WW Cloud IT Infrastructure Market to Grow 24% at $33 Billion in 2015 – IDC

15% CAGR until 2019 and accounting for 46% of total spending on enterprise IT infrastructure

This is a Press Release edited by StorageNewsletter.com on October 12, 2015 at 3:01 pmAccording to the International Data Corporation‘s Worldwide Quarterly cloud IT Infrastructure Tracker, total spending on cloud IT infrastructure (server, storage, and Ethernet switch, excluding double counting between server and storage) will grow by 24.1% and will reach $32.6 billion in 2015.

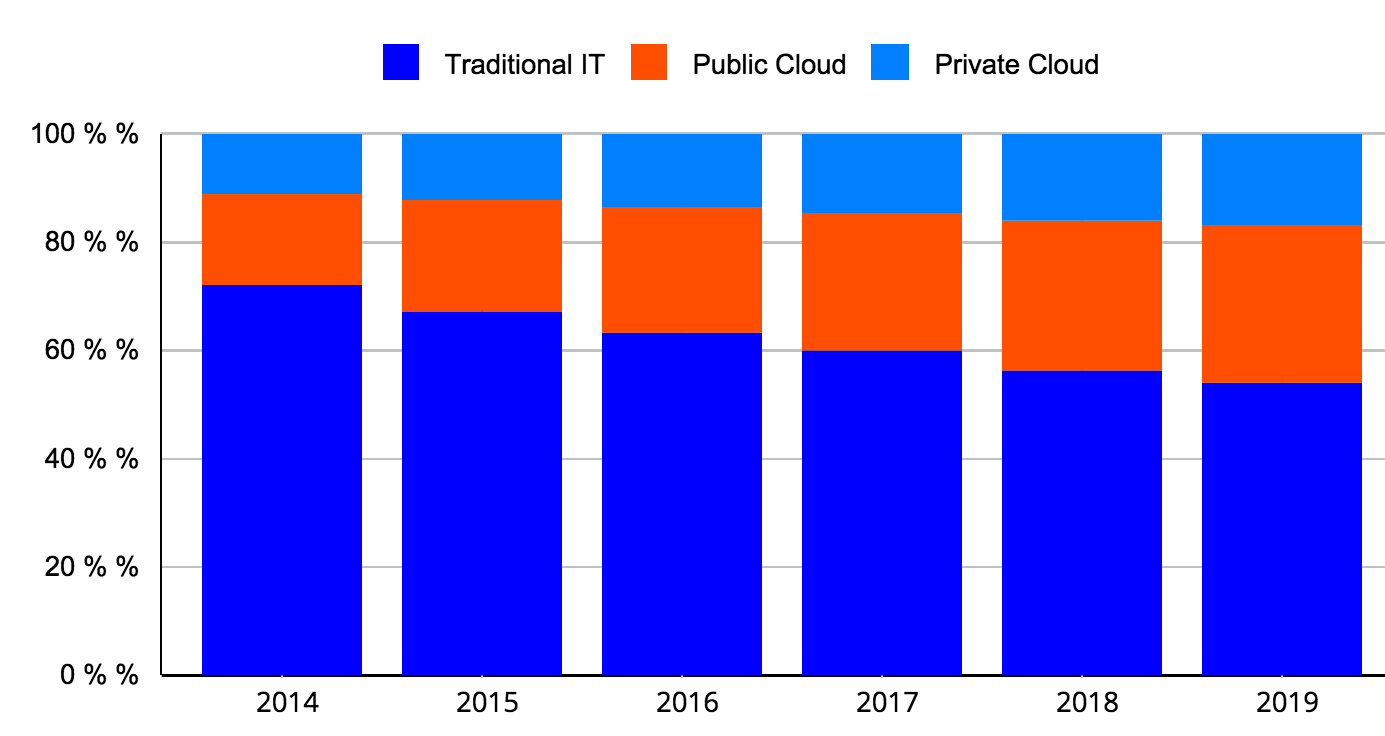

This amount will account for a third of the overall end user spending on enterprise IT infrastructure, up from 27.9% in 2014. In comparison, spending on IT infrastructure deployed in traditional, non-cloud, environments will decline by -1.6% in 2015, although at $66.8 billion will remain the largest segment of the market. Spending on private cloud IT infrastructure in 2015 will grow by 15.8% year over year to $12.1 billion, while spending on public cloud IT infrastructure will increase by 29.6% to $20.5 billion.

WW Cloud IT Infrastructure Market Forecast by Deployment Type 2014-2019

(shares based on value)

IDC expects that spending on cloud IT infrastructure in 2015 will grow across all regions except Central and Eastern Europe, which is disturbed by political and economic turmoil that is having a negative impact on IT spending.

For all three technologies – server, storage and Ethernet switch – growth in spending will exceed 20%, with spending on servers growing at the highest rate, 25.5%.

For the five-year forecast period, IDC expects that cloud IT infrastructure spending will grow at a CAGR of 15.1% and will reach $53.1 billion by 2019 accounting for 46% of the total spending on enterprise IT infrastructure. At the same time, spending on non-cloud IT infrastructure will decline at -1.7% CAGR.

Spending on public cloud IT infrastructure will grow at a higher rate than spending on private cloud IT infrastructure – at 16.3% vs 13.2% CAGR.

In 2019, IDC expects service providers will spend $33.6 billion on IT infrastructure for delivering public cloud services, while spending on private cloud IT infrastructure will reach $19.4 billion.

“Numerous IDC surveys indicate growing interest among enterprise customers to cloud deployments across multiple IT domains,” said Natalya Yezhkova, research director, storage systems. “End users often cite the agility of IT infrastructure and economic reasons as drivers for cloud adoption, but we also expect that the proliferation of next generation applications born and run in the cloud will fuel its further growth.“

Worldwide Quarterly cloud IT Infrastructure Tracker is designed to provide clients with a better understanding of what portion of the server, disk storage systems, and networking hardware markets are being deployed in cloud environments. This tracker will break out vendors’ revenue by the hardware technology market into public and private cloud environments for historical data and also provide a five-year forecast by the technology market.

Taxonomy Notes:

IDC defines cloud services more formally through a checklist of key attributes that an offering must manifest to end users of the service. Public cloud services are shared among unrelated enterprises and consumers; open to a largely unrestricted universe of potential users; and designed for a market, not a single enterprise. The public cloud market includes variety of services designed to extend or, in some cases, replace IT infrastructure deployed in corporate datacenters. It also includes content services delivered by a group of suppliers IDC calls Value Added Content Providers (VACP). Private cloud services are shared within a single enterprise or an extended enterprise with restrictions on access and level of resource dedication and defined/controlled by the enterprise (and beyond the control available in public cloud offerings); can be onsite or offsite; and can be managed by a third-party or in-house staff. In private cloud that is managed by in-house staff, ‘vendors (cloud service providers)’ are equivalent to the IT departments/shared service departments within enterprises/groups. In this utilization model, where standardized services are jointly used within the enterprise/group, business departments, offices, and employees are the ‘service users.’

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter