steep price increases or fee adjustments for extended support and maintenance.

- Storage Virtualize for Public Cloud is limited in the number of storage nodes in each of the public cloud offerings, lagging some of the industry leaders in scale-out, linear performance.

IEIT Systems

It is a Challenger in this Magic Quadrant. It has a broad portfolio of primary storage products, including the NVMe all-flash array HF Series and a new SDS AS13000 ICFS product to address entry-level, midrange and high-end market requirements. Firm’s operations are largely concentrated in China. Clients are mainly in the midmarket and large enterprise market segment. In the past 12 months, the company has introduced support for an anti-ransomware detection and recovery solution, and for its AS13000 ICFS SDS product, synchronous and asynchronous remote replication, and volume encryption.

Strengths

- It is leveraging its captive NVMe SSD drive cost advantages by proactively offering to replace its clients with a mixed hard-disk and flash-installed base with the NVMe SSD drive.

- It combines the AS13000 ICFS SDS product with the strength of its server business to create a price/performance cost advantage over competitive SDS offerings.

- Its clients cite cost-effective pricing and highly resilient storage as reasons to select its products over competing options.

Cautions

- View of the market and its roadmap are not aligned to customer needs outside of the primary China region in which they market and sell their products.

- It lacks a competitive SDS offering for hybrid cloud storage solution for use in the three major public clouds (AWS, Azure and Google), making it tougher for end users to evaluate and assess their hybrid cloud platform strategy.

- Its workload placement AIOps capabilities lag industry leaders for effective optimization and resource allocation across infrastructure, making it difficult for customers to achieve optimal resource utilization and cost efficiencies.

Infinidat

It is a Leader in this Magic Quadrant. The InfiniBox and InfiniBox SSA II are based on its common InfuzeOS, also now available as an SDS product. It is a private company focused on North America, EMEA and Japan that focuses on large enterprises and service providers. In the last 12 months, recent updates are: InfuzeOS Cloud edition for AWS, enhancements for its SSA portfolio, InfiniSafe technology offers cyberdetection, providing dataset scanning and extending its file capabilities. Neural Cache architecture optimizes HDD with SSD technology, providing strong performance in a hybrid system. The products perform well in large-scale virtualization environments, databases and especially for application consolidation.

Strengths

- Customers express a high level of satisfaction with its ease of use, technical support and professional services that are supported by a suite of service-level guarantees.

- Excels at application consolidation, with petabyte-scale offerings in both hybrid and all-flash configurations, achieving favorable dollar per I/O and dollar-per-watt returns that underpin compelling TCO benefits.

- Offers a variety of purchasing models, including Capex-only, elastic pricing (a combination of operating expenditure [Opex] and Capex pricing) and FLX, a consumption-based STaaS offering.

Cautions

- Has limited geographic support for emerging markets, making it difficult for some multinational companies to evaluate services and support capabilities for long-term investments.

- Portfolio lacks a low-capacity (sub-250TB) offering and de-dupe capabilities, limiting its appeal to some smaller customers and select workloads that benefit from de-dupe.

- New SDS InfuzeOS Cloud Edition is based on a single-node architecture, limiting its cloud-native scalability and resiliency attributes, and it is only currently available on AWS.

NetApp

It is a Leader in this Magic Quadrant. It addresses a range of primary storage workloads across its storage arrays: AFF A-Series, AFF C-Series, ASA, FAS, E-Series, EF-Series and its SDS offering, Cloud Volumes Ontap. It supports a global customer base with on-premises or cloud-native storage. During the last 12 months, it introduced a ransomware recovery guarantee, as well as the AFF C-series, which leverages cost-effective QLC flash, packing more capacity per flash drive and thereby lowering energy and carbon emissions. It also introduced its dedicated block-only ASA A-series, with multiple models. Ontap One is a new offering that bundles all data services into a single license and is available across firm’s AFF, ASA and FAS storage models.

Strengths

- Storage OS is designed to run on-premises, and in AWS, Azure and GCP, with the ability to tier and replicate between locations and manage them from a common SaaS-based control plane.

- Has mature and rich enterprise file services capabilities, making it a reliable unified storage offering.

- Its BlueXP is a centralized, AIOps-powered, SaaS-based management portal for its products across on-premises and cloud locations, with built-in capabilities for cloud migration, data classification, governance, protection and storage optimization.

Cautions

- Some customers have expressed concerns about ease of use and the quality of initial technical support.

- Compared to its peer group, has had a limited rollout of financing and storage capitalization for STaaS channel initiatives, limiting on-premises capex to consumption customer deployment options.

- Portfolio can be complex and requires careful understanding of the trade-offs between the different products to select the right product for application and business requirements.

Pure Storage

It is a Leader in this Magic Quadrant. Its portfolio consists of FlashArray//XL, FlashArray//X, FlashArray//C and FlashArray//E, spanning high-to-low performance and capacity workloads. Its SDS offering, Cloud Block Store, is available on AWS and Microsoft Azure. The company sells across small to very large customers and plays mostly in North America, Europe and select countries in APAC. In the last 12 months, the vendor introduced FlashArray//E, which challenges hybrid array price points over 1PB. Additionally, it rolled out performance improvements with its //X and //C products, enhanced file capabilities and improvements to its Pure1 AIOps.

Strengths

- Vertically integrated direct flash modules are tightly integrated with the Purity OS, enabling compelling economics at PB system capacities without compromising performance and reliability.

- The company’s Evergreen portfolio provides flexible consumption model options ranging from all-capex to all-opex, and a hybrid model in the middle, where hardware is capex and software is opex.

- Customer experience is rated highly, as its ease of use and high service levels help reduce administration complexity and save costs.

Cautions

- Aacquisition pricing on its high-end products and overall support fees are generally more expensive than competitive offerings, as a percentage of the initial array costs over a 3-year period.

- Does not offer any cost-effective alternatives to hybrid storage below 250TB, where price is paramount and performance secondary.

Lacks international presence in emerging countries, which could be problematic for customers demanding specific support and service needs.

Vendors added

No vendors were added to this Magic Quadrant.

Vendors dropped

- Fujitsu was unable to meet inclusion criteria, due to its dependency on a 3rd-party storage controller OS.

- Lenovo was unable to meet inclusion criteria, due to its dependency on a 3rd-party storage controller OS.

- Zadara was unable to meet the minimum revenue inclusion criteria.

Market overview

Total external-controller-based (ECB) primary storage revenue grew 5.3% from 2021 to 2022 to $16.8 billion, as a result of solid-state array (SSA) revenue of $1.1 billion in growth, to $10.6 billion total for the period. Primary storage revenue shifted from HDD/hybrid to SSA, driving up SSA’s share in the primary storage market to 63% in 2022. Total ECB primary storage revenue was offset by a decline in hybrid array revenue by $211 million, as the market continued to accelerate to SSA flash. The overall ECB storage global revenue, of which primary storage is a major segment, increased 6.9% to reach $22.7 billion in 2022, fueled by continued storage infrastructure modernization.

External storage systems revenue WW was $5.0 billion in 1Q23, an increase of 0.5% compared to 1Q22. Revenue for SSAs and backup and recovery appliances grew by 3.6% and 9.4% Y/Y, respectively, while HDD/hybrid arrays saw a revenue decline of 1.4%. In the last calendar quarter ending 31 March 2023, the primary storage ECB market was $3.64 billion, down 1.4% from $3.7 billion in 1Q22.

Primary storage vendors continued to make incremental investments to their product portfolios to include support for capabilities such as QLC, cyber resiliency and NVMe-oF TCP technologies. Some vendors have added data services to their STaaS solutions, such as backup, DR and ransomware recovery. Also, every primary storage vendor now offers an STaaS for block service, with total STaaS annual recurring revenue exceeding $1.0 billion as of the end of 2022.

Primary storage vendors also continued to invest in SDS capabilities that provide tighter integration with public cloud providers, extending their on-premises solution to enable hybrid platform solutions. Vendors also have invested heavily in AIOps capabilities to automate telemetry-metric-based SLA offerings in support of application requirements. They have also improved storage asset management costs and optimized utilization with elastic scaling to real-time workload demands. In addition, they have made a conscious effort to reduce support and maintenance costs, included in their as-a-service consumption licensing and pricing.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter