Silicon Motion: Fiscal 2Q18 Financial Results

SSD solutions sales increasing 35% Q/Q

This is a Press Release edited by StorageNewsletter.com on October 11, 2018 at 2:23 pm| (in $ million) | 2Q17 | 2Q18 | 6 mo. 17 | 6 mo. 18 |

| Revenue | 132.7 | 138.1 | 260.0 | 268.4 |

| Growth | 4% | 3% | ||

| Net income (loss) | 25.4 | 33.2 | 47.5 | 53.8 |

Business Highlights

• Embedded Storage sales increased approximately 7% Q/Q and accounted for about 85% of total sales. They comprise primarily eMMC and SSD controllers and data center and industrial SSD solutions.

• Client SSD controller sales increased about 5% Q/Q

• eMMC controller sales decreased about 5% Q/Q

• SSD solutions sales increased about 35% Q/Q

• Client SSD controller projects with NAND flash vendors increased over 50% Q/Q

Silicon Motion Technology Corporation announced its 2FQ18 financial results for the quarter ended June 30, 2018.

For the second quarter, net sales increased 6% sequentially to $138.1 million from $130.3 million in the first quarter 2018.

Net income (GAAP) increased to $30.7 million or $0.85 per diluted ADS (GAAP) from a net income (GAAP) of $23.1 million or $0.64 per diluted ADS (GAAP) in the first quarter 2018.

For the second quarter, net income (non-GAAP) increased to $33.2 million or $0.92 per diluted ADS (non-GAAP) from a net income (non-GAAP) of $25.6 million or $0.71 per diluted ADS (non-GAAP) in the first quarter 2018.

Second Quarter 2018 Review

“In the second quarter, our client SSD controller sales continued to grow sequentially as well as year-over-year. In addition, our pipeline of SSD controller projects with NAND flash makers increased over 50% sequentially in the quarter, which is indicative of our customers growing focus on SSDs and our role as their controller partner,” said Wallace Kou, president and CEO. “Separately, our SSD solutions grew strongly while our eMMC sales declined slightly.”

Returning Value to Shareholders

On October 24, 2017, the board of directors of the company declared a $1.20 per ADS annual dividend to be paid in quarterly installments of $0.30 per ADS. On May 23, 2018, we paid $10.8 million to shareholders as the third installment of our annual dividend.

On August 1, 2017, the company announced that its board of directors had authorized a 12 month program for the company to repurchase up to $200 million. In the second quarter, the company did not repurchase any of its ADS and this program has now expired.

Business Outlook

“As NAND prices continue to decline and SSD affordability and adoption are improving, we are now increasing our full-year SSD controller growth expectation to at least 30%, with strong third quarter sequential growth,” said Kou. “However, due to a one quarter delay of large SSD solutions sales to a hyperscaler customer, we are now expecting our third quarter net sales to be stable sequentially despite strong SSD controller growth with revenue growth expected to improve in the fourth quarter. We expect that our gross and operating margins will benefit from the more favorable sales mix.“

For the third quarter of 2018, management expects revenue between $136.0 million to $142.9 million (down 1.5% to up 3.5% sequentially).

For FY18, management reiterates revenue between $550 million to $576 million (+5% to +10% Y/Y)

Comments

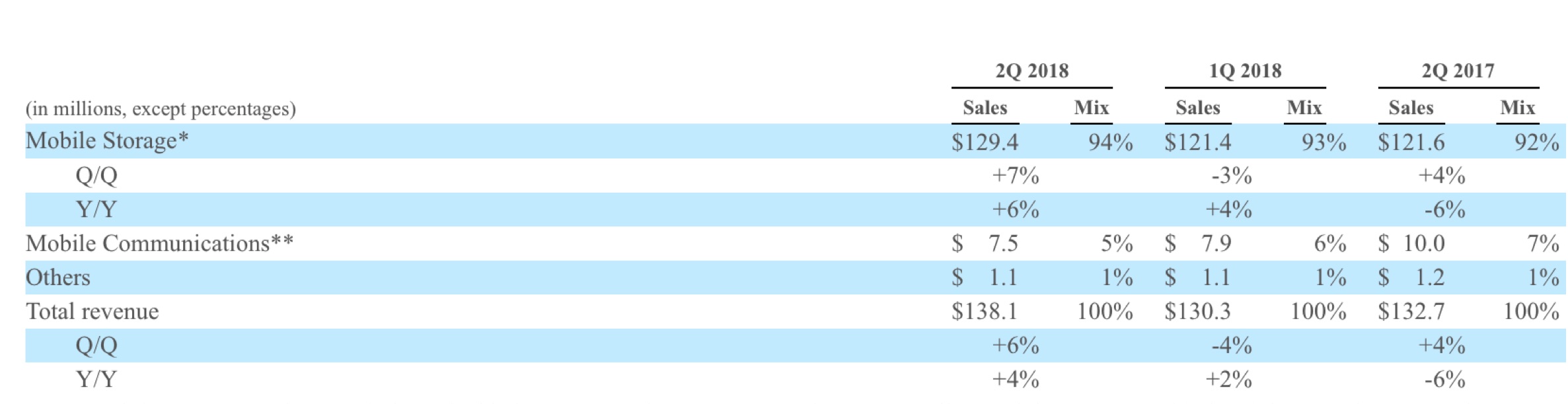

Revenue for the quarter at $138.1 million increases 6% Q/Q and 4% Y/Y.

Sales

Click enlarge

* Mobile Storage products include Embedded Storage products (eMMC and SSD controllers and data center and industrial SSD solutions) and Expandable Storage products (SD memory cards and USB flash drive controllers)

* Mobile Storage products include Embedded Storage products (eMMC and SSD controllers and data center and industrial SSD solutions) and Expandable Storage products (SD memory cards and USB flash drive controllers)

** Mobile Communications products include mobile TV SoCs

Total headcount at the end of 2Q18 increased to 1,273, which was 11 more than at the end of 1Q18.

Abstract of the earnings call transcript:

Wallace Kou, president and CEO:

"With rapid growing NAND supply and increasingly variable NAND prices, flash maker are more focused on SSD opportunity and raising their sales projections.

"As a result of flash partners' improved SSD growth outlook, we are increasing our full-year SSD controller sales growth to, at least, 30%, with sale accelerating in Q3.

"Additionally, during this quarter, we grew our pipeline of SSD controller projects at our 3D NAND flash partners Intel, Micron and WD by over 50% sequentially and more than double compared to last year. The majority of our pipeline of new SSD program are for PCIE, NVMe and now include those are used 64, 72 and 96-layer TLC and QLC 3D NAND with production running from this quarter all the way through 2020.

"NAND prices have fallen meaningfully since the start of this year. Dollar per gigabyte cost of NAND has been falling and will continue to fall rapidly with current high-volume 64 and 72-layer 3D NAND production. Scaling of 4 bits per cell QLC NAND and migration to 96-layer and upcoming higher layer count NAND. Since the NAND industry is very competitive with now seven suppliers, the benefit of increasing lower NAND costs is quickly passed to device OEM and consumers.

"We continue to believe that as NAND costs fall further, SSD demand will accelerate further.

"Now let me turn to our eMMC and UFS controllers. Sales declined slightly this quarter, we believe in line with our flash partners, all eMMC sales patterns in this quarter. China smartphone sales were weak and we believe our flash partner was more focused on SSD. Last quarter, we mentioned that embedded memory of Android smartphone have begun migrating from eMMC to UFS.

"We are encouraged by our growing sales of UFS controller to Micron in the second quarter. And we believe UFS controller sales could account for a meaningful proportion of our overall eMMC plus UFS controller sales in the second-half of this year and continue to grow strongly in 2019.

"Moving to our SSD solutions. Second quarter SSD solution sales increased sharply as our new project in Alibaba scales. In the third quarter, however, our Shannon Data Center SSD will be considerably weak.

"And as NAND prices continue falling from the introduction of increasingly low-cost NAND component over the next few years, we strongly believe that most, if not all of this HDD, will be replaced by SSDs."

Riyadh Lai, CFO:

"In Q2, sales of our SSD controllers grew approximately 5% sequentially.

"And for the full-year 2018, we believe our SSD controller sales will likely grow at least 30%, meaningfully higher than the 20% growth rate that we had previously communicated.

"In Q2, sales of our SSD solutions increased approximately 35% sequentially as Shannon SSD programs at Alibaba ramped and diversified FerriSSD sales continue to grow.

"In Q3, we expect our SSD solution sales to decline sharply as large orders are delayed one quarter and rebound in the fourth quarter. As a result of this delay, we no longer expect our SSD solutions to grow at least 20% for the full-year. Instead, our SSD solutions will at most grow 20% for the full-year. Sales of our memory card and USB flash drive controllers and other legacy products will decline as previously communicated for full-year 2018."

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter