WW Enterprise Storage Systems Market Revenue Up 7.4% Y/Y in 4Q18 at $14.5 Billion – IDC

Lenovo +64%, Dell and NetApp +19%, IBM -6.5%

This is a Press Release edited by StorageNewsletter.com on March 8, 2019 at 2:23 pmAccording to the International Data Corporation‘s Worldwide Quarterly Enterprise Storage Systems Tracker, vendor revenue in the worldwide enterprise storage systems market increased 7.4% Y/Y to $14.5 billion during 4Q18.

Total capacity shipments were up 1.7% year over year to 92.5EB during the quarter.

Revenue generated by the group of original design manufacturers (ODMs) selling directly to hyperscale datacenters declined 1.5% year over year in 4Q18 to $2.7 billion. This represents 18.8% of total enterprise storage investments during the quarter. Sales of server-based storage increased 4.7% year over year to just under $4.1 billion in revenue. This represents 28.1% of total enterprise storage investments. The external storage systems market was worth roughly $7.7 billion during the quarter, up 12.5% from 4Q17.

“The fourth quarter results represent a slight shift from trends realized during the first three quarters of 2018, most notably the revenue decline for the ODM group of vendors as cloud providers slow their investment due to significant existing capacity,” said Sebastian Lagana, research manager, infrastructure platforms and technologies, IDC. “That considered, OEM vendors selling dedicated storage arrays are addressing demand from businesses investing in both on-premises and public cloud infrastructure. Ensuring storage systems support both a hybrid cloud model as well as increasingly data thirsty on-premises compute platforms is a high priority for enterprise customers.”

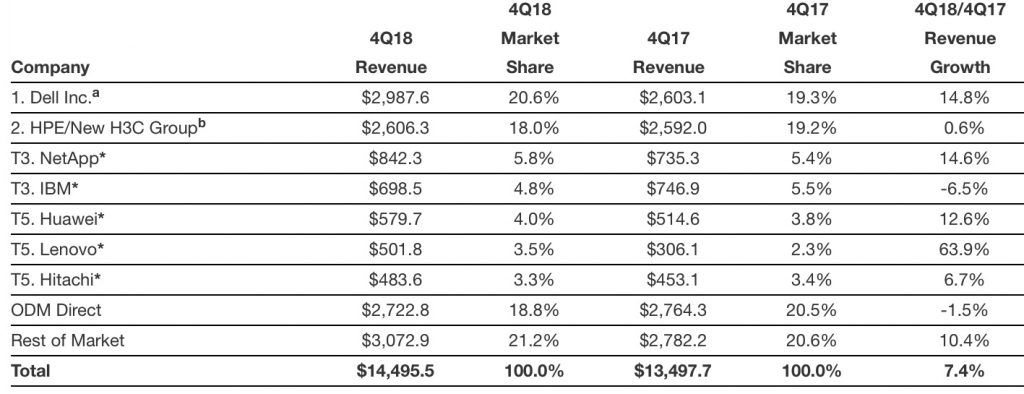

Total Enterprise Storage Systems Market Results by Company

Dell Inc. was the largest supplier for the quarter, accounting for 20.6% of total worldwide enterprise storage systems revenue and growing 14.8% Y/Y. HPE/New H3C Group was the second largest supplier with an 18.0% share of revenue on Y/Y growth of 0.6%. NetApp generated a 5.8% share of total revenue, statistically tying* for the number three spot during the quarter with IBM, which captured 4.8% market share. Huawei, Lenovo and Hitachi all statistically tied* for the number 5 position with shares of 4.0%, 3.5%, and 3.3% respectively. As a single group, storage systems sales by ODMs directly to hyperscale datacenter customers accounted for 18.8% of global spending during the quarter, down 1.5% against 4Q17.

Top 5 Companies, WW Total Enterprise Storage Systems Market, 4Q18

(revenue in $ million)

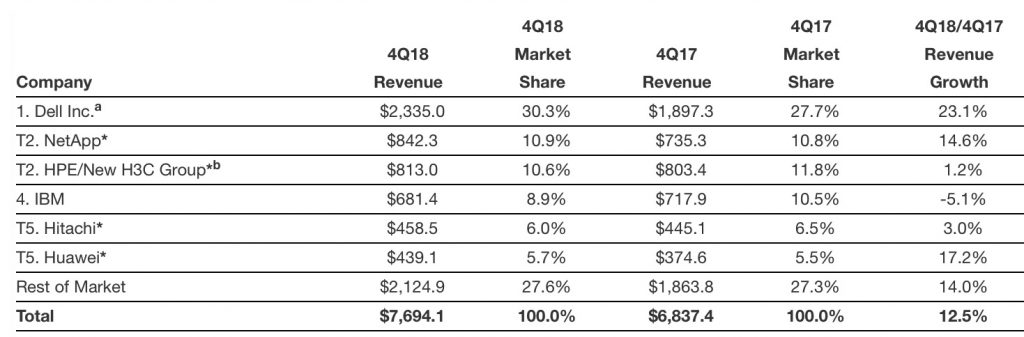

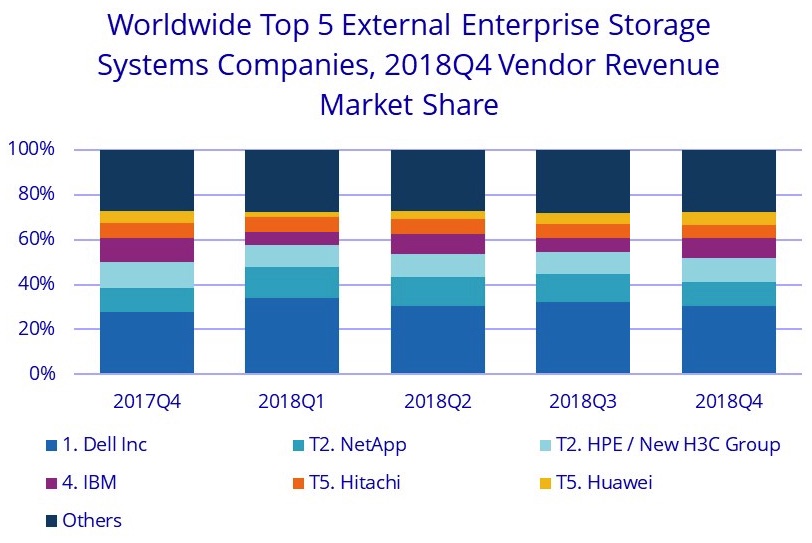

External Enterprise Storage Systems Results, by Company

Dell Inc. was the largest external enterprise storage systems supplier during the quarter, accounting for 30.3% of worldwide revenue. NetApp and HPE/New H3C Group finished statistically tied* for the number 2 position with a 10.9% and 10.6% share of revenue during the quarter respectively. IBM was the fourth largest with 8.9% share, while Hitachi and Huawei rounded out the top 5 in a statistical tie* with 6.0% and 5.7% market share.

Top 5 Companies, WW External Enterprise Storage Systems Market, 4FQ18

(revenue in $ million)

Notes:

* IDC declares a statistical tie in the worldwide enterprise storage systems market when there is a difference of one% or less in the share of revenues or unit shipments among two or more vendors.

a – Dell Inc. represents the combined revenues for Dell and EMC.

b – Due to the existing joint venture between HPE and the New H3C Group, IDC will be reporting market share on a global level for HPE as HPE/New H3C Group starting from 2Q16.

Flash-Based Storage Systems Highlights

The total AFA market generated just over $2.73 billion in revenue during the quarter, up 37.6% Y/Y. The hybrid flash array market was worth slightly more than $3.06 billion in revenue, up 13.4% from 4Q17.

Taxonomy Notes

IDC defines an enterprise storage system as a set of storage elements, including controllers, cables, and (in some instances) HBAs, associated with three or more disks. A system may be located outside of or within a server cabinet and the average cost of the disk storage systems does not include infrastructure storage hardware (i.e. switches) and non-bundled storage software. The information in this quantitative study is based on a branded view of the enterprise storage systems sale. Revenue associated with the products to the end user is attributed to the seller (brand) of the product, not the manufacturer. OEM sales are not included in this study.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter