Samsung Controlled One-Third of NAND Flash Revenue in 3Q15 – DRAMeXchange

Global sales grew as prices showed steep decline.

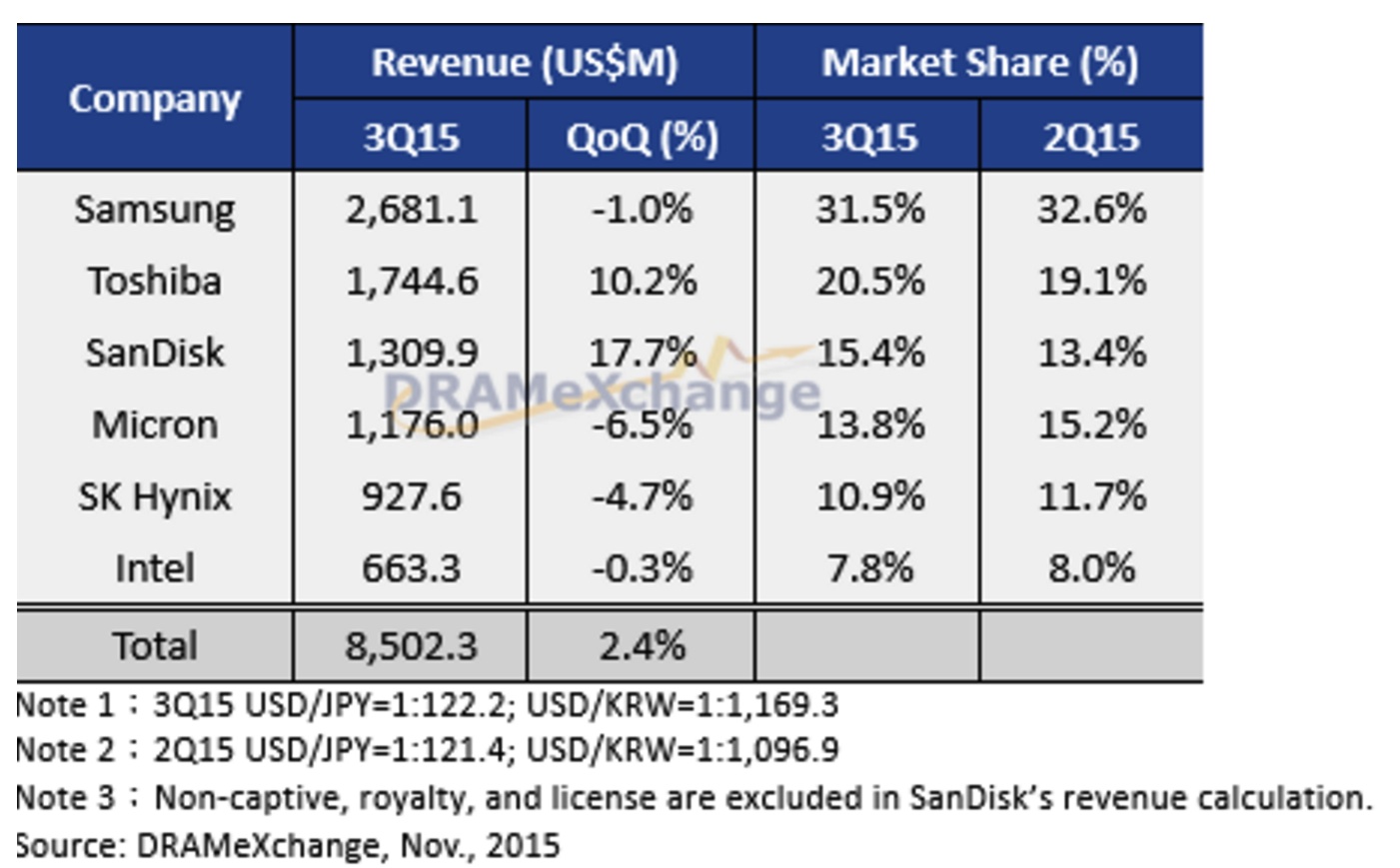

This is a Press Release edited by StorageNewsletter.com on December 1, 2015 at 2:52 pmThe latest report from DRAMeXchange, a division of TrendForce Corp., finds that NAND flash prices fell rapidly in the third quarter, resulting in a mere 2.4% quarterly increase in the global NAND flash revenue.

Sean Yang, assistant VP of DRAMeXchange, said demand was uncharacteristically weak in the third quarter and did not adhere to the seasonal pattern. NAND flash end demand was below expectations due to macroeconomic factor. This resulted in oversupply and sharp price decline in the NAND flash market, putting heavy pressures on NAND flash suppliers’ revenue growth and margins. DRAMeXchange expects the suppliers’ revenue situation to remain difficult during the fourth quarter because of the persisting oversupply problem.

3Q15 Revenue Ranking of Branded NAND Flash Players

Samsung

Both the OEM system product and the retail memory card markets saw a significant drop in their ASPs due to weak demand. This had a negative impact on Samsung’s NAND flash revenue in the third quarter. Compared with the second quarter, the supplier’s bit growth was up 15% but its revenue fell by 1% to $2.68 billion. The supplier’s operating margin also suffered a quarterly decrease. In terms of product strategy, Samsung’s 3D-NAND flash SSD and 16nm eMMC/eMCP product lines are ready. The supplier will be focusing on the promotion and sales of high-density SSD and eMMC/eMCP products to extend its lead over its competitors.

Toshiba

Toshiba’s NAND flash revenue grew by 10% in the third quarter because of several factors. First, Toshiba’s 15nm output increased and exceeded 50% of its total NAND flash production. At the same time, Toshiba’s strategic clients released their latest smartphones, and this in turn caused the shipments of the supplier’s 15nm TLC Mobile-NAND to pick up. Furthermore, server and PC vendors completed the sampling of Toshiba’s SSD products. As for Toshiba’s technology and production plans, Fab 2 equipment is being moved in and tested. Fab 2 is scheduled to do small batch runs of 3D-NAND flash in the first quarter of 2016. Fab 5, which mainly produces MLC and TLC chips, will also begin pilot production of 3D-NAND flash on an upgraded process during next year’s first quarter.

SanDisk

SanDisk saw a massive 49% quarterly increase in NAND flash sales bit growth in the third quarter, even though its ASP dropped 22%. The growth in bit sales was attributed to stock up demand of embedded products following the market release of new smartphones. The averaging selling cost fell by 24%, pushing the supplier’s NAND flash revenue up by 18% quarterly to $1.31 billion. The declining average selling cost also helped lifted the supplier’s gross margin from 39% in the second quarter to 42% in the third. The increase gross margin came after three consecutive quarters of falling figures. Almost 60% of SanDisk’s NAND flash production came from the 15nm process in third quarter. The supplier’s bit output is expected to increase by 40~45% in 2015. However, SanDisk’s annual bit output growth for 2016 will be slightly lower than the industry average because the supplier’s 3D-NAND development schedule will interfere with the production. Moreover, SanDisk will not increase its NAND flash capacity next year.

SK Hynix

In the third quarter, the ASP of NAND flash from SK Hynix fell 15%. This quarterly slide was due to weak demand and a rapid increase in the share of TLC chips in the supplier’s total output. Consequently, SK Hynix NAND flash revenue fell 4.7% to $927 million, while its bit supply volume jumped by 15%. Looking at the supplier’s product mix, SSD and embedded OEM products currently account for nearly 90% of total output. Demand has picked up since the supplier’s strategic clients released their new smartphones in the third quarter, and the supplier has also steadily expanded its shipments of TLC chips made on the 16nm process. TLC output is expected to account for 40% of the total production by the end of the year. SK Hynix has also managed to get a number of its TLC products verified by the module makers and will be ramping up TLC chip production for various applications (e.g. USB, SSD) in this fourth quarter.

Micron

Micron continued its product mix adjustment in its fiscal fourth quarter, which was from June to August. For that period, the supplier’s NAND flash revenue totaled $1.18 billion. The supplier’s bit supply volume and ASP for NAND flash fell by 6% and 1% respectively compared with the third fiscal quarter (from March to May). Micron’s storage business unit (SBU) also saw a slight quarterly decline in its operating margin. In addition to developing more enterprise and client-SSD product lines, Micron has gotten its TLC products verified by strategic partners in the memory module industry. Mass production and shipments have started in this year’s calendar fourth quarter (from October to December). The share of TLC products in Micron’s total output is expected to reach 20% in the first half of next year as well. Looking at technology, Micron is advancing rapidly to 3D-NAND flash manufacturing. The supplier is also on track in moving in equipment into its new fab in Singapore by next year. The share of 3D-NAND in Micron’s total production will expand quickly and may surpass 30% in the second half of 2016.

Intel

Intel’s third-quarter NAND flash revenue totaled $663 million, down 0.3% from the second the quarter. The slight decrease was attributed to strategic clients stocking up earlier in the second quarter and the rapidly declining ASP. In terms of NAND flash production strategy, Intel will strengthen its ties with its supply partner Micron and convert its chipset fab in Dalian, China, into a 3D-NAND fab. Intel, which sets its sights on future SSD opportunities in China, has therefore become the second NAND flash supplier to invest in a wafer fab in the country.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter