NAND Flash Revenue at $74 Billion in 2022 Corresponding to 7.4% Y/Y Increase

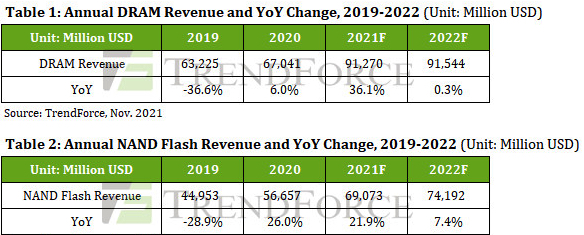

2022 DRAM sales reaching $91.5 billion, with prices likely to rally in 2H22

This is a Press Release edited by StorageNewsletter.com on November 11, 2021 at 2:02 pmDespite the forecasted 18.6% Y/Y growth in total DRAM bit supply next year, the global DRAM market is still expected to shift from a shortage situation to an oversupply, according to TrendForce, Inc.

This shift can primarily be attributed to the fact that, not only are most buyers now carrying a relatively high level of DRAM inventory, but DRAM bit demand is also expected to increase by only 17.1% Y/Y in 2022. On the price front, the oversupply situation will result in a drop in DRAM ASP in 2022 but not a major decline in annual DRAM revenue, thanks to the oligopolistic nature of the DRAM industry. Annual DRAM revenue for 2022 is expected to reach $91.54 billion, which represents a slight Y/Y increase of 0.3%.

Based on an analysis of DRAM sufficiency ratio (which refers to the surplus of supply in comparison with demand) for each quarter in 2022, it is forecasted a 15% Y/Y decrease in DRAM ASP for 2022, with prices undergoing the more noticeable declines during the first half of the year. Heading into 2H22, however, owing to the rise in DDR5 penetration rate, as well as the arrival of peak seasonal demand, the decline in DRAM ASP will likely narrow. TrendForce does not rule out the possibility that DRAM ASP may even hold flat or undergo an increase in 2H22.

Annual NAND flash revenue expected to experience yet another increase next year by 7.4% Y/Y while numerous suppliers compete in higher-layer NAND flash market segment

Turning to the NAND flash market, the forecast iss a 31.8% increase in total bit supply for 2022 and a 30.8% increase in total bit demand. Hence, NAND flash ASP will likely experience a downtrend next year as a result of the oversupply situation. In addition, due to the perfect competition in the NAND flash market, the decline in NAND flash ASP next year will be more noticeable than the decline in DRAM ASP. However, NAND flash suppliers continues to make progress in the stacking of NAND flash layers, so the growth in NAND flash bit supply next year will therefore remain above 30%. TrendForce thus expects NAND flash revenue to have more room for growth and reach $74.19 billion in 2022, a 7.4% Y/Y increase.

The forecast is based on an analysis of NAND flash sufficiency ratios for each quarter in 2022 similarly points to an 18.0% Y/Y decline in NAND flash ASP next year. Much like DRAM, NAND flash prices will undergo the more noticeable declines during 1H22. Arrival of peak seasonal demand in 2H22 will potentially result in a narrowing of price drops and a potential for quarterly prices to hold flat.

On the whole, the revenue performance of the DRAM industry and that of the NAND flash industry over the years show that the annual total DRAM revenue is growing at more stable pace. Again, this has to do with the oligopolistic structure of the DRAM market. Since the DRAM market has a different competitive landscape, the fluctuations in the overall DRAM ASP have been relatively modest over the long run. However, the development of the DRAM manufacturing technology is approaching a physical bottleneck as process nodes shrink below the 20nm level. This means that the bit growth derived from the deployment of a more advanced process is becoming more and more limited over the years.

On the other hand, not only are NAND flash suppliers relatively more unstable in their capacity expansion plans compared to the DRAM industry, but further improvements in NAND flash layer-stacking technology also remains feasible. Hence, the fluctuations in the overall NAND flash ASP have been relatively more volatile over the long run. On account of these factors, the DRAM industry generally has smaller Y/Y revenue growth rates compared with the NAND flash industry, although the DRAM industry continues to surpass the NAND flash industry in terms of profitability.

Profitability of suppliers may be constrained if total revenue fails to keep pace with continuously rising Capex

Regarding the Capex of DRAM suppliers, there has been a gradual increase in these suppliers’ Capex to sales ratio in recent years, for 2 reasons.

First, the development of the DRAM manufacturing technology is approaching a physical bottleneck. Die improvements have become more and more limited after process nodes have shrunk below the 20nm level. Micron’s 1alpha nm process can offer an almost 30% increase in bits per wafer, but the 1Xnm-to-1Ynm migrations and the subsequent 1Ynm-to-1Znm migrations that the major suppliers have undertaken in the recent period have yielded increases of no more than 15% in bits per wafer. Looking at future technological developments, Samsung and SK hynix have already integrated EUV lithography into their most advanced process technologies. However, orders for EUV lithography tools have a much longer lead time, and the costs of these tools are also high. Hence, the three dominant suppliers have allocated a large chunk of capital expenditure in advance to place orders for EUV lithography tools ahead of time.

Secondly, the oligopolistic structure of the DRAM market has also helped establish a regime where there is a very low chance of a supplier’s ASP dipping under its fully-loaded cost despite the recurrence of the cyclical price downturn. Moreover, DRAM suppliers have accumulated a substantial amount of profit from their products. In view of the difficulties in die shrinking, suppliers ranging from the three dominant suppliers to others with less market share (such as Nanya Tech and Winbond) have developed tangible plans for capacity expansions. These plans have, in turn, become the other main driver behind the ongoing increase in the Capex to sales ratio.

The Capex to sales ratio of NAND flash suppliers have likewise risen substantially following the transition to 3D NAND technology in 2017. Notably, the average Capex to sales ratio fell within the 25-30% range prior to 2017, but it has since climbed to nearly 40% as of now. This growth can primarily be attributed to the fact that, as the number of 3D NAND layers increases, there is a corresponding increase in the lead times of NAND flash products and in the degree of precision as well as difficulty involved in the etching process. While the mainstream layer count of NAND flash products approaches 1YY layers, suppliers are currently planning to move forward with the development of products with 2XX layers, which place an ever-increasing demand on etch depth. The Capex of NAND flash suppliers will continue to grow alongside increases in layer count and revenue.

TrendForce indicates that NAND flash layer-stacking technology will continue to progress, meaning suppliers will continue to pursue the stacking of additional layers as a way to lower their manufacturing cost per gigabyte. As such, the NAND flash industry’s Capex will have additional potential for growth going forward, with a Capex to sales ratio of close to 40% or above. It should be noted, however, that if total NAND flash revenue fails to keep pace with the growth in Capex in the next few years, NAND flash suppliers’ Capex to sales ratio may potentially undergo an excessive increase, thereby constraining the profitability of suppliers.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter