74.5% of Notebook PCs With SSDs in 2019

Compared to 83% with HDDs in 2004

This is a Press Release edited by StorageNewsletter.com on July 7, 2020 at 2:23 pmThis FOCUS ON: Notebook PC Storage Evolves was written by Trendfocus, Inc. on June 30, 2020.

Storage Devices for the Notebook PC Industry Continue to Innovate

The same number of options remain, but technologies have changed

The notebook PC market has seen significant changes over time in terms of storage devices used.

HDDs were the standard storage device for years and years. The notebook PC market was viewed in 2014, just 6 short years ago, as a still robust, high-volume market with new and exciting developments occurring.

Around that same time, some market observers thought that tablets, and to some extent smartphones, were bound to be the successor to notebooks. In 2014, 216 million tablets shipped worldwide. This was 20% higher than the 179 million notebook PCs that shipped that same year.

However, not so long after that, it became clear that notebook PCs were here to stay, even if volumes declined slightly each year. In 2019, the industry shipped between 140 and 150 million tablets, down from the >200 million unit range from 5 years earlier. The logic and use cases for the two separate devices were quickly realized; notebook PCs were for ‘content creation’ and tablets (and smartphones) were for ‘content consumption.’ The idea that notebook PCs would remain important was good news for the SSD industry, and to some extent, still, the HDD industry. SSD integration into notebook PCs had crossed the initial integration and acceptance stage and was now on the verge of a massive ramp. Creating new offerings and continuously lowering pricing to capture share in this massive market was a priority for all SSD players.

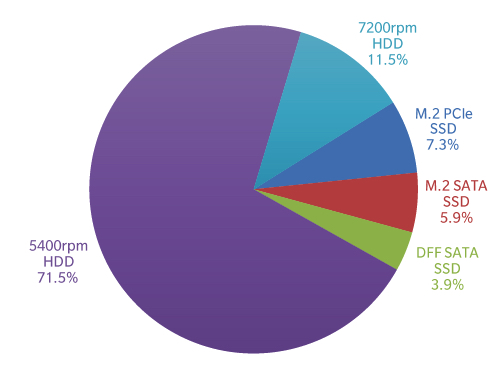

Chart 1: Total Notebook PC Market, by Storage Device

(units in million)

2014 Notebook PC TAM: 179 Million

In 2014, 83% of all notebook PCs utilized HDDs. These offerings came in a variety of options – including different z-heights, capacities, and spin speeds (namely 5,400rpm and 7,200rpm). HDD companies were still experiencing great volumes of sales of their products into this market.

The logic was that HDDs provided very high capacities at much lower prices, a priority for customers at the time. The somewhat still new (and extremely expensive) high-end options were SSDs.

Apple had led the charge with SSD adoption, mainly with an M.2-like PCIe module. However, this only equated to about 13 million units in 2014. Adding the other offerings available at the time, M.2 SATA and 2.5-inch SATA, accounted for approximately 30 million units of the total 179 million notebook PCs shipped that same year.

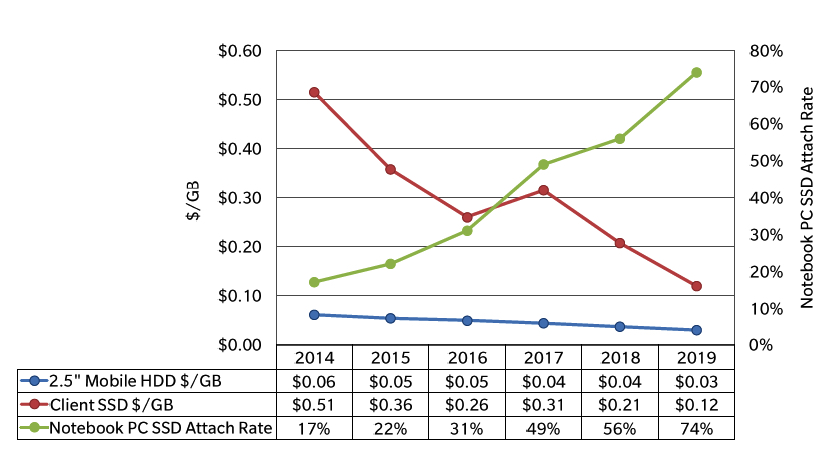

It is no surprise that the volumes were low as the average SSD price point was around $0.51/GB at that time, meaning a 128GB SSD for a notebook PC cost around $67. The average capacity for SSDs that year still had not reached 200GB, coming in at approximately 190GB. At that same time, 500GB HDDs were available for $38. A 1TB HDD could be had for about $52, a price 20% lower and capacity 780% higher than the sweet-spot SSD of the time.

It was very clear in terms of OEM strategy that SSDs were a high-end offering and price points reflected that, as did subsequent volumes. Even so, the industry managed an attach rate of approximately 17% for solid state storage that year. But the clock was ticking for HDDs in this market.

In 2014 and beyond, other OEMs started to branch out in their efforts to expand their SSD offerings. However, these products continued to be tied to higher performance and pricing tiers. Five years ago, consumers had many options. Notebook computers with an M.2 PCIe SSD (mainly from Apple) were on the market at extremely high price points. Below that, there was M.2 SATA – still a very good, much higher performing solution compared to HDDs, and also in a form factor allowing for much slimmer computers.

After that, there were the remaining 2.5-inch options. Although there were offerings with 2.5-inch SATA SSDs, many users still opted for HDDs which dominated volumes as price points and economies of scale still lagged for client SSD offerings, not to mention that NAND output levels were insufficient to support such a market.

The commercial PC market was enjoying some success with SSD migration as lower capacities and higher average system prices were more acceptable for this segment. By 2015, the overall market SSD attach rate was greater than 22% – over 1/5 of the market, but still no hockey stick effect.

Drastic Price Drops Help SSD Integration

Fast forward 2 years to 2017, and a 500GB HDD was still in the mid-$30s, while a 1TB HDD had dropped to approximately $48. SSDs of the same capacities at that time were approximately $160 and $320, respectively. However, a 128GB SSD could be had for $41 in 2017. The market did see a slight increase in pricing from 2016 to 2017 for SSDs due to supply constraints, but as history has shown, these short adjustments upwards tend to be temporary.

Once supply caught backup after multiple NAND vendors ramped 3D NAND, pricing continued downward. During that time, M.2 PCIe still commanded a premium over M.2 SATA, albeit a very slight premium (but pennies matter in this market segment).

Nonetheless, OEMs had started aggressively down the M.2 PCIe path. Apple was not the only game in town by that point. In 2017, M.2 PCIe shipments increased to 46.4 million units, a 257% jump in just 3 years – pretty amazing considering major OEMs have a limited number of design-cycles each year and that the decision to switch entailed migrating to not only a new form factor, but also a new protocol. In addition, adoptees were starting to feel comfortable with the number of SSD vendors offering like-for-like solutions as multiple supplier strategies were now more prevalent.

At this time, M.2 PCIe was mainly available in a 2280 form factor. This had become the sweet spot for nearly all deployments. HDDs continued to decline as a function of the accelerating SSD attach rate. In 2017, 49% of notebook PCs now included SSDs. 163 million notebook PCs shipped, utilizing 80 million SSDs and 83 million HDDs. This would grow to a 56% attach rate the following year, in 2018.

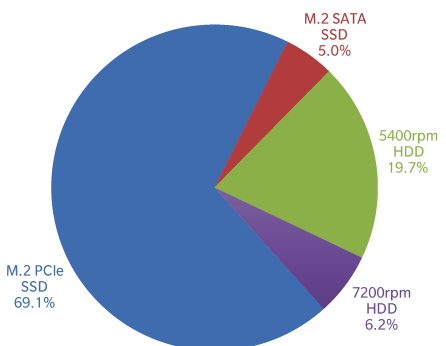

Chart 2: Total Notebook PC Market, by Storage Device

(units in million)

2019 Notebook PC TAM: 181 Million

Solid State Drives Rule

Entering 2019, it was very clear that HDDs were now a thing of the past for notebook PCs, even with HDD pricing still very favorable at $35 for a 500GB drive and $36 for 1TB. Notebook OEMs believed greater value (experience) was seen with SSDs – both in terms of form factors (slimmer designs) and fantastic performance. All this occurred even while SSD pricing was still much higher than that of HDDs. A 512GB SSD cost around $59, however, 128GB and 256GB offerings now cost less than a 500GB HDD, at $21 and $31 respectively. By 2019, 128GB SSDs had experienced a 53% decline in pricing in just two short years.

There was major price elasticity with these new offerings. Many users were now very comfortable moving to a lower-capacity offering knowing that every other attribute of the product as well as the overall user experience would be better with an SSD. The attach rate for 2019 reached 74%. Of the SSDs in notebook PCs, M.2 PCIe was now definitely the storage solution of choice. It represented over 69% of all notebooks builds in 2019. In just five short years it had taken over the number one position held by 5,400rpm HDD drives in the market. It is important to note that this solution was still, on average, $0.12/GB, whereas an HDD’s average price was just $0.03/GB (and this doesn’t change much anymore Y/Y.) M.2 PCIe unit growth had climbed 955% in 5 years with a $/GB price point 400% higher than an HDD $/GB price point.

This massive ramp in SSD integration was obviously enabled by continuous NAND and controller technology improvements. With each gen, NAND densities became greater, and at the same time, less expensive. For controller companies, innovation continued with each new NAND gen, helping with NAND management, performance, and overall cost structures. Those cost benefits contributed to drastic declines in pricing over the years – declines that were perhaps a bit too aggressive in certain respects, sacrificing margins.

As seen with the 2019 splits in Chart 2 above, there are still varying options for choosing storage devices. However, PCIe as an option gets even more detailed within that broad category.

Companies such as Phison and SMI have enabled many SSD vendors to offer lower-cost solutions (value PCIe) in place of SATA SSDs – ensuring increased performance at a great value to their customers. The value PCIe segment is quickly becoming the volume PCIe SKU for some SSD vendors and the volume swim lane for not only client PCIe in general, but all client OEM offerings. This swim lane will, at some point, become the volume SKU across the board. The lower-tier SATA SSD swim lane quickly become suppressed by ‘value PCIe’. This offering, helped by both aggressive pricing and new NAND technologies that fostered lower costs, allowed notebook OEMs to embrace multiple swim lanes for SSDs even if they were using the same protocol. In effect, not tying swim lanes to different protocols, but to different performance levels within the same protocol.

Chart 3: Notebook PC Storage $/GB, by Storage Device

Additional Notebook PC Storage Options Arise

Back in 2014, there were 5 main storage options for notebooks: 5,400rpm HDD, 7,200rpm HDD, 2.5-inch SATA SSD, M.2 SATA SSD, M.2 PCIe SSD. Now, M.2 PCIe can be split into three additional swim lanes – performance, mainstream, and value. So, adding the 3 separate categories for PCIe, the market went from 5 categories in 2014 to 6 categories today.

However, like the market has seen with other product categories where too many swim lanes for a similar class of product exists, one of these categories usually gets squeezed out – and this would mean ‘mainstream’ probably gets squeezed out in this case. This can be for one of many reasons: streamlining qualifications, supply issues, SKU management, minimizing/simplifying complicated configurations, etc. In the end, vendors wind up trying to separate too many attributes to too many pricing tiers. And with SSD pricing tiers only differing by one or two pennies now, less may be more in this situation. It makes sense that the ‘value’ and ‘mainstream’ swim lanes become one.

Another storage option for major notebook OEMs that has been squeezed out as of late is the SATA SSD swim lane. DFF SATA quickly gave way to M.2 a few years ago. Then, rather quickly, M.2 SATA gave way to M.2 PCIe. Trendfocus estimates that of all the M.2 SATA SSDs that shipped in the market last year, only about three million units went to major OEM builds. Value PCIe has been replacing SATA SSDs for that swim lane.

Even within M.2 for PCIe, we have seen further differentiation when it comes to form factors. Current varying dimensions include 2230, 2242, and 2280, and even standalone BGA in some very limited cases. BGA has not seen much volume for PCs, and we do not anticipate to change much in the future. There continues to be a lot of interest in standalone BGAs, but this market needs to mature before any sizable adoption tales place. The question becomes, how many different modules (dimensions) will the industry be willing to support? If 2280 has worked well for a number of years now, and PCIe gen 4 will most likely requires this dimension, why not standardize around this and benefit from economies of scale, SKU management, and multiple supplier benefits, as well as minimizing the number of qualifications required?

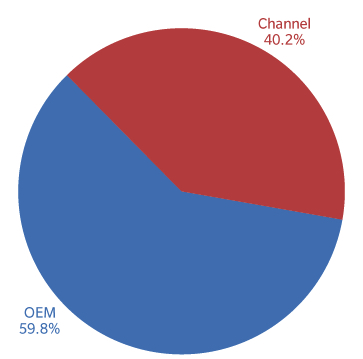

Chart 4: Client SSD Market, Channel Vs. OEM

(units in million)

1CQ20 Client SSD TAM: 69 Million

SATA Offerting See a Long Tail

The entire discussion has centered around major OEM notebook solution and how they have evolved over the years. However, the channel/aftermarket is still responsible for a large portion of the volume each year. For some SSD vendors, their SSD shipment splits are different with OEM business. Some SSD vendors could be well diversified when it comes to high-end PCIe, mainstream/value PCIe, and still low-end SATA, including 2.5-inch, where they serve both major OEM business and the channel/aftermarket segment.

As the Chart 4 above illustrates, OEM business represents about 60% of all SSD units shipped – which means 40% goes to the lower-tier and channel markets. PCIe has enjoyed significant growth at the major OEM companies, with channel lagging behind with integration to this not-so-new technology. Some vendors may be more focused on just the channel/aftermarket segment where SATA (especially 2.5-inch SATA) still proliferates with a great number of opportunities. This has been a very good business for the vendors committed to it. For some SSD vendors who have maintained resources and strategies to support this market, SATA remains a viable and in-demand solution. For other vendors who have had their challenges in the channel and have maybe been OEM-focused as their main strategy over the years – PCIe has been and will be their priority for years to come. They could essentially drop all SATA support from their offerings and not miss too much opportunity as a function of the market they serve. Again, for the vendors who do focus strictly on the channel – SATA is their bread and butter and will be for a number of years going forward.

Conclusions, Analysis: Innovation Continues in a Mature Market

In just five short years, the notebook PC market has largely transitioned away from hard disk drives to solid state drives. The market has gone from notebook PC configurations that comprised the vast majority of HDD offerings, including different spindle speeds, z-heights, and capacities with just a small portion of SSDs at the very high end to the vast majority of offerings incorporating SSDs. Even so, the market is still filled with multiple options driven by different technology offerings tied to performance. The options with HDD z-heights (5mm, 7mm, 9.5mm, 12.5mm) have become form factor options for SSDs such as 2280, 2230, and 2242. Over the next couple of years, there will be some consolidation – PCIe will converge with the value and mainstream segments becoming one category, while performance level (premium) solutions will remain. Even with that said, some SATA offerings (2.5-inch and M.2) will have a long tail in certain markets, especially in the channel due to legacy system upgrades and lagging technology transitions, sometimes by choice and sometimes due to lack of resources to transition. Another reason may be to simply maintain a lower-priced tier to sell to the market segment that desires that. A couple points are clear – the notebook PC market, over the long term, is still active, is still alive and well and the SSD industry has ensured that storage options will continue to proliferate and provide increased value and performance with each new design.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter