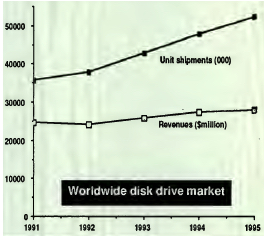

History (1992): Total Shipments of HDDs to Grow From 32.6 Million in 1991 to 52.4 Million in 1995

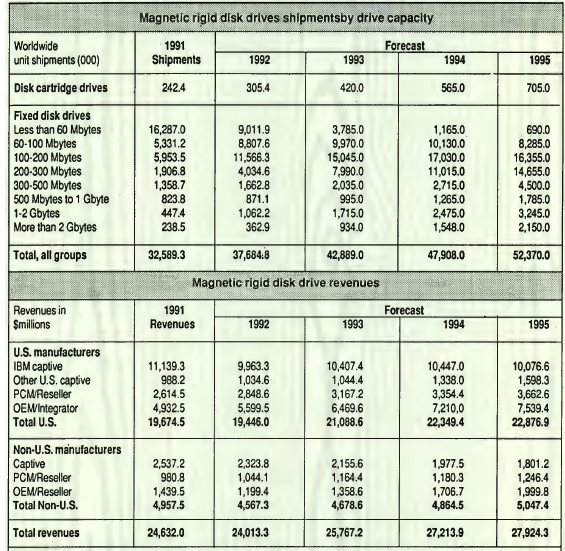

100-200MB group dominates in 1992.

By Jean Jacques Maleval | August 7, 2020 at 2:06 pmThe average disk drive capacities used for most computer applications have continued to increase faster than the industry expected, according to the 1992 Disk/Trend report on rigid disk drives ($1,985) published by Disk/Trend, Inc. (Mountain View, CA).

With estimated shipments of 11.6 million drives in 1992, rigid disk drives in the 100-200MB group now dominate the industry’s rigid disk drive output.

Changing software requirements for PCs have boosted the typical disk drive used with new PC’s into the 100-200MB range, but average disk capacities used with network file servers, technical workstations, minicomputers and mainframes are also increasing.

Forecasted average annual shipment growth for 200-300MB drives is 112.5% in the 1993-1995 period, and drives with over 2GB capacities will average 71.4% annual growth.

* Overall sales for the rigid disk drive industry are expected to be down 2.5% for 1992, the result of lower revenue for captive drives manufactured by system manufacturers and shipped with their own systems. However, non-captive drive revenue for 1992 are projected to increase 7.3%, and 1992’s estimated total revenue of $24 billion for all rigid disk drives are forecasted to grow to $27.9 billion in 1995.

* Total unit shipments of rigid disk drives are expected to grow from 32.6 million drives in 1991 to 52.4 million in 1995. 1991 shipments of 26 million 3.5-inch drives were 79.9% of the WW total for that year. Increased 3.5-inch drive shipments are expected in 1992 and 1993, but, by 1995, 3.5-inch shipments will start to decline in the face of competition from smaller drives. 1995’s 2.5-inch drive shipments are projected at 10.7 million, and shipments for 1.8-inch and smaller drives will rise to 7.2 million.

* The average price per megabyte is expected to continue to drop in all capacity ranges. The 1991 average of $2.76/MB for non captive 100-200MB drives is projected to be down to $1.60 on 1995, and the non captive average for 1-2GB drives is expected to decline from $1.48 to $0.62.

* As shipments by the WW industry increase, the number of participating companies continues to decline. Although 57 companies manufactured drives in 1991, the total has been reduced to 47 in 1992. During the past year, 16 companies stopped producing drives, typically because their small market shares prevented profitable business activities, and 6 new companies started rigid operations. Drive manufacturers headquartered in the US held 79.8% of WW revenue.

* Non captive revenue was $9.9 billion in 1991, with Seagate Technology continuing to hold market leadership, with 26.2% of the WW total. Conner Peripherals increased its share of WW non captive revenues to 15.7%, according to Disk/Trend.

Notes:

1. Revenue is reported at the price level at which drives are actually sold: captive, PCM/reseller or OEM/integrator. 2. Revenue for leased drives is reported on an “if sold” basis.

3. “PCM/reseller” means drives sold by manufacturers of plug compatible products or drives which are resold in the after market through wholesalers and dealers. “OEM/integrator” means drives sold to system manufacturers to be used as part of computer systems, plus sales to system integrators which assemble complete systems.

This article is an abstract of news published on the former paper version of Computer Data Storage Newsletter on issue ≠58, published on November 1992.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter