-0.8% Y/Y at $6.3 Billion in 2Q19 for WW Enterprise External OEM Storage Systems Market – IDC

Even AFA market down 0.7%

This is a Press Release edited by StorageNewsletter.com on September 6, 2019 at 2:39 pmAccording to the International Data Corporation‘s Worldwide Quarterly Enterprise Storage Systems Tracker, vendor revenue in the WW enterprise external OEM storage systems market decreased 0.8% Y/Y to $6.3 billion during 2Q19.

Total capacity shipments in the external storage systems market were up 5.2%Y/Y to 16.3EB during the quarter, while capacity shipments in the total market (including ODMs and server-based storage) declined 4.2% to 107.9EB. Revenue generated by the group of original design manufacturers (ODMs) selling directly to hyperscale datacenters declined 22.9% Y/Y in 2Q19 to $4.2 billion.

“Second quarter results trended similarly to the first quarter with ODMs continuing to decline against a difficult Y/Y comparison and internal (server-based) storage weighed down by a contraction in the server market,” said Sebastian Lagana, research manager, infrastructure platforms and technologies. “While the external OEM segment was pressured by contraction in AFAs, which has long been a growth driver for the segment, we did note end user investment in mid-range SAN platforms remained strong, with nearly all OEMs generating growth in that portion of the market.”

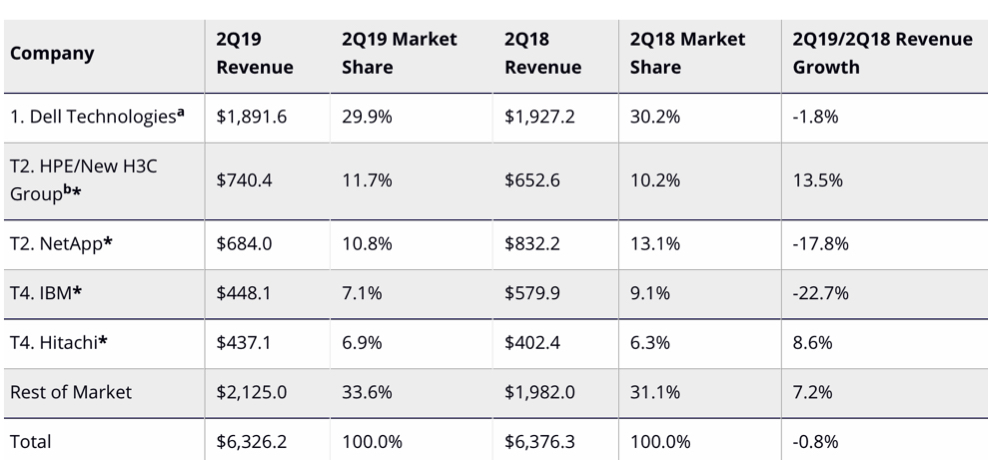

Enterprise External OEM Storage Systems Results, by Company

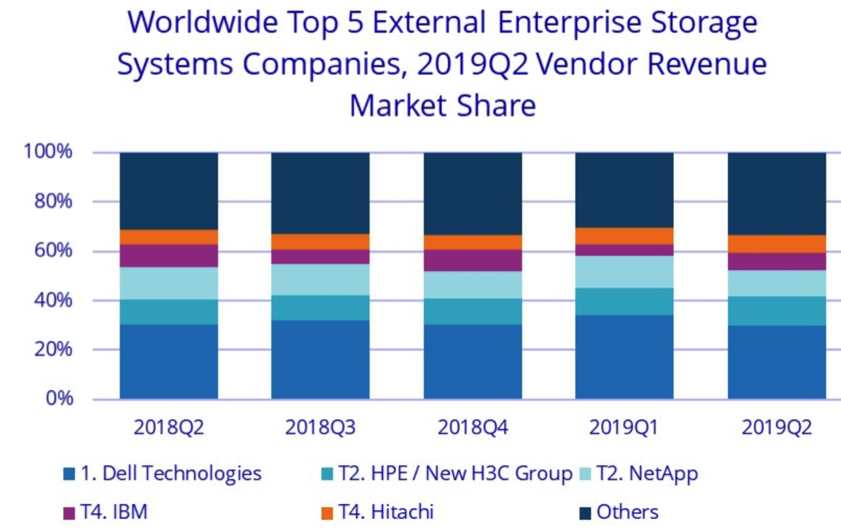

Dell Technologies was the largest enterprise external storage systems supplier during the quarter, accounting for 29.9% of WW revenue. HPE/New H3C Group and NetApp tied* for the second position with 11.7% and 10.8% of the market respectively. IBM and Hitachi tied* for the fourth position with 7.1% and 6.9% of global external storage market revenues.

Top 5, WW Enterprise External OEM Enterprise Storage Systems Market, 2Q19

(in $ million)

Notes:

* IDC declares a statistical tie in the WW enterprise storage systems market when there is a difference of 1% or less in the share of revenues or unit shipments among two or more vendors.

a – Dell Technologies represents the combined revenues for Dell and EMC.

b – Due to the existing joint venture between HPE and the New H3C Group, IDC will be reporting market share on a global level for HPE as HPE/New H3C Group starting from 2Q16.

Flash-Based Storage Systems Highlights

The total AFA market generated nearly $2.1 billion in revenue during the quarter, down 0.7% Y/H. The hybrid flash array market was worth nearly $2.7 billion in revenue, up 3.8% from 2Q18.

Regional External OEM Enterprise Storage System Highlights

On a geographic basis, Japan grew the fastest of any region, up 20.8% Y/Y. AsiaPac (excluding Japan) was up 7.9%. EMEA was down 3.2% while the USA was down 4.6% and Latin America declined 17.1%. Spending within China increased 10.9% Y/Y.

Taxonomy Notes

IDC defines an enterprise storage system as a set of storage elements, including controllers, cables, and (in some instances) HBAs, associated with three or more disks. A system may be located outside of or within a server cabinet and the average cost of the disk storage systems does not include infrastructure storage hardware (i.e. switches) and non-bundled storage software.

The information in this quantitative study is based on a branded view of the enterprise storage systems sale. Revenue associated with the products to the end user is attributed to the seller (brand) of the product, not the manufacturer. OEM sales are not included in this study.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter