WW Converged Systems Market Up 4.5% Y/Y in 1Q20 to $3.9 Billion

As branded, Dell leader in front of Nutanix and HPE

This is a Press Release edited by StorageNewsletter.com on June 19, 2020 at 2:23 pmAccording to the International Data Corporation‘s Worldwide Quarterly Converged Systems Tracker, WW converged systems market revenue increased 4.5% Y/Y to $3.9 billion during 1Q20.

“The overall converged systems market showed resilience during a difficult macro environment in the first quarter of 2020,” said Sebastian Lagana, research manager, infrastructure platforms and technologies. “While the hyperconverged system market continued to expand as enterprises seek to take advantage of software-defined infrastructure, the certified reference systems and integrated infrastructure segment posted its best quarter of growth since 2Q19 on the strength of richly configured platform sales related to demanding workloads in industries such as healthcare and telecoms.”

Converged Systems Segments

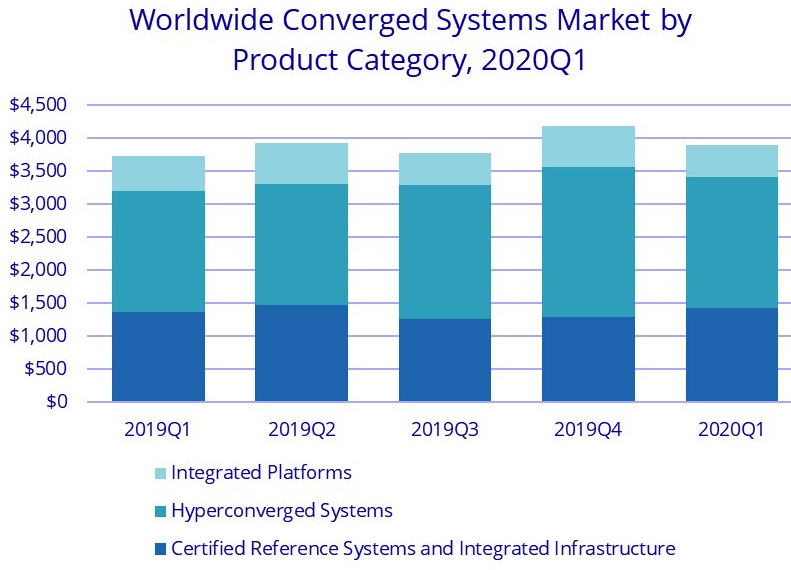

IDC’s converged systems market view offers three segments: certified reference systems and integrated infrastructure, integrated platforms, and hyperconverged systems.

The certified reference systems and integrated infrastructure market generated just over $1.4 billion in revenue during 1Q20, which represents growth of 4.4% Y/Y and accounts for 36.8% of all converged systems revenue.

Integrated platforms sales declined 8.7% to $3.9 billion in 1Q20, generating $478 million worth of revenue. This amounted to 12.3% of the total converged systems market revenue.

Sales of hyperconverged systems grew 8.3% to $3.9 billion Y/Y during 1Q20, generating just under $2.0 billion worth of revenue. This amounted to 50.9% of the total converged systems market.

IDC offers two ways to rank technology suppliers within the hyperconverged systems market: by the brand of the hyperconverged solution or by the owner of the software providing the core hyperconverged capabilities.

Rankings based on a branded view of the market can be found in the first table below and rankings based on the owner of the hyperconverged software can be found in the second table below. Both tables include all the same software and hardware, summing to the same market size.

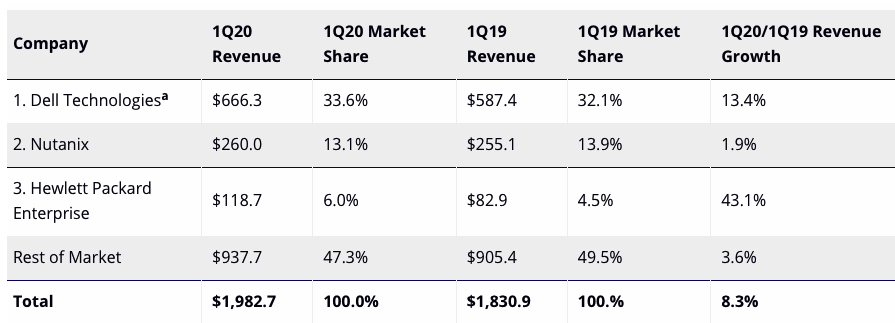

As it relates to the branded view of the hyperconverged systems market, Dell Technologies was the largest supplier with $666.3 million in revenue and a 33.6% share. Nutanix generated $260.0 million in branded hardware revenue, representing 13.1% of the total HCI market during the quarter. Hewlett Packard Enterprise finished the quarter in the ≠3 spot with $118.7 million in revenue, which amounted to a 6.0% share.

Top 3 Companies, WW Hyperconverged Systems as Branded, 1Q20

(revenue in $million)

a Dell Technologies represents the combined revenues for Dell and EMC sales for all quarters shown.

a Dell Technologies represents the combined revenues for Dell and EMC sales for all quarters shown.

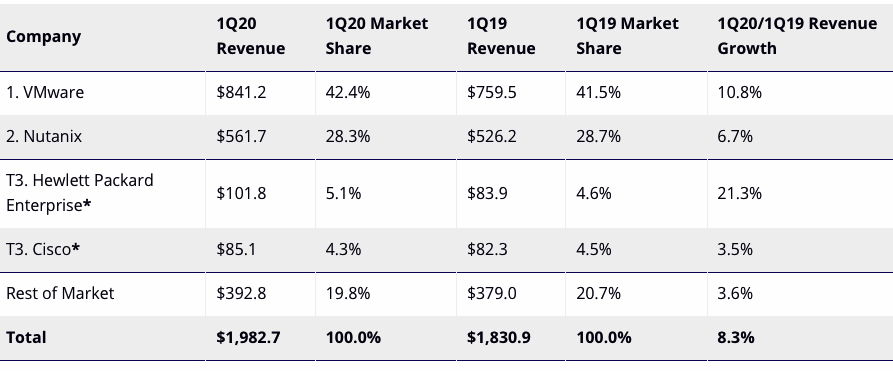

The rankings based on the owner of the hyperconverged software show that new systems running VMware hyperconverged software represented $841.2 million in total 1Q20 vendor revenue, or 42.4% of the total market. Systems running Nutanix hyperconverged software represented $561.7 million in first quarter vendor revenue or 28.3% of the total market. Both amounts represent the value of all HCI hardware, HCI software, and system infrastructure software sold, regardless of how it was branded at the hardware level. As hardware sales are a major factor in these data, the chart should not be assumed to solely reflect, or completely align with, the respective companies’ overall software performance.

Top 3 Companies, WW Hyperconverged Systems Revenue Attributed to Owner of HCI Software, 1Q20

(revenue in $million)

* IDC declares a statistical tie in the WW converged systems market when there is a difference of one% or less in the share of revenues or unit shipments among two or more vendors.

Taxonomy Notes

Beginning with the release of 2019 results, IDC has expanded its definition of the hyperconverged systems market segment to include a new breed of systems called disaggregated HCI (hyperconverged infrastructure). Such systems are designed from the ground up to only support distinct/separate compute and storage nodes. An example of such a system in the market today is NetApp’s HCI solution. They offer non-linear scaling of the hyperconverged cluster to make it easier to scale compute and storage resources independent of each other while offering crucial functions such as QoS. For these disaggregated HCI solutions, the storage nodes may not have a hypervisor at all since they do not have to run VMs or applications.

IDC defines converged systems as pre-integrated, vendor-certified systems containing server hardware, disk storage systems, networking equipment, and basic element/systems management software. Systems not sold with all four of these components are not counted within this tracker. Specific to management software, IDC includes embedded or integrated management and control software optimized for the auto discovery, provisioning and pooling of physical and virtual compute, storage and networking resources shipped as part of the core, standard integrated system. Numbers in this press release may not sum due to rounding.

Certified reference systems and integrated infrastructure are pre-integrated, vendor-certified systems containing server hardware, disk storage systems, networking equipment, and basic element/systems management software. Integrated platforms are integrated systems that are sold with additional pre-integrated packaged software and customized system engineering optimized to enable such functions as application development software, databases, testing, and integration tools. Hyperconverged systems collapse core storage and compute functionality into a single, highly virtualized solution. A key characteristic of hyperconverged systems that differentiate these solutions from other integrated systems is their scale-out architecture and their ability to provide all compute and storage functions through the same x86 server-based resources. Market values for all three segments includes hardware and software but excludes services and support.

IDC considers a unit to be a full system including server, storage, and networking. Individual server, storage, or networking nodes are not counted as units. Hyperconverged system units are counted at the appliance (aka chassis) level. Many hyperconverged appliances are deployed on multi-node servers. IDC will count each appliance, not each node, as a single system.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter