History (1991): Decline of FDD Market for First Time Since 1985

Drop of 1.3% in units shipped in 1991

By Jean Jacques Maleval | April 28, 2020 at 2:31 pmFor the first time since 1985, both shipments and revenue for flexible disk drives in 1991 are expected to be lower than the previous year.

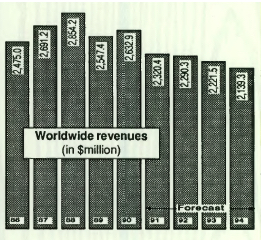

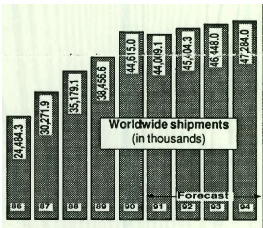

WW unit shipments in 1991 are projected at 44 million drives, according to the released 1991 report from Disk/Trend (Mountain View, CA), a drop of 1.3%. 1991 revenue for floppy drives is forecasted at $2.3 billion, down 11.8%. Growth in unit shipments is expected to resume in 1992, but average annual shipment increases in the 1992-94 period are expected to average only 2.3%.

Continuous changes in the industry’s product mix and limited expansion of PC applications for floppy drives will hold down growth in unit shipments.

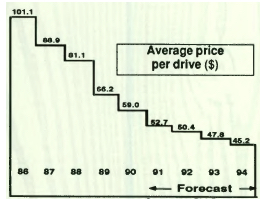

Total industry revenue is expected to decline 2.5% during the same period, under pressure from intense competition and dropping prices.

Here are other highlights from the 1991 Disk/Trend report ($1,380) on flexible disk drives:

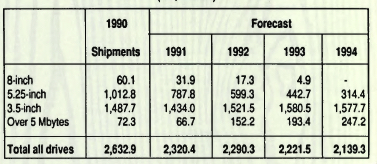

- Microfloppies, mostly 3.5-inch models, have become the dominant product group in the floppy drive industry. 66% of the floppy drive industry’s 1990 shipments were microfloppy drives, with the 1994 total forecasted at 82%. 5.25-inch minifloppy drives led the industry’s shipments until 1988, but dropped to a 33% share in 1990, with a further decline to 14% forecasted for 1994.

- The trend to increased capacity in the microfloppy form factor remains strong. Microfloppy drives with unformatted capacities of 1MB or less were only 22.6% of the microfloppy total in 1990. Drives with 1.6 to 2MB capacity held 77.4% of 1990 microfloppy drive shipments, with 1994 projected at 85.8%. New drives with 4MB unformatted capacity were adopted by IBM in 1991 for a new PS/2 personal computer model, and 8.3% of the 1994 shipment total for all microfloppy drives is expected to be diverted to the 4MB models.

- Throughout the history of the floppy drive industry, there has been a movement to smaller form factors, and the miniaturization trend continues with 3.5-inch microfloppy drives. The first 3.5-inch drives introduced by Sony in 1982 were 2 inches in height, but most of the industry followed the lead of Citizen Watch, which introduced one-inch high drives in 1984. The demand for even smaller drives is providing a new challenge, with some new drives only one inch in height. One-inch high drives held 78.2% of 1990 WW microfloppy drives shipments, but drives with heights of 3/4 inch or less are forecasted to capture 77.9% of 1994 shipments.

- After years of delays, volume production capability for high capacity 3.5-inch floppy drives was established in 1991, with more to come in 1992. Lack of interchange standards between the US and Japanese drive manufacturers active in the field will cause confusion among potential buyers, but Disk/Trend forecasts for 3.5-inch high capacity floppies anticipate significant growth, to 1.3 million drives in 1994.

- Sony originated the 3.5-inch floppy format and continued to hold leadership in 1990 shipments of non-captive drives, with 20.5% of the WW unit shipment total. Teac increased its lead in the 5.25-inch drive market to 29.1% of the WW noncaptive drive shipments. Y-E Data continued to lead the small remaining market for 8-inch floppy drives with 71.6% of 1990 shipments, and Iomega increased its lead in high capacity floppy drives with 91.9% of the non-captive unit shipments, mostly 5.25-inch models.

The report also contains basic product specs on 235 disk drives and profiles on 53 existing and former manufacturers of flexible disk drives.

Flexible disk drives WW unit shipments (in thousands)

Flexible disk drives WW revenues (in $million)

This article is an abstract of news published on the former paper version of Computer Data Storage Newsletter on issue ≠47, published on December 1991.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter