History 2001: AsiaPac Disk Storage Systems Market Hesitates but Grows

Increased by 4.7% in the first 6 months of 2001 compared with the same period in 2000

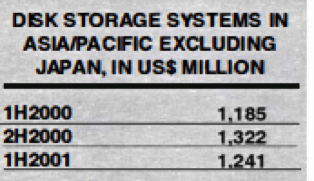

By Jean Jacques Maleval | April 20, 2023 at 2:01 pmIDC research has shown that the disk storage systems market revenue in AsiaPac excluding Japan increased by 4.7% in the first 6 months of 2001 compared with the same period in 2000.

This is attributed to the strong demand for disk storage capacity in most country markets although spending constraints are appearing, impacting overall expenditure.

Total capacity added in the 6 months was 14,325 TB, up 93.6% on the corresponding period in 2000. The market was valued at $1,241 million for the first six months 2001.

However revenue growth is being impacted by the continuing decrease in the price of storage capacity per gigabyte. The majority of growth in storage in AsiaPac in 2001 is still being driven by applications that need continuous availability, content replication and distribution, and information sharing. Data for these applications is primarily being located in external storage subsystems. The key market drivers are applications that capture, store, and access vast amounts of data resulting in a dramatic increase in the demand for additional storage resources.

Although disk storage systems internal to the server have experienced growth at a higher rate than the increase in the number of servers, it is external disk storage systems that are in experiencing the largest increase in demand. External storage systems are key building blocks for SANs and for NAS and are also being installed for rackmount installations.

The storage market in AsiaPac has been impacted to varying degrees by the recent economic downturn, although this has varied by country. Broadly, there has been increasing interest in low-cost, shorter term storage solutions. Many users still have the ongoing need for significant and regular increases in storage capacity due to the sheer growth of data. The limitation on expenditure budgets, however, has resulted in a short term response to buy more low cost DAS or NAS storage at the expense of deferred integration and management costs. This has provided a market opportunity for vendors offering low-cost storage systems. External storage systems are able to expand incrementally as the organization’s demand for storage rises.

The report indicates that users in many organizations are beginning to see the storage resource as a competitive differentiator rather than simply as a growing, necessary cost. This change in mind-set is becoming important for vendors and channel partners. It will provide a key reason for user organizations to adopt network storage solutions that offer significant benefits in terms of data access, availability and reliability to those users that can make a successful transition.

Market drivers

The majority of growth in storage in AsiaPac in 2001 is still being driven by applications that need continuous availability, content replication and distribution, and information sharing. Data for these applications is primarily located in external storage subsystems. The key market drivers are applications that capture, store and access vast amounts of data.

These include:

- eBusiness and increased Web activity,

- email and collaborative computing in which data replication is a major source of increased storage demand,

- enterprise resource management,

- data warehousing and decision support systems,

- new applications which store video, voice and sound, analog and real time data, and graphics or other images,

- user organizations expanding their reach out towards their customers or backwards down the supply chain.

Each of these results in a dramatic increase in storage requirements and typically leads to a re-assessment of the organization’s storage architecture due to the need to proactively manage the growing storage resource.

Key vendors

The largest storage system suppliers in AsiaPac in the first half of 2001 included the major systems suppliers, Compaq, IBM, Sun, and HP. These 4 vendors accounted for almost two 3rd of storage systems revenue.

Server-independent storage vendor, EMC, has secured a strong market position and accounted for 15.6% of the total market revenue.

The top 5 vendors accounted for more than 80% of the storage systems revenue.

NetApp, HDS, and Dell have also secured prominent positions in some country markets. Storage-only, server-independent storage vendors such as EMC, NetApp, and HDS are promoting their ability to operate in most server environments unconstrained by the existing server and application infrastructure.

This approach contrasts with the major server vendors who typically have a high share of their own server environments but a much lower share in other accounts.

The major vendors are seeking to build on their existing installed base and are working closely with channel partners to build market penetration, particularly aiming to secure a strong early position in the rapidly growing network storage market.

This article is an abstract of news published on issue 166 on November 2001 from the former paper version of Computer Data Storage Newsletter.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter