History (1995): 1995 Sales for RAIDs Set at $7.7 Billion, Revenue Over $13 Billion Forecasted for 1998

IBM leader with 23% followed by EMC at 22%

By Jean Jacques Maleval | March 30, 2021 at 2:31 pmDisk drive arrays have become a major part of the storage industry.

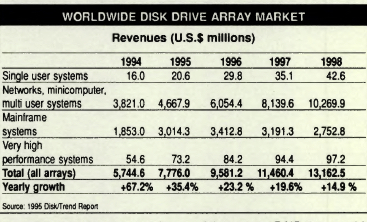

According to a Disk/Trend (Mountain View, CA) market study on disk drive arrays, known by many under the RAID acronym due to generous publicity since the beginning of the 1990’s, WW sales revenues will exceed $7.7 billion in 1995, as the result of shipment of more than 565,000 arrays.

More than $13.1 billion is forecasted for the WW RAID 1998 total, but the industry’s structure and products are evolving as the sales increase.

Disk drive array sales for network, minicomputer and multi-user markets are expected to remain the largest product group, with more than $10 billion in 1998 revenues.

However, disk drive array sales revenues for mainframe computers are expected to peak in 1996 – not because less storage capacity will be shipped, but due to continuous price reductions for the large quantity of disk drives shipped with mainframe disk arrays.

The network server and midrange system market generated 66.6% of all RAID sales revenues in 1994 and consumed 93.1% of all array shipments. This market was dominated by US systems manufacturers, such as Compaq, IBM, Hewlett-Packard, Digital Equipment and Sun Microsystems, selling internally developed “captive” arrays with their own computer systems.

EMC has been developing the market for mainframe disk drive arrays for several years, and was joined during the past year by Storage Technology, Hitachi and IBM, with the result that mainframe array sales revenues are expected to jump from 1993’s $867 million to over $3 billion in 1995. But next year is forecasted to be the peak revenue year for mainframe arrays, at $3.4 billion, dropping to $2.7 billion in 1998.

Despite a weak mainframe computer market, the amount of disk storage capacity is projected to increase, but the prices for disk drives will decline even faster. During the last few years, shipments of array controller boards, used by OEMs, integrators and computer do-it-yourselfers assemble complete array subsystems, have enjoyed a higher growth rate than any other array product group, up 103.3% in 1994, with another 65.2% jump forecasted for 1995.

This pattern is expected to change after 1996, with the introduction of single chip array controllers which can be mounted on system motherboards, and unit shipments of board-level arrays are expected to be in decline by 1998.

179 companies which offer disk drive arrays under their own name are identified in the Disk/Trend Report, an increase of 25 companies in the last year. 147 of these firms are headquartered in USA, and these US-based companies produced over 94% of 1994’s revenue total. 707 disk drive arrays are described in detail in the study.

RAID-5 has become the most popular array configuration, and 70% of the individual arrays listed in the report have RAID-5 capability, optimized for fault tolerance, with the ability to rebuild lost data if one drive fails. 23% are RAID-0 or RAID-1, or combinations, designed for mirroring disks or striping data across all drives in an array. Most of the rest are RAID-3, or combinations thereof, with lower RAID levels, optimized for high data transfer rates.

IBM continued as the leader in RAID revenue, capturing 23.3% of the 1994 WW total, with $1.3 billion in sales of complete subsystems for captive use with networks and midrange systems, plus mainframe array sales starting the fourth quarter of the year.

EMC was close behind with 22.3% of overall array revenues, from subsystems with mirrored disk capability for the IBM mainframe, IBM AS/400 and OEM markets.

Digital Equipment held 12.1%, mostly from strong captive sales of its highly modular array subsystems.

This article is an abstract of news published on the former paper version of Computer Data Storage Newsletter on issue 90, published on July 1995.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter