Computex: Intel Optane and Other Next-Gen Memories Have Chance to Penetrate Into Market 2020 – DRAMeXchange

Datacenters and other special fields first to use them

This is a Press Release edited by StorageNewsletter.com on June 12, 2019 at 2:31 pmWhether DRAM or NAND Flash, current memory solutions are straining the physical limits of production processes, meaning it is becoming more and more difficult to keep on raising performance and lowering costs.

Therefore, there has been much discussion revolving around Intel Optane and other next-gen memories in recent years, in hopes of discovering new solutions while keeping modifications to the current platform to a minimum or even leaving it completely untouched. DRAMeXchange, a division of TrendForce, Inc. holds that next-gen memories and current solutions have their respective pros and cons, with prices forming the most critical areas of opportunity.

TrendForce states that Intel, Samsung and Micron and other memory manufacturers have already begun investments into next-gen memory solutions such as MRAM, PRAM and RRAM. Intel’s Optane, for example, uses 3DxPoint as the basis for designing server products. Since the release of DIMMs, which are completely compatible with servers on the market, identical slots allow motherboard design manufacturers to change server modules or Optane solutions at will to control the total cost of the completed product.

However, next-gen memory costs remain high due to the lack of up-scaling and normalization, leading vendors to target datacenters and other special applications, especially hyperscale datacenters with rather highly customized designs, which will allow new configurations to be planned for different memories.

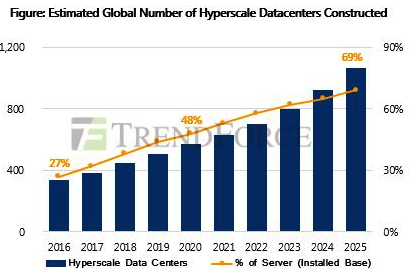

Due to AI reaching maturity and the pervasiveness of intelligent end devices in recent years, many application services have been integrated through the use of servers, especially those application services which require a huge amount of data for computation and training. Furthermore, server demand has been on the rise as virtual platform and cloud storage technologies gradually develop, bringing about the growth of hyperscale datacenters in the process. According to TrendForce’s investigations, the number of hyperscale datacenters constructed globally will reach a projected 1070 in 2025, registering a CAGR growth of 13.7% over the 2016-2025 period.

Memory Prices to Bounce in 2020,

Forming Area of Opportunity for Next-Gen Memories

From a market standpoint, DRAM and NAND are all facing oversupply, and current memory solution prices remain at a low point. The continual descent in DRAM prices is basically due to the drop in server and smartphone demand and the consequent quick-freeze in consumption and accumulating inventories. The NAND market, on the other hand, is prone to wars over market shares, and the shift from 2D NAND to varying degrees of 3D NAND caused supply bits to grow by large. In summary of the above, DRAM and NAND prices slid simultaneously and speedily in 2019, and NAND prices are nearing cash costs for suppliers.

Due to the cheapening trend of existing memory solutions, it may not be the best time for next-gen memories to make their entrance. Yet restocking momentum built through the gradual recovery in demand and price flexibility may occasion a rebound in server price in 2020, giving next-gen solutions a better chance to penetrate into the market. TrendForce posits that in the future years to come, there will be more adoption of next-gen memories in the market, allowing them to become alternative solutions.

Global Market Research Institute TrendForce was holding Compuforum 2019: The Big Future of Data Economics, at the Taipei International Convention Center (TICC), Taiwan, on May 31, 2019 during Computex.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter