History (1991): Users Shifting to Multifunction Optical Drives – Freeman Report

Unit shipments of CD-ROM and rewritable and multifunction units will rise dramatically through 1996.

By Jean Jacques Maleval | March 18, 2020 at 2:18 pmMajor shifts within the optical storage market are forecast to occur between now and 1996.

The availability of multifunction optical disk drives is causing prospective 5.25-inch write-once users to shift toward this newest class of optical devices.

Meanwhile, users of 12- and 14-inch write-once products are quietly abandoning low-end versions and migrating to higher capacity and performance next gen products.

“These rapid shifts within the market are catching some vendors off-guard while others are capitalizing on the changes, “declares Robert C. Abraham and Raymond C. Freeman, Jr., authors of the 326-page Freeman Report: Optical storage Outlook, available for $1,950 from Freeman Associates (Santa Barbara, CA).

These shifts did not dampen users’ enthusiasm for optical products, however.

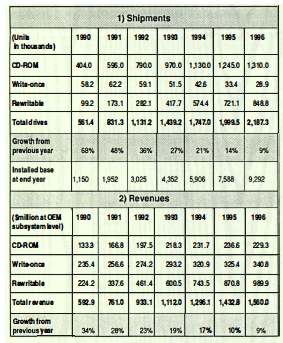

“Total drive shipments for 1990 were up 68% over 1989 levels, and 1990 revenues outstripped 1989 by 34%,” reported Freeman.

Unit shipments of CD-ROM drives and rewritable and multifunction drives will rise dramatically through 1996. Revenues from rewritable and multifunction optical disk drives will grow steadily as OEMs and system integrators employ these new products. Rewritable optical disk drives exhibit many of the same characteristics as magnetic disk drives but offer the added feature of media removability.

“Multifunction drives are the chameleon of optical products, capable of operating in multiple modes of operation depending on the type of optical media in use,” states Abraham. “Most of these drives will incorporate a rewritable mode.“

The WW market for all types of optical disk drives will exceed $1.5 billion at OEM price levels in 1996, an 18% compounded growth rate from $593 million value of the 1990 market. Annual shipments of drives will exceed 2.1 million units in 1996. Projected unit shipments for 1996 total 1.3 million CD-ROM drives (60% of total optical disk drives), 28,900 write-once units (1%), and 848,000 rewritable and multifunction devices combined (39%).

The composite total of these unit shipments represents a compounded growth rate of 25% during the six-year period from 1990 through 1996.

Revenues shares for 1996 are divided quite differently from unit shipments.

CD-ROM drives, at $229 million, will account for only 15% of total revenue stated at OEM levels. Write-once devices will represent $341 million, or 22% of total dollar volume, and rewritable and multifunction products will achieve a 63% share of 1996 revenues with $990 million.

CD-ROM drives will be the predominant class through the forecast period in terms of unit volumes. Write-once drives will relinquish their lead in revenue to rewritable and multifunction drives in 1991. Rewritable and multifunction revenues will dominate the optical market thereafter.

CD-ROM market place quickens

After several sluggish years, the market for CD-ROM drives for all data applications is now growing rapidly. Declining hardware, software, and replication costs have broadened the market for CD-ROM technology. Unit shipments are predicted to be at 1.3 million drives in 1996, up 22% annually from 404,000 units in 1990.

Revenue will grow from $133 million in 1990 to $229 million in 1996, an annual rate of 9%.

Production of CD-ROM drives will continue to be dominated by Japanese manufacturers and Philips in the Netherlands (marketed by Laser Magnetic Storage International) because of their established positions in the CD audio market.

The report predicts that no U.S. manufacturer will enter the CD-ROM drive manufacturing business. Involvements by U.S. companies in CD-ROM will continue to be extensive but will occur in electronic publishing, marketing, systems integration, and disk replication.

Write-once revenue lead fades

Write-once versions have led the market for optical disk drives since 1983 in terms of revenue, but will finally yield to rewritable/multifunttion devices in 1991. While 1990 unit shipments of write-once drives were only 14% of the level of CD-ROM drives, write-once revenues were 177% of CD-ROM revenues. Write-once revenue is expected to be 149% of CD-ROM in 1996 despite comparable unit shipments of only 2% that year.

This disparate ratio, due to the large differential in average unit prices between the two product classes, further reflects the shift within write-once to high-end products.

Write-once drives with capacities of less than 1GB surpassed drives in the greater than 1GB range in 1987 in terms of unit shipments.

The shift from write-once to multifunction devices is much more pronounced for the less than 1GB class, however, causing shipments of these products to decline from their peak of 48,600 units in 1991 to zero units in 1996.

Of the 2 classes of write-once drives remaining in 1996, 97% of unit shipments and 98% of revenue will be from drives in the greater than 3GB category. These products entered the market in low volume in 1988. Their portion of total write-once units and revenue will climb steadily.

Rewritable and multifunction products surge after entry rewritable drives started shipping quantities in late 1988 from several suppliers and quickly grew in volume as they filled latent demand. In terms of revenue, rewritable drives overtook CD-ROM drives in 1989, will pass write once drives in 1991, and will achieve 1.7x their combined dollar volume in 1996.

Nearly all rewritable drives during the forecast period will be of capacities below 1GB.

The report provides separate forecasts for 5.2S-inch and 3.5-inch rewritable products and combines multifunction drives into these categories.

The smaller form factor drives entered the market in 1990 and are receiving a big boost with IBM’s recent announcement of a 3.5-inch rewritable drive for certain IBM desktop systems.

Unit shipments of 3.5-inch drives will surpass 5.25-inch drives in 1996, but will lag in revenue throughout the period.

Total rewritable/multifunction shipments will rise from 99,200 drives in 1990 to 848,000 drives in 1996, a compound growth rate of 43%. Revenue during that same period will grow from $224 million to $990 million, a rate of 28%.

All optical disk drives worldwide

This article is an abstract of news published on the former paper version of Computer Data Storage Newsletter on issue ≠43, published on August 1991.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter