Western Digital: Fiscal 3Q19 Financial Results

All main figures down including sales by 27% Y/Y and loss increasing

This is a Press Release edited by StorageNewsletter.com on May 1, 2019 at 2:19 pm| (in $ million) | 3Q18 | 3Q19 | 9 mo. 18 | 9 mo. 19 |

| Revenue | 5,013 | 3,674 | 15,530 | 12,935 |

| Growth | -27% | -17% | ||

| Net income (loss) | 61 | (581) | (81) | (557) |

Western Digital Corp. reported revenue of $3.7 billion for its third fiscal quarter ended March 29, 2019.

The operating loss was $394 million with a net loss of $581 million, or ($1.99) per share.

Excluding certain non-GAAP adjustments, the company achieved non-GAAP operating income of $186 million and non-GAAP net income of $49 million, or $0.17 per share. Both the GAAP and non-GAAP results include lower of cost or market inventory charges of approximately $110 million in cost of revenue, primarily related to certain flash memory products that contain DRAM components.

In the year-ago quarter, the company reported revenue of $5.0 billion, operating income of $914 million and net income of $61 million, or $0.20 per share. Non-GAAP operating income in the year-ago quarter was $1.3 billion and non-GAAP net income was $1.1 billion, or $3.63 per share.

The company generated $204 million in cash from operations during 3FQ19, ending with $3.8 billion of total cash, cash equivalents and available-for-sale securities. The company returned $146 million to shareholders through dividends. On February 14, 2019, the company declared a cash dividend of $0.50 per share of its common stock, which was paid to shareholders on April 15, 2019.

“Market conditions have generally been consistent with our expectations, and while the business environment remains soft, there are initial indications of improving trends,” said Steve Milligan, CEO. “Our expectation for the demand environment to further improve for both flash and HDD products for the balance of calendar 2019 is largely unchanged. We are executing well on enhancing our product portfolio, driving technology advancements, rightsizing our factory production levels and lowering our cost and expense structure, all of which position us to emerge stronger as market conditions improve.”

Comments

WDC continues to shrink drastically with sales down 27% Y/Y and 13% Q/Q at $3.7 billion in the middle of guidance range, and loss continuing and increasing.

That's the result of the fast diminishing HDD market and price reducing for SSDs as everyone knows. For the company, HDD sales were stable and SSD revenue were down 26% sequentially for the most recent quarter.

Nevertheless the firm saw incremental improvement in demand for capacity enterprise and client compute disk drives. Sales of these devices were a bit stronger than expected. Flash industry dynamics remain challenging but the company expects both flash and HDD demand to further improve for the balance of CY19.

WDC remains on track to launch 16TB and 18TB HAMR this calendar year.

In response to the current flash business conditions, the company is reducing its wafer starts at its flash-based memory manufacturing facilities operated through its partnership with Toshiba Memory Corporation. The temporary abnormal reduction in output has resulted in flash manufacturing underutilization charges which are expensed as incurred. The Kuala Lumpur manufacturing facility has largely ceased operations. The manufacturer is on track to achieve an overall reduction of 10% to 15% of its bit output in calendar year 2019.

WDC has also consolidated its head manufacturing operations from Thailand to the Philippines.

HDD and SSD revenue

| in $ million | 1Q18 | 1Q19 | 2Q19 |

3Q19 |

2Q/3Q19 growth |

| HDD |

2,610 | 2,494 | 2,060 | 2,064 | +0% |

| SSD |

2,571 | 2,534 | 2,173 | 1,610 | -26% |

Flash revenue was $1.6 billion with a sequential bit decline of 5% and a sequential ASP/GB decline of 23%. HDD revenue was $2.1 billion, similar to the prior quarter.

Revenue mix

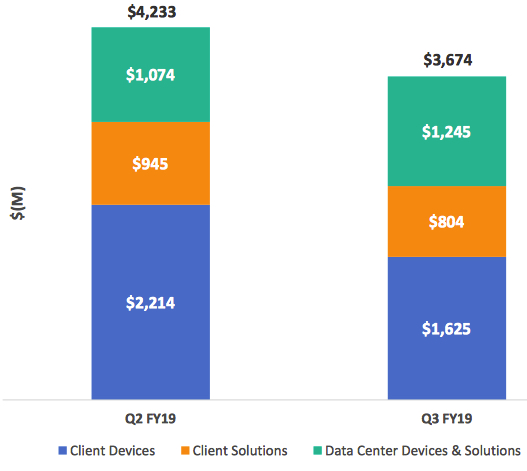

f

Data center devices and solutions (1)

• Demand for capacity enterprise drives better than expected

• Initial revenue shipments of enterprise NVMe SSD solutions and on track to accelerate ramp throughout CY19, debut of shipments of NVMe client SSDs based on 96-layer, 3D flash, BiCS4 technology supposed to become highest volume runner in terms of flash output, and to represent more than 25% of total shippable flash bits next quarter.

Client solutions (2)

• Continue to expand presence in external SSDs sold through retail

• Average capacity per unit for flash devices grew 44% Y/Y

Client devices (3)

Mobile embedded revenue declined due to weak handset demand

Notebook and desktop revenue decreased due to seasonality and flash price declines

(1) Data center devices and solutions: enterprise HDD and SSD, data center software, data center solutions and licensing and royalties

(2) Client solutions: branded HDD and flash, removables and licensing and royalties.

(3) Client devices: notebook and desktop, and consumer electronics HDD, client SSD, embedded, wafer sales and licensing and royalties.

| Exabyte metrics | 1FQ19 | 2FQ19 | 3FQ19 |

| Q/Q change in HDD exabytes sold (2) | -6% | -17% | 13% |

| Q/Q change in flash exabytes sold (2) | 28% | 5% | -5% |

| Q/Q change in total exabytes sold (2) | -3% | -15% | 11% |

| Flash metrics | 1FQ19 | 2FQ19 | 3FQ19 |

| Q/Q change in ASP/GB (2) | -16% | -18% | -23% |

(2) Excludes licensing, royalties, and non-memory products.

Guidance: Revenue between $3.6 and 3.8 billion, finally maybe quarterly slightly increasing and, based on recent industry announcements, WDC estimates flash industry supply growth to be slightly more than 30% in calendar 2019, somewhat lower from its prior forecast. Based in these expectations, WDC's global revenue will reach between $15.5 and $16.7 billion for FY19, an impressive decrease of 19% to 20% compared to FY18.

Volume and HDD Share for Fiscal Quarters

(units in million)

| Client compute units (5) |

Non-compute units (6) |

Data centers units (7) |

Total HDDs (8) |

Exabytes Shipped |

ASP (9) |

|

| 2Q18 |

21.1 | 14.4 | 6;8 | 42.3 |

NA | $63 |

| 3Q18 |

17.6 | 11.2 | 7.6 | 36.4 |

NA | $72 |

| 4Q18 |

17.8 | 13.7 | 7.5 | 39.0 |

NA | $70 |

| 1Q19 | 16.3 | 11.2 | 6.6 | 34.1 | 103.3 | $72 |

| 2Q19 |

14.0 | 11.3 | 5.1 | 30.2 |

75.9 |

$67 |

| 3Q19 |

12.9 |

9.3 |

5.6 |

27.8 |

97.5 |

$73 |

(6) Non-compute products consist of retail channel and consumer electronics HDDs.

(7) Data center products consist of enterprise HDDs (high-capacity and performance) and enterprise systems

(8) HDD unit volume excludes data storage systems and media

(9) HDD ASP is calculated by dividing HDD revenue by HDD units. Data storage systems are excluded from this calculation, as data storage systems ASP is measured on a per system basis rather than a per drive basis

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter