NAND Flash Revenue for 3Q20 Up by Only 0.3% Q/Q

Owing to weak server sales

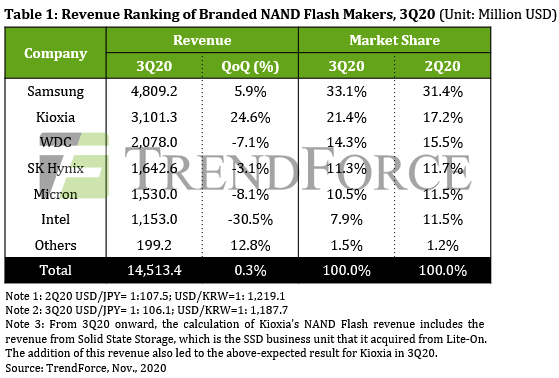

This is a Press Release edited by StorageNewsletter.com on November 30, 2020 at 2:15 pmTotal NAND flash revenue reached $14.5 billion in 3Q20, a 0.3% increase Q/Q, while total NAND flash bit shipment rose by 9% Q/Q, but the ASP fell by 9% Q/Q, according to TrendForce, Inc.

The market situation in 3Q20 can be attributed to the rising demand from the consumer electronics end as well as the recovering smartphone demand before the year-end peak sales season. Notably, in the PC market, the rise of distance education contributed to the growing number and scale of Chromebook tenders, but the increase in the demand for Chromebook devices has not led to a significant increase in NAND flash consumption because storage capacity is rather limited for this kind of notebook computer.

Moreover, clients in the server and data center segments had aggressively stocked up on components and server barebones during 2Q20 due to worries about the impact of the pandemic on the supply chain. Hence, their inventories reached a fairly high level by 3Q20. Clients are now under pressure to control and reduce their inventories during this second half of the year. With them scaling back procurement, the overall NAND flash demand has also weakened, leading to a downward turn in the contract prices of most NAND flash products.

On the other hand, the latest escalation in the US-China trade dispute saw the US government expanding its export control rules vs. Huawei in mid-3Q20. Subsequently, Huawei had to pull component shipments forward and stock up as much as possible before the rules came into effect. The wave of procurement triggered by this event affected not only MCP and UFS solutions for smartphones but also low-density MLC eMMC solutions for consumer products and NAND wafers for components. Bit shipments for 3Q20 on the whole grew on account of this event.

Looking ahead to 4Q20, customers in the server segment will continue with their inventory reduction efforts. Hence, the overall demand will still be rather sluggish. Furthermore, the wave of procurement initiated by Huawei has subsided since the stricter export control regime came into force in mid-September. Other Chinese smartphone brands are now aggressively building their component inventories in preparation to capture Huawei’s market share. However, their demand together with the demand related to the iPhone 12 series is not enough to reverse the oversupply situation that will be affecting the entire NAND flash market through 4Q20. Also, Samsung and YMTC still intend to continue raising production output, thereby worsening the glut in the NAND flash market. TrendForce expects the continuing decline in prices to lead to a Q/Q decline in total NAND flash revenue in 4Q20.

Samsung

Its ASP fell by nearly 10% Q/Q for 3Q20 as the overall demand was adversely affected by the inventory reduction efforts that were taking place in the server segment. However, its bit shipments exceeded expectations for the same period and offset the price decline. The tightening of the US export restrictions in the middle of the quarter compelled Huawei to extend its component inventory “one last time” before being cut off from foreign suppliers. At the same time, Samsung benefitted from the stock-up demand related to the upcoming release of the iPhone 12 series. It saw a Q/Q increase of almost 20% in its NAND flash bit shipments for 3Q20. Thanks to this, its NAND flash revenue for the same quarter also rose by 5.9% Q/Q to $4.809 billion.

At the moment, Samsung is proceeding with the second-phase expansion of its Xi’an base as scheduled. As for developments in technology and products, the V5 (92L) process still accounts for the majority share of Samsung’s NAND flash output. To maintain cost competitiveness, Samsung will be stepping up efforts to get clients to adopt SSDs and UFS solutions featuring V6 (128L) NAND flash. The transition from the V5 to the V6 will become more pronounced in 2021.

Kioxia

Its bit shipments in 3Q20 increased by nearly 25% Q/Q thanks to its aggressive inventory building and the demand related to the releases of the iPhone 12 series and new game consoles. However, its ASP fell by around 9% Q/Q on account of the declining overall demand for NAND flash products. Despite the drop in prices, Kioxia posted a considerable revenue growth for 3Q20 because its earnings report for the period included the revenue from the SSD business unit that it acquired from Lite-On. The supplier’s NAND flash revenue went up by 24.6% Q/Q to $3.101 billion.

In the aspect of capacity planning, the company can add new production capacity at K1 but plans to keep its total wafer starts relatively constant to the end of 2021. Moving to product development, 96L products still account for the majority share of its supply. The production of 112L BiCS products is not expected to pick up noticeably until 2H21. It is worth noting that the firm just announced this October 29 that it will build a new production facility, designated as Fab7, at its Yokkaichi base. The construction is scheduled to begin in 1Q21, and the facility is set to contribute to the supplier’s output in 2022. With respect to products, Fab7 will probably focus on solutions after the BiCS6 gen.

Western Digital (WDC)

Its bit shipments increased by 1% Q/Q due to stronger-than-expected sales of storage products for the retail and gaming markets. However, its shipments of client SSDs and enterprise SSDs dropped noticeably because of inventory adjustments by clients in the PC and server segments. Moreover, its ASP fell by about 9% Q/Q because of the change in its product mix and the weakening of the overall demand. As a result, the firm was not able to prevent a decline in its quarterly revenue and recorded a Q/Q drop of 7.1% to $2.078 billion.

Turning to capacity planning, WDC will be collaborating with Kioxia to ready more production capacity at K1 and build the new Fab7 at Yokkaichi. These expansion activities will enhance WDC’s competitive position vis-à-vis the other major suppliers. As for product development, WDC will only begin to accelerate the transition to the BiCS5 (112L) technology in 2021. For now, most of its products are still based on the 96L BiCS4 technology. WDC will also being offering BiCS4 SSDs with the PCIe 4.0 interface in the near future.

SK hynix

It gives more weight to mobile solutions in its NAND flash product mix, so its bit shipments for 3Q20 grew by about 9% Q/Q on the backs of the new iPhone devices, new game consoles, and Huawei’s procurement activities. However, SK hynix was also affected by the inventory reduction efforts in the server segment. The share of SSDs in its NAND flash product shipments fell under 45% in 3Q20, and its ASP also dropped by around 10% Q/Q. Taken these factors altogether, company’s revenue for 3Q20 dipped by 3.1% Q/Q to $1.643 billion.

The firm will not make any significant changes to its production capacity. It is expected to maintain its wafer input levels to the end of 2021. To extend its cost advantage, it is pushing clients to adopt 96L and 128L solutions. The 128L process is expected to comprise around 30% of the supplier’s overall NAND flash output by the end of this year. However, the adoption of 128L solutions by server OEMs requires more time. Regarding SK hynix’s acquisition of Intel’s NAND flash business, the deal was announced this October 20. TrendForce points out that the deal will help strengthen SK hynix in the development of QLC NAND flash and enterprise SSDs, which are two areas that the company needs to improve. Through the acquisition of Intel’s assets, SK hynix will also become the world’s second-largest NAND flash supplier by market share.

Micron

Its revenue for its latest fiscal quarter dropped by 8.1% Q/Q to $1.53 billion. It has been optimizing its sales mix with a focus on reducing the share of channel-market wafers. Nevertheless, its ASP fell by nearly 8% Q/Q for its latest fiscal quarter (June-August) due to the downturn of the whole NAND flash market. The temporary wave of procurement initiated by Huawei helped Micron’s bit shipments, which were on par with the previous quarter.

On the technology front, the vendor has started to ship 128L products featuring Replacement Gate, which is its own transistor design. However, the supplier’s focus for next year will be on the market release of its 176L products. It intends to have most of its storage products for OEMs directly migrate to the 176L technology. These include client SSDs, UFS solutions, etc. The deliveries of 176L samples are scheduled to be completed before 2Q21. Furthermore, the firm is steadily raising the shipment share of QLC products. This indicates that Micron wants to be regarded as the main alternative to Intel in the QLC segment.

Intel

It experienced a substantial Q/Q decline of almost 25% in its bit shipments for 3Q20. Since it has a large market share for enterprise SSDs, the increasing pressure on server OEMs to reduce their component inventories turned this advantage into a disadvantage in bit shipments. Also, it suffered a Q/Q drop of around 10% in its ASP because of the weakening overall demand. With falling shipments and prices, its NAND flash revenue for 3Q20 registered a steep Q/Q decline of 30.5% to $1.153 billion.

In the aspect of capacity planning, Intel has no expansion plan for this year and intends to maintain wafer starts at its Dalian plant. For next year, it will undertake capacity expansion, though the long-term benefit of the additional capacity will mostly go to SK Hynix. Looking at plans related to products and technology, Intel remains focused on enterprise SSDs and has sent samples of 144L products to its clients. The production of 144L solutions is expected to begin ramping up in 2021.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter