True Challenge Facing Memory Industry With COVID-19 in China Will Surface in 3Q20

If demand continues to fall, NAND flash prices may be expected to take quick nosedive in 2H20.

This is a Press Release edited by StorageNewsletter.com on March 17, 2020 at 2:15 pmAccording to the DRAMeXchange research division of TrendForce, Inc., despite the apparent slowdown of the COVID-19 outbreak in China, the virus is now rapidly multiplying across the Middle East, Europe, and the United States.

Earlier, the World Health Organization declared the COVID-19 outbreak a pandemic, which poses dire, system-wide risks for the global economy. Similarly, the memory market may take a turn for the worse and go into a slump earlier than expected.

Regarding market demand, the pandemic’s rapid proliferation will severely impede economic and social activities and subsequently hinder consumer purchasing power. On the other hand, lowered electronic product shipments will bring about a corresponding drop in memory demand.

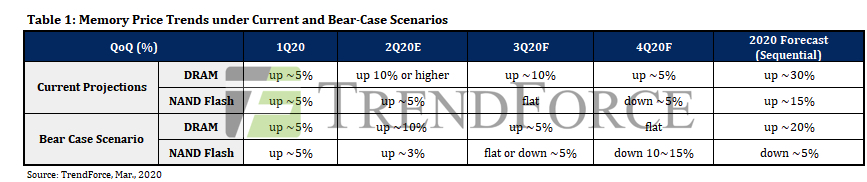

DRAM and NAND flash ASPs are able to maintain their growths in 1Q20 and 2Q20 primarily because of relatively low client inventory levels.

Provided that the current ASP uptrend continues, clients may have a strong incentive to raise their stock of memory products. Nevertheless, the true challenge facing the memory industry will surface in 3Q20, when sluggish consumer demand will encumber device manufacturers’ inventory reduction efforts, massively weakening client-side memory procurement and resulting in limited ASP growth. Worse yet, rising NAND flash prices may make a turnaround into a decline instead.

Note: Current Projections are based on data from the beginning of March, 2020. Bear Case Scenarios are newly added forecasts based on data from March 12, 2020.

As the global economy cools down, and consumer confidence dips, demand for electronic devices will continue to decrease

As the global economy cools down due to the pandemic, there are 2 implications facing the consumer electronics industry:

- The general public begins allocating relatively conservative amounts of its income to personal spending, in turn deferring the demand for consumer electronics and diminishing the average spending in the market.

- The pandemic results in higher logistics and human resource costs within the consumer electronics supply chain while lowering revenues, potentially triggering an industry-wide reorganization and reshuffle.

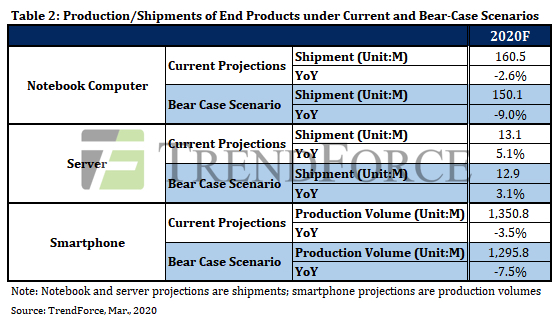

At the moment, the three types of electronic products with the highest impact on DRAM and NAND flash markets are notebook computers, servers, and smartphones. Out of these three applications, smartphone production will undergo the greatest magnitude of cutbacks. Although the recent sell-through performance has been quite remarkable since the Lunar New Year, the upward momentum is unlikely to last; actual smartphone production remains still in decline.

The rising demand for telework and distance learning has galvanized a corresponding rising demand for servers. With cloud service providers’ ongoing efforts at infrastructure build-out, the demand for servers has not been noticeably impacted by the pandemic. Most enterprise clients, on the other hand, have adopted a cautious approach to business operations and conservatized their CAPEX, potentially – and gradually – weakening future demand for enterprise servers.

Sluggish demand means limited growth for 2H20 memory prices, with NAND flash prices possibly decreasing

It was initially forecasted a probable constant growth for DRAM and NAND flash prices up to the end of the year, given that both products saw limited supply growth in 2020, at 13% and 32% Y/Y, respectively, in addition to the mostly low inventory levels maintained by DRAM and NAND flash clients. As structural changes start to take place on the demand side, memory purchasers will exhibit a weakened readiness to raise inventory levels from the end of 2Q20 onwards, in turn affecting the price trend of memory products in 2H20. In terms of DRAM, the considerable preexisting gap between supply and demand is expected to persist even if demand drops. Thus, 2H20 DRAM prices will, at worst, exhibit limited growth rather than a decline.

Unlike DRAM, there does not exist a similarly considerable shortage in the NAND flash market. As well, client-side demand has started showing hints of downturn for 2Q20. If demand continues to fall, NAND flash prices may be expected to take a quick nosedive in 2H20.

Note: Current Projections are based on data from the beginning of March, 2020. Bear Case Scenarios are newly added forecasts based on data from March 12, 2020.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter