History (1993): High-End Tape Cartridge Market Stumbles

Dims future for half-inch tape.

By Jean Jacques Maleval | September 23, 2020 at 2:12 pmOver the past several years, high-end cartridge drives have enjoyed great success satisfying the need for high-performance tape on mainframe systems.

“This market saturation, however, will combine with hard times in the mainframe market to constrain future demand for these products,” declares Robert C. Abraham and Raymond C. Freeman, Jr., authors of the newly-completed report from Freeman Associates (Santa Barbara, CA): Computer Tape Outlook – Half-Inch Products (223 pages, $1,950).

Performance enhancements, such as the introduction of 36-track models by IBM, have been unable to counter the slow growth of system sales.

“Despite stagnation at the high-end, widespread acceptance of compatible low-cost models has accelerated in active mid-range markets,” the authors wrote.

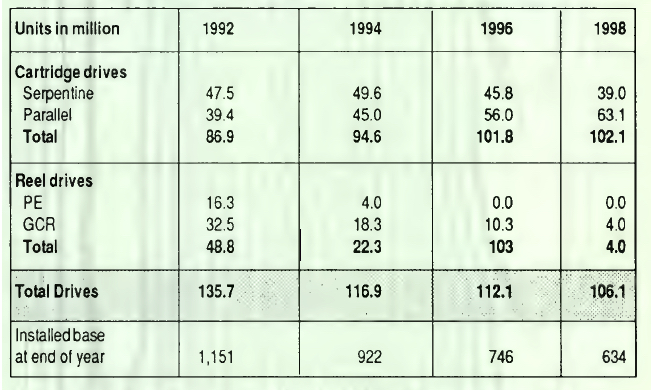

Reel drive markets will continue to wane, accounting for only 4% of half-inch tape drives shipped in 1998, and only 3% of revenue.

Buoyed by growth in the low cost segment, demand for 18- and 36- track parallel-recording tape subsystems will grow from 39,400 drives in 1992 to 63,100 drives in 1998, a CAGR of 8%.

Demand for much-lower-cost serpentine cartridge devices will remain relatively flat through 1994 before starting to roll off.

Shipments of PE and GCR reel tape drives will decline dramatically, with half of the product types ceasing to exist by 1995.

Flat projections for cartridge drives conceal dramatic product shifts

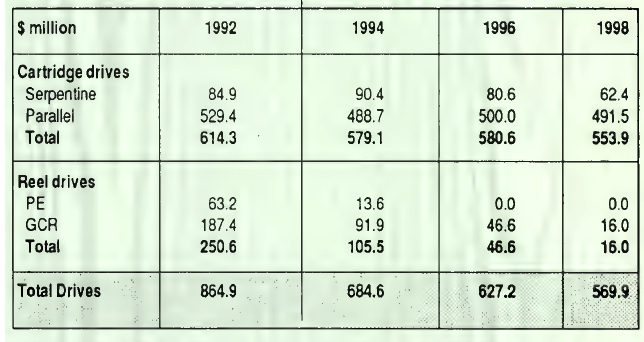

Freeman Associates predicts the WW market for all types of half-inch cartridge tape subsystems will drop to $554 million at OEM price levels in 1998, a compound rate of decline of 2% from the $614 million value of the 1992 market.

Unit shipments of these drives will grow at a 3% rate over that six-year period, from 86,900 transports in 1992 to 102,100 in 1998.

The report analyzes the important role of low-cost IBM-compatible cartridge subsystems, such as those already available from Cipher, Fujitsu, Laser Magnetic Storage, NEC, and Storage Technology. These drives – which comprise the only half-inch tape class forecast to grow over the six year period – are targeted at OEM accounts and can read and write tapes compatible with IBM 3480/3490 mainframe tape subsystems. Not intended as replacements for mainframe drives, these devices extend the use of parallel-recorded half-inch cartridges to smaller mid-range and network PC systems, facilitating data interchange. Shipments of these new products will swell from 8,300 units in 1992 to 45,100 units in 1998, an annual growth rate of 33%. Revenue will surge from $72 million to $266 million over the same 6-year period, an annual rate of 24%.

High-end parallel recording cartridge drives, principally IBM 3490 and compatible 18- and 36-track devices, will continue to serve the mainframe market. Shipments will decline at an 8% rate, from 31,100 in 1992 to 18,000 in 1998. Revenue for these subsystems will shrink from $457 million to $225 million, an 11% rate of decline. These revenue figures will remain the highest of any half-inch tape product class until 1997, when parallel low cost units will move ahead.

“Shipments of low cost serpentine recorded cartridge drives peaked at 72,000 units in 1989, dipped to 47,500 units in 1992 before rising slightly, finally declining to 39,000 units in 1998,” Freeman predicts. “This lackluster performance is partly the result of product delays and partly due to availability of newer low-end and mid-range devices such as DAT and 8mm helical scan drives and high capacity QIC products.”

The revenue for serpentine products is estimated to decline at a rate of 3% at OEM levels for 6-year period, dropping from $85 million in 1992 to $62 million in 1998 after peaking at $90 million in 1994. The longer duration of revenue growth reflects a change in mix to higher-performance higher-cost products.

End-of-life approaches for many reel classes

“Sales of half-inch reel-to-reel magnetic tape drives peaked in 1986. The last survivor in the reel market will be GCR streamer drives, comprising 100% of shipments of reel drives by 1997,” claims Abraham.

All other categories of reel drives are forecast to continue to subside and then terminate production during the 6-year forecast period.

Shipments of all GCR drives will drop from a peak of 71,000 in 1988 to 32,500 in 1992, then to 4,000 in 1998. Across the six-year period starting in 1992, this represents a 78% annual rate of decline.

The report analyzes specs of 120 models of tape drives produced by 24 manufacturers; 62 offerings from 12 media makers

Projected WW shipments all half-inch tape drives

Projected WW revenue all half-inch tape drives

This article is an abstract of news published on the former paper version of Computer Data Storage Newsletter on issue 64, published on May 1993.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter