EMEA Integrated Systems 3Q18 Market Revenue Up 20% Y/Y – IDC

Leading the pack: Dell EMC, Cisco/NetApp, HPE, Oracle, Nutanix

This is a Press Release edited by StorageNewsletter.com on January 21, 2019 at 2:22 pmThe integrated systems market in Europe, the Middle East, and Africa (EMEA) showed significant growth in 3Q18, reporting $873 million in user value, with Y/Y growth of 20.1%, according to the latest International Data Corporation‘s Quarterly Converged Systems Tracker.

Traditional converged systems, made up of certified reference systems and integrated infrastructure and integrated platforms, had a flat performance in this quarter, but still accounted for over 60% of total sales in EMEA. Meanwhile, hyperconverged systems have continued to show strong growth, reporting $348 million in 3Q18, with 70.9% Y/Y growth.

“Hyperconverged continues to see increased adoption in the EMEA market as companies make use of these systems’ simplicity, allowing IT managers to shift their focus higher up the stack,” said Eckhardt Fischer, senior research analyst, European infrastructure, IDC.

“Similar to last quarter, the growth in integrated systems has mainly been driven by a strong hyperconverged segment, while the more traditional certified reference systems and integrated infrastructure and integrated platforms segments saw a flat trend in U.S. dollar value terms, with little differentiation between segments,” said Silvia Cosso, research manager, European infrastructure, IDC. “Overall demand generated by the advantage of having pre-integrated, fine-tuned systems able to simplify the management and deployment of datacenter infrastructure, but their higher acquisition cost limits their deployment to specific use cases.”

Western Europe

In the EMEA region, Western Europe’s revenues account for about 78% of sales, of which the U.K., France, Germany, and the Nordic region still represent the lion’s share, around 75%. The Western European hyperconverged market is still being driven strongly by a handful of vendors that have found greater success by focusing on the larger 500 companies.

CEMA

Central and Eastern Europe, the Middle East, and Africa (CEMA) accounted for 22% share of EMEA market revenue in 3Q18, with Central and Eastern Europe (CEE) recording the strongest growth in EMEA. Sales of hyperconverged systems in CEMA exceeded both converged systems and integrated platforms sales for the first time and grew by 81% year-over-year.

“The majority of hyperconverged systems sales were driven by organizations from developing countries, mostly in the Middle East and Africa (MEA) region where the deployment of hyperconverged systems helps to address the lack of skilled IT resources as well as organizations’ growing need for scalability and agility,” said Jiri Helebrand, research manager, IDC CEMA.

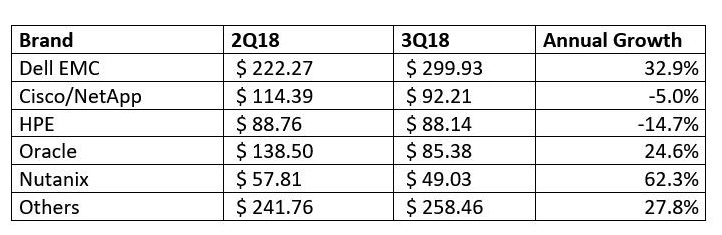

Top 5 Vendor Storage Systems Value Table

New Way of Purchasing Infrastructure and Applications

The following section provides definitions for the converged systems market. Given the overlap between converged systems and other infrastructure markets (including system infrastructure software), some definitions are taken directly from taxonomy documents covering enterprise storage systems, networking, servers, and system infrastructure software.

It should be noted that IDC’s segmentation of this market was updated for the March 2017 Converged Systems Tracker. None of the segmentation updates have changed the size of the overall market.

Specifically, the following changes have been made:

- A hyperconverged software vendor view has been added.

- Rack-scale hyperconverged solutions have been called out as a type of hyperconverged solution.

More details to these two changes are offered respectively within the ‘branded market view’ and ‘hyperconverged systems’ sections below.

Converged Systems

On a broad level, converged systems represent a competitive market based on elements from several of IDC’s existing taxonomies. Fundamentally, converged systems are differentiated from traditional hardware platforms and architectures in that they are designed to be deployed quickly using a modular building-block approach to rapidly scale up resources and workloads. Because these converged systems are pre-integrated and engineered to optimize internal east-west network traffic within the box, they are simpler to deploy and maintain while reducing processing and network overhead and latency. They enable the system to run its basic functions autonomously via programmed algorithms and present rich APIs that can be leveraged by higher-level systems and application management software or directly by end-user self-service portals.

IDC divides the converged systems market into three categories:

Integrated Platforms

- Certified Reference Systems and Integrated Infrastructure

Hyperconverged Systems

Integrated infrastructure and certified reference systems typically include the following datacenter resources:

- Servers

- Enterprise storage systems

- Networking equipment

- System infrastructure software (management software, virtualization software, multipathing software, etc.)

Integrated platforms include the items listed above plus some combination of applications, databases, and middleware that are shipped as a fully integrated part of the solution.

Hyperconverged systems are a new generation of converged systems that can virtualize some aspects of the resources listed above through virtualization or software-defined infrastructure. Specifically, hyperconverged systems leverage software-defined storage controller software (SDS-CS) to provide enterprise storage services through the same x86 server resources also used to run hypervisors and applications. These systems eliminate shared, networked storage systems, thus further converging storage and compute resources. SDS networking is expected to drive yet another level of convergence and flexibility within this market.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter