WW Enterprise Storage Market Down 7% Y/Y in 4Q16 – IDC

33% for Dell, 10% for HPE, IBM and NetApp, 7% for Hitachi, all of them with sales decreasing

This is a Press Release edited by StorageNewsletter.com on March 7, 2017 at 2:57 pmTotal worldwide enterprise storage systems factory revenue was down 6.7% year over year while reaching $11.1 billion in 4Q16, according to the International Data Corporation‘s Worldwide Quarterly Enterprise Storage Systems Tracker.

Total capacity shipments were up 18.3% Y/Y to 52.4 exabytes during the quarter.

Revenue growth increased within the group of original design manufacturers (ODMs) that sell directly to hyperscale datacenters. This portion of the market was up 3.2% year over year to $1.2 billion.

Sales of server-based storage declined 7.8% during the quarter and accounted for $3.4 billion in revenue.

External storage systems remained the largest market segment, but the $6.4 billion in sales represented a Y/Y decline of 7.8%.

It should be noted that the size of the server-based storage market has been updated this quarter to reflect a change to IDC’s enterprise storage systems taxonomy. New methodology for sizing the server-based storage market is now more inclusive than in the past, thus increasing the size of the market in terms of value, systems shipped, and capacity consumed. Changes to the server-based storage market have been applied retroactively to ensure continuity with past quarters.

“2016 represented a year of considerable change for the enterprise storage systems market,” said Liz Conner, research manager, storage systems. “While the broader enterprise storage systems market has been impacted by headwinds, companies continue to increase their investments in several key areas, such as software-defined storage, cloud-based storage, all-flash storage systems, and converged systems. As a result, traditional enterprise storage vendors have aligned their portfolios to meet the shifting demands.”

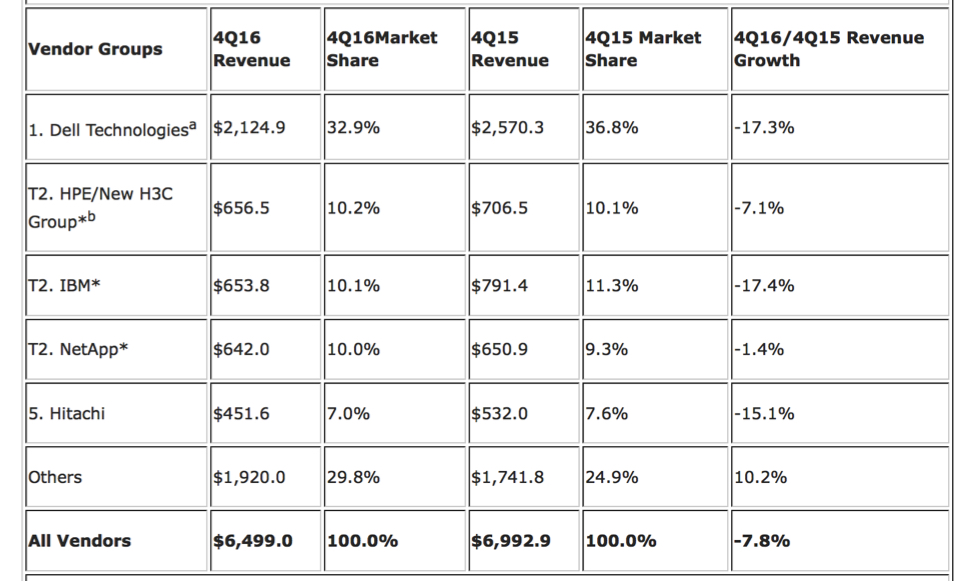

4Q16 External Enterprise Storage Systems Results, by Vendor Group

Dell Technologies was the largest external enterprise storage systems supplier during the quarter, accounting for 32.9% of worldwide revenues. HPE, IBM, and NetApp finished in a statistical tie* for the number 2 position with 10.2%, 10.1% and 10.0% of market share, respectively. HPE’s share and year-over-year growth rate includes revenues from the H3C joint venture in China that began in May of 2016; as a result, the reported HPE/New H3C Group combines storage revenue for both companies globally. Hitachi rounded out the top 5 with revenue share of 7.0%.

Top 5 Vendors, WW External Enterprise Storage Systems Market, 4Q16

(revenues are in $ million) Notes:

Notes:

* IDC declares a statistical tie in the worldwide enterprise storage systems market when there is less than 1% difference in the revenue share of two or more vendors.

a – Dell Technologies represents the combined revenues for Dell and EMC.

b – Due to the existing joint venture between HPE and the New H3C Group,

IDC will be reporting external market share on a global level for HPE as HPE/New H3C Group starting from 2Q16 and going forward.

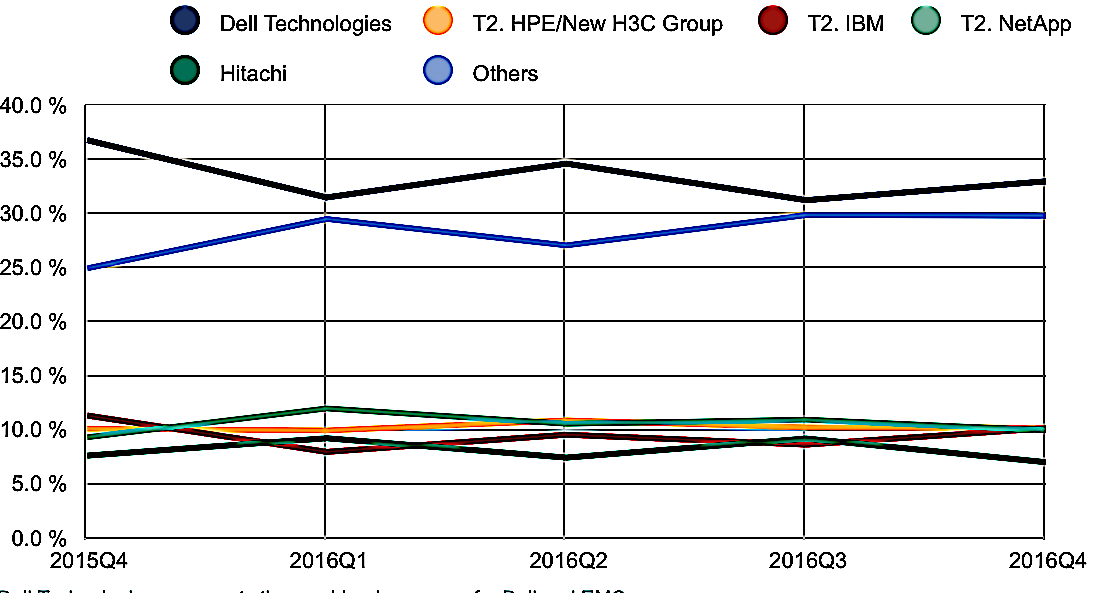

WW Total External Enterprise Storage Systems Market, Top 5 Vendors, 4Q15-4Q16

(shares based on revenue)

Source: IDC Worldwide Quarterly Enterprise Storage Systems Tracker, March 3, 2016

* Dell Technologies represents the combined revenues for Dell and EMC

* HPE/New H3C Group represents the combined revenues for HPE and New H3C Group

Source : IDC Worldwide Quarterly Enterprise Storage Systems Tracker Q4 2016

Flash-Based Storage Systems Highlights

The total all-flash array market generated almost $1.7 billion in revenue during the quarter, up 61.2% year over year. The hybrid flash array segment of the market continues to be a significant part of the overall market with $2.5 billion in revenue and 38.4% market share.

Taxonomy Notes

IDC defines an enterprise storage system (ESS) as a set of storage elements used to provide persistent data storage resources including power supplies, cooling, system enclosures, storage controllers, system cabling & external connections, and storage media (HDDs and/or flash). An enterprise storage system may be located outside of or within an application server. IDC excludes storage networking (e.g., FC switches) and non-bundled storage software when sizing the enterprise storage systems market.

The information in this quantitative study is based on a branded view of the disk storage systems sale. Revenue associated with the products to the end user is attributed to the seller (brand) of the product, not the manufacturer. Original equipment manufacturer (OEM) sales are not included in this study. In this study, Hitachi Data Systems (HDS) sales do not reflect their OEM sales to Sun Microsystems and Hewlett-Packard.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter