Seagate: Fiscal 4Q19 Financial Results

Revenue down quarterly by 16% but more profitability

This is a Press Release edited by StorageNewsletter.com on August 5, 2019 at 2:56 pm| (in $ million) | 4Q18 | 4Q19 | FY18 | FY19 |

| Revenue | 2,835 | 2,371 | 11,184 | 10,390 |

| Growth | -16% | -7% | ||

| Net income (loss) | 461 | 983 | 1,182 | 2,012 |

4FQ19 Highlights

• Revenue of $2.37 billion

• GAAP diluted earnings per share (EPS) of $3.54; reflects a one-time deferred tax benefit of $702 million

• Non-GAAP diluted EPS of $0.86

• Cash flow from operations of $448 million and free cash flow of $297 million

• Repurchased 7.8 million shares for $350 million

• Declared cash dividend of $0.63 per share

FY19 Highlights

• Revenue of $10.4 billion

• GAAP diluted EPS of $7.06

• Non-GAAP diluted EPS of $4.82

• Cash flow from operations of $1.8 billion and free cash flow of $1.2 billion

• Returned $1.7 billion to shareholders through dividends and share repurchases

Seagate Technology plc reported financial results for its fiscal fourth quarter and fiscal year ended June 28, 2019.

“We continued to execute well in the June quarter in the midst of an uncertain global environment. We once again delivered on all of our financial expectations, while driving higher operating profit and earnings per share quarter-over-quarter, and demonstrating our ongoing focus on optimizing free cash flow,” said Dave Mosley, CEO. “As we enter our next fiscal year, global industry conditions have started to improve, particularly among cloud and hyperscale customers. Seagate is in a strong strategic position to address growing demand for mass storage. In March, we began shipping the industry’s highest capacity 16TB drives. Qualifications are progressing well and we remain on track to ramp production in order to meet future demand. We have also begun to qualify our dual-actuator technology with multiple customers, which doubles drive performance while maintaining the same capacity. Seagate’s strong technology pipeline continues to deliver efficient and cost-effective solutions for customers to manage ever-increasing amounts of data.“

In 4FQ19, the company recognized a one-time deferred tax benefit of $702 million resulting from a release of a valuation allowance related primarily to our U.S. deferred tax assets, which is reflected in GAAP net income, but excluded from non-GAAP net income. This was driven by improvements in the company’s profitability outlook in the U.S. including firm’s efforts to structurally and operationally align enterprise data solutions business with the rest of the company. This does not materially change future worldwide effective tax rate.

The company generated $448 million in cash flow from operations and $297 million in free cash flow during 4FQ19. For FY19, the company generated $1.8 billion in cash flow from operations and $1.2 billion in free cash flow. Balance sheet is healthy and during 4FQ19, it paid cash dividends of $174 million and repurchased 7.8 million ordinary shares for $350 million. For the full year, the company paid cash dividends of $713 million and repurchased 21 million ordinary shares for $963 million. Cash and cash equivalents totaled $2.2 billion at the end of the quarter. There were 269 million ordinary shares issued and outstanding as of the end of the quarter.

Quarterly cash dividend

The board of directors of the company declared a quarterly cash dividend of $0.63 per share, which will be payable on October 9, 2019 to shareholders of record as of the close of business on September 25, 2019.

The company is providing the following guidance for its 14-week for 1FQ20:

• Revenue of $2.55 billion, plus or minus 5%

• Non-GAAP diluted EPS of $0.90, plus or minus 5%

Comments

Guidance announced on the former quarter revenue of approximately $2.32 billion, plus or minus 5% for the most recent quarter, and being finally $2.37 billion, and sales of around $10.3 billion for FY19 or 8% less compared to FY18, and being and finally 10.39 billion, the lower figure since at least FY15.

Revenue for 4FQ19 was $2,371 million, down 16% Y/Y and 2.5% Q/Q with comparable net income, notably resulting from the backdrop of increasing geopolitical uncertainty and regulatory hurdles.

CEO Dave Mosley commented: "These broader macro conditions disrupted our customers buying patterns, causing trepidation among some of our enterprise and OEM partners. While prompting others to accelerate demand, including a few surveillance customers."

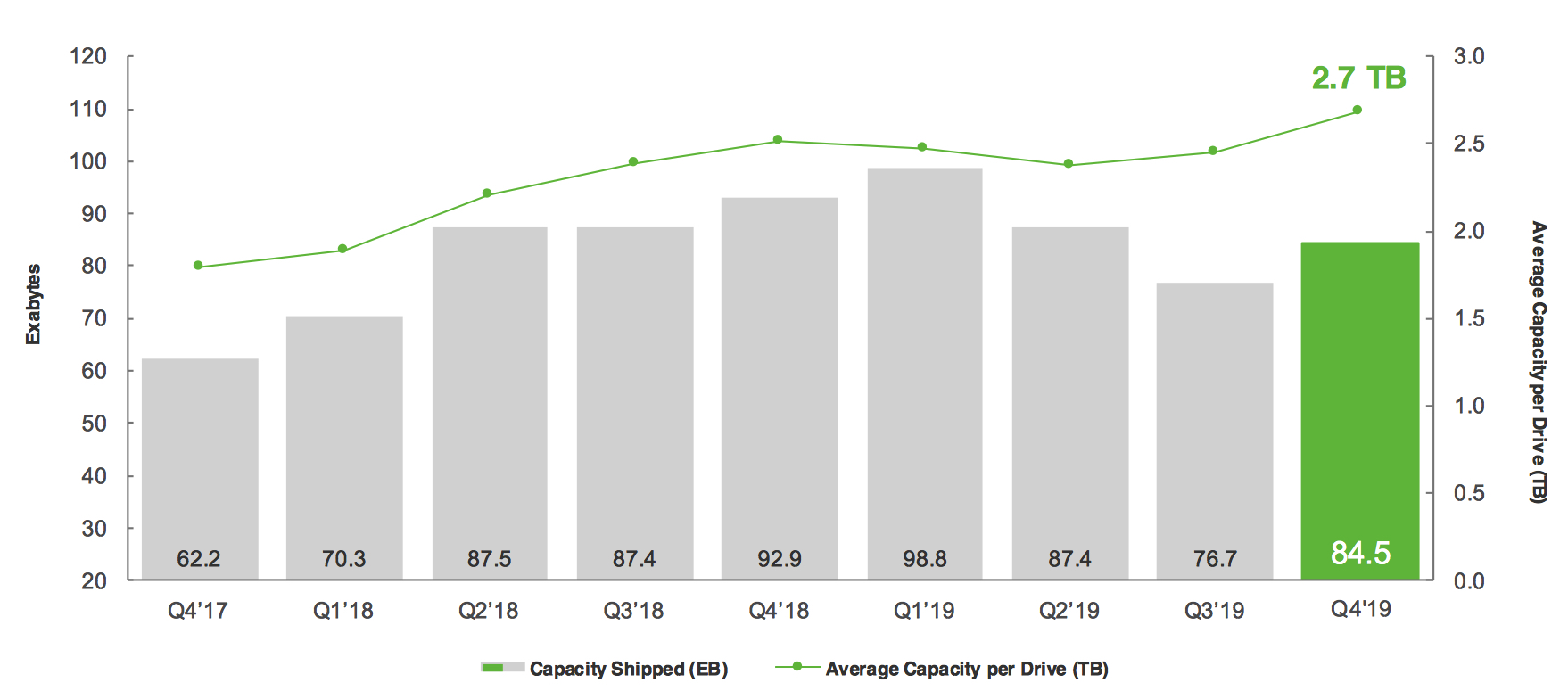

Total exabytes shipment were up 10% Q/Q to 84.5EB.

Revenue for the enterprise market, which includes nearline and mission critical HDDs represented 41% of total June quarter revenue, up from 39% in the March quarter, mainly due to stronger demand in nearline drives. Exabyte shipments into the enterprise market were up 15% Q/Q at 38EB. Nearline drives accounted for more than 90% of that total, with the average capacity per nearline drive at nearly 8TB. Revenue from 12TB and higher capacity drives now represents more than 50% of total nearline revenue, compared with 36% in the prior quarter. The firm shipped 33EB into the edge non-compute market during the June quarter, compared to 29EB in the prior period.

Seagate HDD Capacity Shipped and Average Capacity per Drive

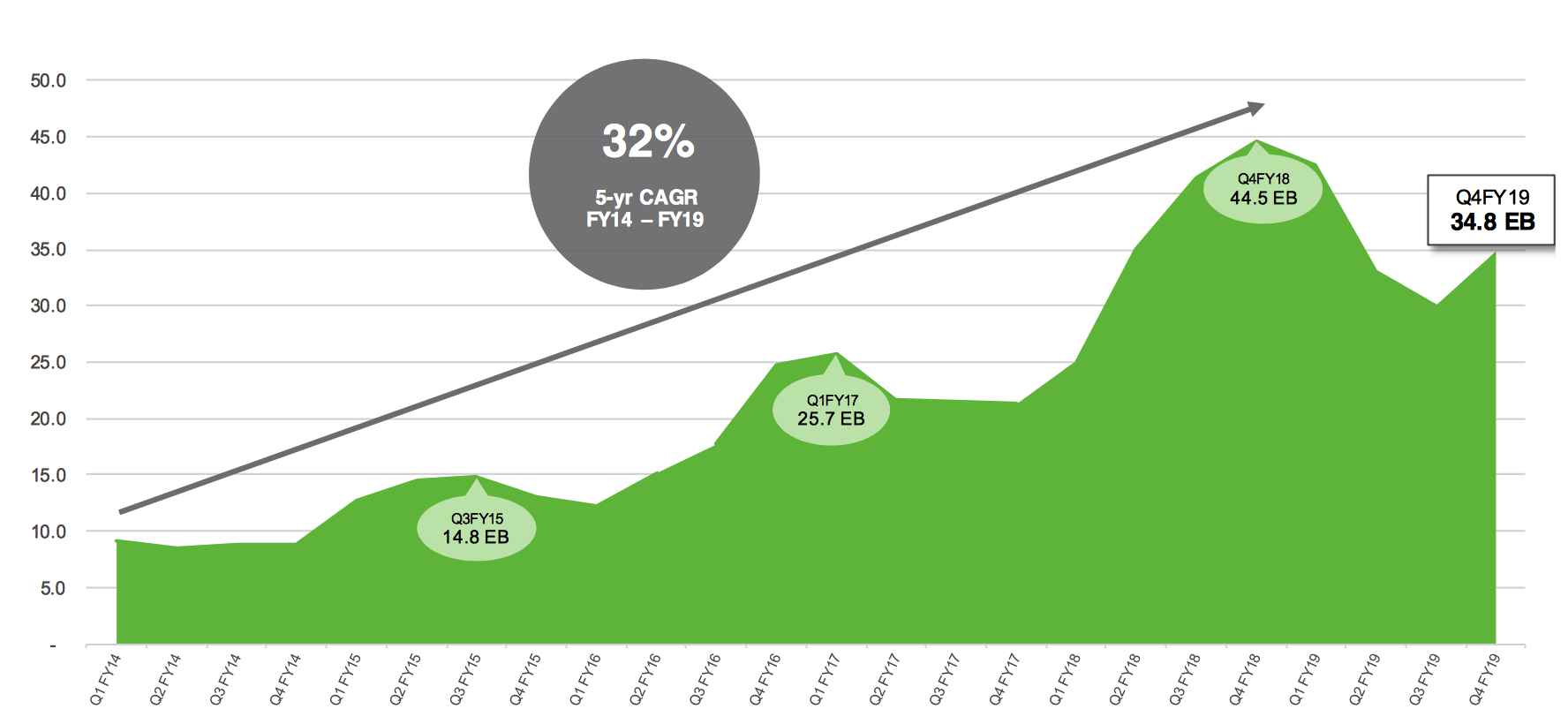

Seagate Nearline Demand Trend

Revenue from the edge compute market, including desktop and notebooks HDDs, contributed 18% of total sales, relative to 20% in the March quarter. Exabyte shipments down 6% to 14EB reflect typical seasonality.

Sales for the edge non-compute market, which include the surveillance, NAS, gaming, DVR and consumer application, increased to 34% of the total June quarter revenue, compared to 32% in the prior quarter.

Revenue for cloud system business was slightly down Q/Q.

As the firm shared last quarter, it began shipping 16TB in late March to deliver the highest capacity HDDs, and has already introduced products for enterprise and edge storage applications. Customer qualifications are progressing, and it remains on track to ramp high volume shipments later in CY19.

Total Q/Q exabyte shipments increased following the improving demand for nearline drives from cloud and hyperscale customers.

Innovative MACH.2 dual actuator technology is garnering interest. Customers have started to qualify these drives, which the firm expects to begin shipping later in 2019, starting around the 20TB capacity.

The company continues to be a poor player in SSD with revenue diminishing Q/Q from $189 million to $167 million or -12%, representing only 7% of global sales. The quarterly decline was driven by lower demand from enterprise SSD customers.

During the quarter, it received a cash payment of $1.35 billion from Toshiba Memory Holding Company for the early redemption of the outstanding preferred share Seagate held in the company. Just over the year ago, the HDD manufacturer made a $1.27 billion investment in TMC preferred shares.

As of the end of June, cash and cash equivalents were $2.2 billion, up $832 million from the prior quarter.

After being number two in number of HDD shipped, Seagate is now indisputably the leader of this segment, and probably in the future, now with 40% of the WW market share, WD being at 35% and Toshiba growing at 25%, with 2.5-inch HDDs continuing to decrease compared to 3.5-inch devices, according to Trendfocus.

Seagate expects exabyte shipments into the enterprise nearline market will be above the long-term CAGR of 35% to 40% in FY20. Additionally, it hopes to deliver revenue growth Y/Y.

Seagate hopes next fiscal year Capex to be near the midpoint of its target range of between 6% and 8% of revenue, to support plans to increase manufacturing exabyte capacity, to address growing demand.

HDD product mix trends

| (units in million) | 3FQ19 | 4FQ19 |

| EB enterprise mission critical | 2.9 | 2.9 |

| EB enterprise nearline | 30.0 | 34.8 |

| EB client non-compute consumer electronics | 17.6 | 22.7 |

| EB client non-compute consumer | 11.6 | 110.4 |

| EB client compute, desktop+notebook | 14.6 | 13.7 |

| Enterprise as % of total revenue | 39% | 41% |

| Client non-compute as % of total revenue | 32% | 34% |

| Client compute as % of total revenue | 20% | 18% |

Revenue by products in $ million

| 3FQ19 | 4FQ19 | Q/Q Growth | % of total revenue in 4FQ19 |

|

| HDDs | 2,124 | 2,204 | 4% | 93% |

| Enterprise data solutions, SSD and others |

189 | 167 | -12% | 7% |

Seagate's HDDs from 2FQ15 to 4FQ19

| Fiscal period | HDD ASP | Exabytes shipped |

Average GB/drive |

| 2Q15 | $61 | 61.3 | 1,077 |

| 3Q15 | $62 | 55.2 | 1,102 |

| 4Q15 | $60 | 52.0 | 1,148 |

| 1Q16 | $58 | 55.6 | 1,176 |

| 2Q16 | $59 | 60.6 | 1,320 |

| 3Q16 | $60 | 55.6 | 1,417 |

| 4Q16 | $67 | 61.7 | 1,674 |

| 1Q17 | $67 | 66.7 | 1,716 |

| 2Q17 | $66 | 68.2 | 1,709 |

| 3Q17 | $67 | 65.5 | 1,800 |

| 4Q17 | $64 | 62.2 | 1,800 |

| 1Q18 | $64 | 70.3 | 1,900 |

| 2Q18 | $68 | 87.5 | 2,200 |

| 3Q18 | $70.5 | 87.4 | 2,400 |

| 4Q18 |

$72 | 92.9 | 2,500 |

| 1Q19 | $70 | 98.8 | 2,500 |

| 2Q19 |

$68 | 87.4 | 2,400 |

| 3Q19 |

$72 | 76.7 | 2,400 |

| 4Q19 |

$79.7 |

84.5 |

2,700 |

Seagate vs. WD for 4FQ19

(revenue and net income in $ million, units in million)

| Seagate | WD | % in favor of WD |

|

| Revenue | 2,371 | 3,634 | 53% |

| Net income | 983 | (197) | NA |

| HDD shipped | 32.0 | 27.7 | -13% |

| Average GB/drive | 2,400 | 4,025 | 68% |

| Exabytes shipped | 76.7 | 111.5 | 45% |

| HDD ASP | $79.7 | $84.5 | 6% |

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter