History (1990): Optical Disk Drive Shipments Up 118% in 1989 Over 1988 – Freeman Report

With revenue increasing by 95%

By Jean Jacques Maleval | December 13, 2019 at 2:12 pm“Increased availability of drives and media and lower device prices are widening the acceptance of optical storage technology in all categories,” declared Robert B. Abraham and Raymond C. Freeman, Jr., authors of the 398-page Freeman Report: Optical storage Outlook (389 pages, $1,850), available from Freeman Associates (Santa Barbara, CA). “Total drive shipments for 1989 were up 118% over 1988 levels, and 1989 revenues outstripped 1988 by 95%.”

Unit shipments of CD-ROM and rewritable drives will rise dramatically through 1995.

Revenues from rewritable optical disk drives – the newest product class – will grow steadily as OEMs and system integrators employ these long-awaited products. Rewritable optical disk drives exhibit many of the same characteristics as magnetic HDDs but offer the added functionality of media removability.

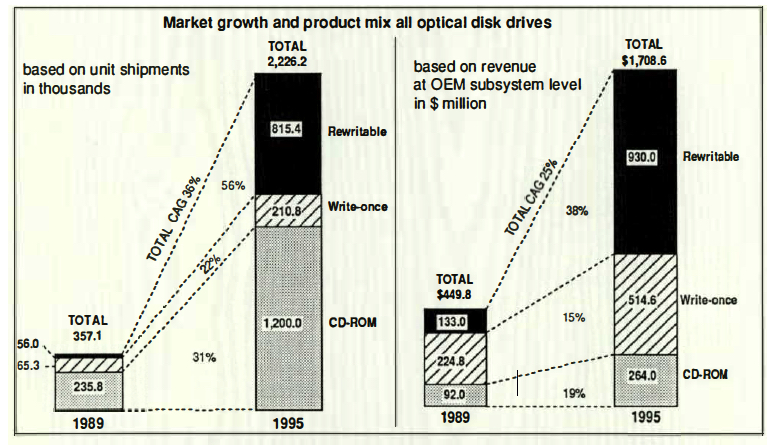

The WW market for all types of optical data disk drives will exceed $1.7 billion at OEM price levels in 1995, a 25% CAGR from the $449 million value of the 1989 market. Annual shipments of drives will exceed 2.2 million units in 1995. Projected unit shipments for 1995 total 1,200,000 CD-ROM drives (54% of total optical disk drives), 210,000 write-once units (9%), and 815,000 rewritable devices (37%).

The composite total of these units shipments represents a CAGR of 36% during the 6-year period from 1989 through 1995.

Revenue shares for 1995 are divided quite differently from unit shipments.

CD-ROM drives, at $264 million, will account for only 15% of total revenue stated at OEM levels.

Write-once devices will represent $514 million, or 30%, of total dollar volume, and rewritable products will achieve a 55% share of 1995 revenues at $930 million.

CD-ROM drives will be the predominant class through 1995 in terms of unit volumes.

Write-once drives will relinquish their lead in revenue to rewritable drives in 1991.

Rewritable revenues will dominate the optical market thereafter.

CD-ROM market pace quickening after several sluggish years, the market for CD-ROM drives for all data applications is growing rapidly. Declining hardware and software prices have broadened the appeal of CD-ROM technology.

Production of CD-ROM drives will continue to be dominated by Japanese manufacturers and Philips in The Netherlands (marketed by Laser Magnetic Storage International) because of their established positions in compact audio disc players.

The report predicts that no US manufacturer will enter the CD-ROM drive business. Involvement by U. companies in the CD-ROM market will continue to be extensive but will occur in electronic publishing, marketing, systems integration and disk replication, not in production of drives.

Write-once revenue lead to fade write-once versions have led the market for optical data disk drives since 1983 in terms of revenue gen but will finally relinquish that lead to rewritable devices in 1991. While 1989 unit shipments of write-once drives were only 26% of shipment levels of CD-ROM drives, write-once device revenues were 2.4X CD-ROM revenues, and are expected to be nearly 2 times in 1995 despite unit shipments that are only 17% of CD-ROM unit shipments.

Write-once drives with capacities of less than 1GB surpassed drives in the 1 to 3GB range in 1987 in terms of unit shipments and will progressively widen that edge through 1995 when they will outs hip the higher capacity drives by a factor of six times.

Because of the aggressive price competition expected in the less than 1GB class, however, they will earn only twice the revenue throughput the forecast period than their larger capacity cousins.

High capacity write-once drives exceeding 3GB entered the market in low volume production in 1988. Their portion of total write-once revenue will climb steadily to 26% by 1995.

Rewritable products surging after entry rewritable drives started shipping in small quantities in late 1988 from several suppliers and quickly grew in volume as they met the latent demand. Nearly all rewritable drives during this forecast period will be of capacities below 1GB.

Larger capacity drives will enter the market in 1991 as high-end system devices.

Rewritable drives overtook CD-ROM drives in terms of revenue in 1989 and will achieve three and one-half times the dollar volume of CD-ROM drives in 1995. Rewritable revenues will exceed those for write-once devices starting in 1991.

Report forecasts 7 market segments

The report analyzes the market and forecasts WW shipment volumes, revenues, and market shares for 7 classes of optical disk drives from 1988 through 1995. Pricing trends are analyzed, interaction with magnetic storage products is assessed, and future product directions are identified.

Specs are given for 83 models of read-only, write-once and rewritable drives produced worldwide by 33 manufacturers.

A total of 41 manufacturers are developing or producing optical disk drives. Characteristics of 105 offerings from 43 optical disk media makers are listed, along with one offering each of optical tape drive and media. Read-only disk preparation services provided by 27 companies are described, and lists of 22 suppliers of CD-ROM integration and software services and 55 electronic publishers are provided. Profiles of 64 companies active in the optical storage industry are included.

This article is an abstract of news published on the former paper version of Computer Data Storage Newsletter on issue ≠30, published on July 1990.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter