History (1996): 1997 RAID WW Sales to Top $12 Billion in 1996, Rising to $18.6 Billion in 1999

As marginal array producers start to drop out.

By Jean Jacques Maleval | August 16, 2021 at 2:01 pmThe disk drive array market continues to grow rapidly, led by strong sales of disk drive arrays, popularly known as RAID subsystems, for expanding applications with network file servers and mainframe computer systems.

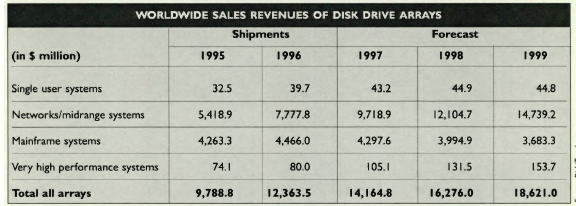

1996 WW sales are expected to reach $12.3 billion, rising to $18.6 billion in 1999, according to Disk/Trend’s market study on disk drive arrays ($1,475).

As disk drive arrays have become a major part of the computer industry, a shakeout of manufacturers with marginal market shares has started.

The report on disk drive arrays lists 158 companies which offer disk drive arrays under their own name, down from 179 a year ago. Companies headquartered in USA produced over 92% of 1995’s revenue total, with IBM, EMC, Digital Equipment and Compaq Computer the leaders in WW sales.

+130% for mainframe disk arrays

Sales of disk drive arrays used with mainframe computers grew faster during the last few years than any other type of array, up more than 130% in 1995, spearheaded by successful products from EMC, IBM and Hitachi Data Systems. But mainframe array sales revenues are expected to peak in 1996 at $4.4 billion, with a gradual decline to follow. Annual increases in the amount of disk storage capacity used with mainframes are expected to continue, but prices for disk drives will decline even faster, causing WW sales revenues for mainframe array subsystems to drop an average of 6.2% during each of the next 3 years.

Largest market: network servers and mid-range systems

Network server and mid range system applications are clearly the largest market for disk drive arrays, with 55.4% of 1995 sales revenues and 91.8% of the total unit shipments. More than 140 disk drive array producers are active in the networks/mid-range systems field, including more than IO systems manufacturers selling internally developed arrays with their own computer systems on a captive basis. Worldwide sales revenues for networks/ mid-range system arrays are projected to climb from 1995’s $5.4 billion to $14.7 billion in 1999.

Towards single chip controllers array controller boards, used by OEMs, integrators and computer do-it-your-selfers to assemble complete array subsystems, have experienced a high growth rate in recent years, and unit shipments jumped another 54.3% in 1995.

However, the future of board-level array controllers has been threatened by the introduction of single chip and chip set array controllers which can be mounted on system motherboards, eliminating the need for separate array controller boards in many array subsystems for PC networks.

The Disk/Trend forecasts indicate a decline in array controller boards after 1998.

IBM, number one

Boosted by large sales increa es for new mainframe arrays, plus established mid-range array product lines, IBM maintained its leadership in total disk drive array sales revenues, holding 33.7% of the 1995 WW total, with $3.3 billion in sales. EMC continued in second position with 16.1% of overall array revenues, generated by array subsystems for the IBM mainframe, mid-range and OEM markets. Digital Equipment held 12.6%, mostly from strong captive sales of its highly modular array subsystems, supplemented by growing OEM sales.

The report also contains basic product specs on 694 disk drive array models and profiles on 182 existing and former manufacturers of disk drive arrays.

This article is an abstract of news published on the former paper version of Computer Data Storage Newsletter on issue 107, published on December 1996.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter