History (1992): Optical Disk Drives Market Nudge One Million Unit Mark in 1991

On way to 3.1 million in 1997

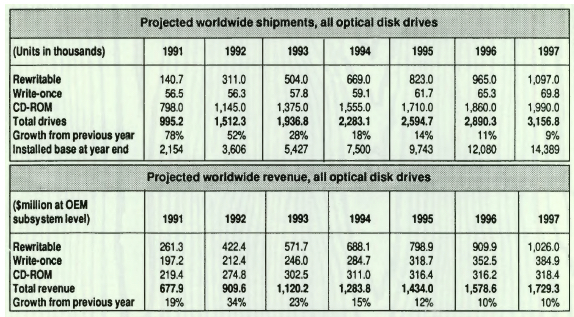

By Jean Jacques Maleval | May 19, 2020 at 2:22 pm“The optical disk drive industry shipped 995,000 units in 1991 and is projected to deliver more than 1.5 million units in 1992 – a 52% growth – on its way to a 3.1 million unit year in 1997,” according to Robert C. Abraham and Raymond C. Freeman, Jr., authors of the 317-page report ($1,950) from Freeman Associates Inc. (Santa Barbara, CA): Optical storage Outlook, 1992.

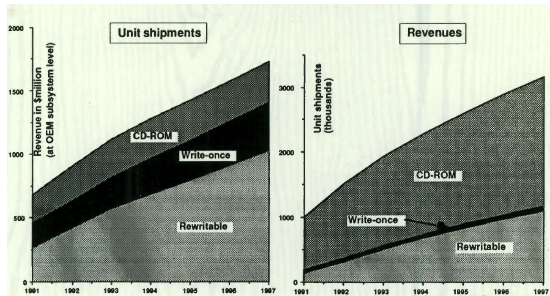

“CD-ROM drives led the shipment parade in 1991, accounting for 80% of all optical units shipped, while rewritable optical devices moved ahead of write-once drives that year for the first time as the optical revenue leader. Total drive shipments for 1991 were up 67% over 1990 levels, while revenue was up by 19%,” reported Freeman. “This difference in growth rates is due to the much higher unit growth rate for CD-ROM drives – the lowest priced optical category – and failing prices for all categories of optical products.“

According to the newly completed market analysis, the worldwide market for all types of optical disk drives will exceed $1.7 billion at OEM price levels in 1997, a 17% CAGR the $678 million value of the 1991 market.

Revenues for 1997 are divided between rewritable and multifunction products at $1,026 million (59% of total revenue); write-once devices at $385 million (22%); and CD-ROM drives at $318 million (19%).

CD-ROM drives will be the predominant class through the forecast period in terms of unit volumes.

Rewritable and multifunction drives wrested away the lead in revenue from write-once drives in 1991 and will dominate optical revenues thereafter.

Rewritable and multifunction products will gain broad acceptance

Unit shipments of rewritable optical disk drives (which include multifunctional versions) will rise dramatically through 1997. Revenues from rewritable drives will grow steadily as OEMs and system integrators employ these products in new applications.

“Multifunction drives will become the workhorses of the optical world, capable of write-once and/or read-only modes of operation in addition to their native rewritable mode,” states Freeman.

Essentially all rewritable drives during the forecast period will be of capacities below 1GB.

Total rewritable/multifunction shipments will rise from 140,700 drives in 1991 to 1.1 million drives in 1997, a CAGR of 41%. Revenues during that period will grow from $261 million to $1,026 million, a rate of 26%.

Revenue from rewritable drives overtook CD-ROM drives in 1989, passed write-once drives in 1990, and will achieve nearly 1.5x their combined dollar volume in 1997.

Unit shipments of 3.5-inch drives will surpass 5.25-inch drives in 1993, but will lag in revenue throughout the forecast period.

Write-once buyers shift to larger diameter or multifunction drives

Dramatic shifts are taking place among the 4 product classes comprising the write-once segment: write-once CD (writes on 4.72-inch diameter disks in the CD-ROM format), traditional 5.25-inch products, and 2 high-end classes utilizing 12-inch or 14-inch disks.

Dedicated write-once users are quietly abandoning 5.25-inch diameter products and opting for either larger diameter write-once or 5.25-inch multifunction products, which include a write-once function.

These market shifts have caught some vendors guard, while others were able to exploit the changes,” declares Abraham.

Write-once versions led the optical drive market in terms of revenue from 1983, until being overtaken by rewritable/multifunction devices in 1991. Unit shipments of WORM drives were only 6% of all optical shipments in 1991, but accounted for 29% of total optical revenues. Write-once unit shipments are expected to drop to only 2% of total optical shipments in 1997, but revenue will still account for 22% of the total.

These disparate ratios are due to the large differential in average unit prices between write-once and the other optical product classes.

The heightened change in the ratio further reflects the shift within write-once to the more expensive large diameter products.

Due to the shift from write-once to multifunction devices, shipments of 5.25-inch WORM drives will decline from their peak of 46,000 units in 1991 to zero units in 1997. The lower-performance of the two large diameter classes will also decline from its 1989 peak of 11,000 units to zero units in 1995. Of the two classes of write-once drives remaining in 1997, 53% of unit shipments and 6% of revenues will be from the write-once CD class; 47% of units and 94% of revenues will come from drives in the greater than 3GB category.

CD-ROM market growth boosted by new applications, lower costs

Multimedia applications, a steady flow of new CD-ROM titles, and declining hardware, software, and replication costs have broadened the market for CD-ROM technology. Unit shipments are predicted to reach 2 million drives in 1997, up 16% annually from the 798,000 units in 1991. Revenue will grow from $219 million in 1991 to $318 million in 1997, an annual rate of 6%.

Production of CD-ROM drives will continue to be dominated by Japanese manufacturers and Philips in the Netherlands (marketed by Laser Magnetic Storage International) because of their established positions in the CD audio market.

The report predicts that no US manufacturer will enter the CD-ROM drive manufacturing business. Involvement by US companies in CD-ROM will continue to be extensive but will occur in electronic publishing, marketing, systems integration, and disk replication.

The report identifies 102 models of rewritable, write-once, and CD-ROM drives produced worldwide by 33 manufacturers and 88 offerings from 27 optical disk media makers. It lists 26 disk preparation service companies, 33 representative CD-ROM service companies and 23 representative electronic publishers.

Worldwide market projections, all optical disk drives

This article is an abstract of news published on the former paper version of Computer Data Storage Newsletter on issue ≠50, published on March 1992.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter