Software-Defined-Storage Market to Reach $86 billion by 2023

28% CAGR from 2019

This is a Press Release edited by StorageNewsletter.com on March 19, 2020 at 2:20 pmThe software-defined-storage (SDS) market is expected to register a 28% CAGR from 2019 through 2023 to reach $86 billion as vendors expand product offerings to meet rising demand, according to Omdia, a registered trademark of Informa PLC.

As storage capacity grows due to the accumulation of data for video, big data, data analytics, AI and ML, an increasing portion of data center storage- spend is expected to shift towards SDS storage, which is suited for this new type of data retention and processing.

The SDS market comprises hyper-converged infrastructure (HCI) and standalone SDS products.

“HCI has become a runaway hit because of its ease of deployment and ongoing operation,” said Dennis Hahn, principal analyst, data center storage, cloud and data center research practice, Omdia. “HCI represents an affordable way to add capacity, with small enterprises able to configure and manage the technology using generalists on their staff. Many enterprises like HCI as a pragmatic solution for meeting their immediate growth challenges. In contrast, a core data center storage solution would likely entail the use of skilled administrators to conduct equipment integration into the data-center infrastructure.”

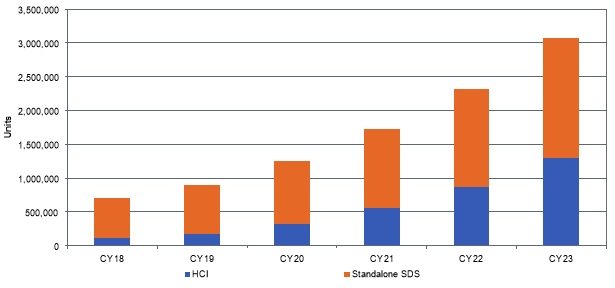

HCI shipments are estimated to have grown 24% Y/Y in 2019, achieving a 56% 4-year CAGR in 2023. Meanwhile, standalone SDS (non-HCI) shipments grew 12% in 2019, to achieve a 21% 5-year CAGR in 2023.

Furthermore, HCI is forecasted to reach $43 billion by 2023, rising at a 5-year CAGR of 47%, whereas standalone SDS is forecasted to reach $42 billion by 2023 for a 5-year CAGR of 18%, according to Omdia’s Data Center Software Defined Storage Market Trackerhttps://technology.informa.com/620865/data-center-software-defined-storage-market-tracker.

In 2CQ19, HCI revenue totalled $1.9 billion, up 27% Y/Y and standalone SDS amounted to $4.3 billion, down 12% Y/Y.

Furthermore, factory-defined comprised 33% of the standalone SDS market in terms of units during the same period, with file was at 42%, object at 20%, block at 18%, all-in-one at 13% and unified at 7%.

Cloud service providers contributed 43% of total SDS revenue in 2019. In contrast, telco service providers contributed a mere 4%.

Software defined storage unit forecast

Slow but steady rise in the adoption of standalone SDS storage

Standalone SDS storage has been slower to take off in the enterprise, although it provides lower costs than traditional storage and allows independent server and storage scaling.

Slowing standalone SDS adoption has been attributed to a lack of standards to help users marry their independent choice of SDS hardware to SDS software. However, as compatibility issues are worked out, standalone SDS is expected to gain increasing market traction.

Standalone SDS separates the purchasing of storage hardware from the software, providing choices for buyers. Hardware options come with multi-vendor sourcing, allowing users to hunt for options and enhance bargaining power.

Cloud service providers have bee committed to SDS for several years because they have the in-house skills to make it work. Enterprises are just beginning to seriously try the approach, often as an appliance offering, to assess its payback.

During the next 4 years, vendors are expected to increasingly drive up performance to further enable compatible hardware/software options. Standards, such as those developed by the Open Compute Project, allow for the creation of storage solutions that provide consistent storage deployment and associated support, hence reducing the level of skills required.

Highlights from report include:

• HCI is forecasted to reach $43 billion by 2023, for a 5-year CAGR of 47%.

• Standalone SDS is forecasted to reach $42 billion by 2023 for a 5-year CAGR of 18%.

• HCI revenue was $1.9 billion, up 27% Y/Y in 2CQ19 and standalone SDS was $4.3 billion, down 12% Y/Y.

• Factory-defined represented 33% of standalone SDS units in 2CQ19, with file (42%), object (20%), block (18%), all-in-one (13%), and unified (7%) by access method.

• Cloud service provider accounted for 43% of total SDS revenue in 2019, telco service provider was 4%, and enterprise was 53%, with enterprise going to 65% in 2023.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter