WW NAND Flash Revenue Fell by 24% Q/Q for 3Q23 at $13.7 Billion

As suppliers made large price concessions with ASP down 18%.

This is a Press Release edited by StorageNewsletter.com on November 29, 2022 at 2:01 pmThis market report, published on November 23, 2022, was written by Bryan Ao and Sean Lin, analysts at market intelligence firm TrendForce Corp.

Global NAND Flash Revenue Fell by 24.3% QoQ for 3Q23

As Suppliers Made Large Price Concessions That in Turn Impacted Their Results

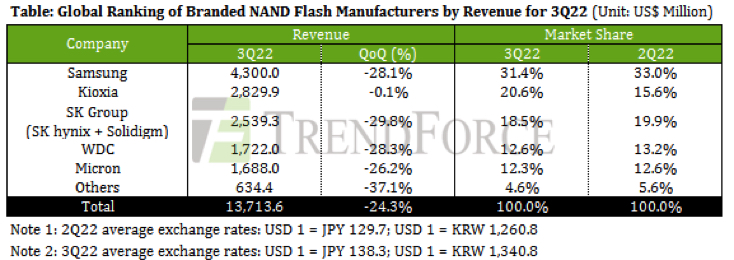

The whole NAND flash market was severely weakened by plummeting demand in 3Q22.

Because shipments of end products including consumer electronics and servers had been below expectations, the overall NAND ASP fell by 18.3% Q/Q. Furthermore, the general economic outlook remained pessimistic, so enterprises across many sectors started to scale back their capital expenditure plans and halted the momentum of their procurement activities. Due to this development, the problem of excess inventory eventually spread to NAND flash suppliers. The pressure on suppliers to make sales was ratcheted up dramatically. NAND flash bit shipments fell by 6.7% Q/Q for 3Q22, and the overall NAND flash ASP also kept sliding. On account of the unfavorable market situation, the NAND flash industry recorded a total revenue of $13.71 billion for 3Q22. The QoQ revenue decline reached as much as 24.3%.

The ranking of NAND flash suppliers by revenue saw 2 notable changes for 3Q22.

First, SK Group moved down to 3rd place as it suffered the largest revenue drop among suppliers. Its revenue slipped by 29.8% Q/Q to $2.54 billion mainly due to the significant deterioration of the demand for PCs and smartphones. Its subsidiary Solidigm was also affected by the slowdown in server procurements. Previously, servers had a fairly stable demand situation compared with other kinds of end products. However, server demand eventually buckled in 3Q22 as result of enterprises cutting capital expenditure and undergoing a period of inventory correction. Compared with 2Q22, SK Group (that encompasses SK hynix and Solidigm) posted a drop of 11.1% in bit shipments and an even steeper decline of more than 20% in ASP.

The other notable change in the 3Q22 ranking was Kioxia. The supplier returned to 2nd place in terms of revenue and market share because it was able to make a gradual recovery from the material contamination incident that had happened earlier this year. Even though Kioxia did suffer a significant decline in its ASP due to the slumping demand for consumer electronics, its bit shipments were bolstered by the seasonal stock-up activities of its clients in the smartphone industry and rose by 23.5% Q/Q. Taken altogether, Kioxia’s revenue dipped by just 0.1% Q/Q to $2.83 billion.

Owing to Downturn in Both Quantity and Price, Micron Posted Largest Drop in NAND Flash Bit Shipments with Q/Q Decline Reaching 21%

Other NAND flash suppliers including Samsung, Western Digital and Micron all posted a considerable Q/Q decline in revenue for 3Q22 because of a drop in both price and shipment quantity. Again, weakening demand for end products was one of the major reasons behind these suppliers’ poor performances.

Regarding Samsung, the supplier saw a drop in its enterprise SSD shipments during 3Q22 as server demand slowed down. This was a sharp negative turn compared with the situation in 2Q22, when orders related to data centers were propping up enterprise SSD procurements. Samsung’s revenue fell by 28.1% Q/Q to $4.3 billion for 3Q22.

Western Digital‘s NAND flash business were under enormous pressure in 3Q22 as it recorded a Q/Q decline in bit shipments and a sharp drop in its ASP. All in all, its revenue fell by 28.3% Q/Q to $1.72 billion.

Turning to Micron, an analysis of its memory revenue performance, which encompasses both DRAM and NAND flash, has revealed that the only the application segment that did well in 3Q22 was automotive memory solutions. It actually posted a new high for its revenue from automotive memory solutions in that quarter. Conversely, its revenue figures related to other memory-related applications, including NAND flash solutions for data centers, industrial IoT, etc., all exhibited a Q/Q drop. And because of the poor results for the rest of application segments, its NAND flash revenue as a whole registered a steep Q/Q decline of 26.2% to $1.69 billion.

NAND Revenue Will Show Q/Q Drop Again for 4Q22 as Inventory Pressure Continues to Mount and Production Cuts Bring No Immediate Relief

Moving into 4Q22, TrendForce believes that with the notable exception of Samsung, most suppliers will be more cautious in planning output following their respective earnings calls for the third quarter. To restore balance to supply-demand dynamics as quickly as possible, suppliers will be taking measures such as cutting wafer input and decelerating the pace of technology migration.

However, the usual demand surge in connection with the year-end holiday sales has failed to materialize this year, and NAND flash buyers’ passiveness is causing inventory to further accumulate on the supply side.

As for production cuts, their effect on the market will not be apparent for at least a quarter. Hence, prices of NAND flash products will still be under significant downward pressure in 4Q22, and TrendForce has widened the projected Q/Q decline in contract prices to 20~25% in its latest forecast.

With high inventory and falling prices serving as constraining factors, the NAND flash industry is also forecasted to post a Q/Q decline of almost 20% in its total revenue for 4Q22.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter