3Q14 WW Personal and Entry Level Storage Market Up by 4.8% Y/Y – IDC

19 million units shipped

This is a Press Release edited by StorageNewsletter.com on November 18, 2014 at 2:36 pmThe worldwide personal and entry-level storage (PELS) market was up by 4.8% year over year with almost 19 million units shipped in 3Q14, according to the International Data Corporation‘s Worldwide Personal and Entry Level Storage Tracker.

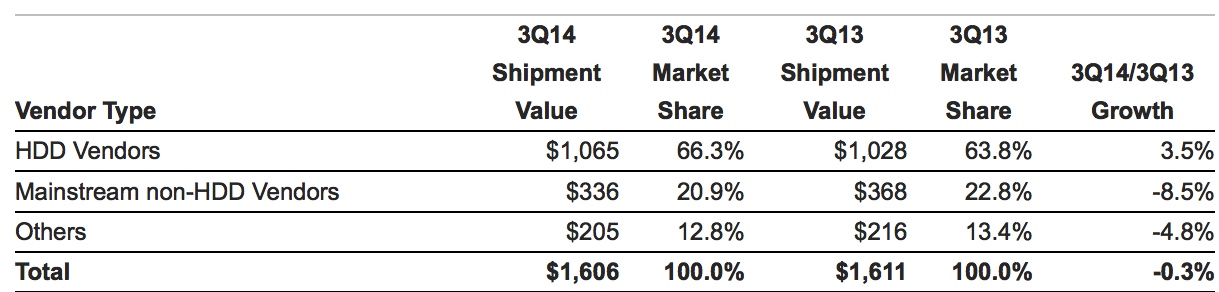

Shipment values declined -0.3% year over year to $1.6 billion.

“The personal and entry-level storage market showed strong shipment growth in the third quarter of 2014 with 18.8 million units shipped,” said Jingwen Li, research analyst, storage systems. “Both the personal and entry-level portion of the market contributed to this growth. The personal storage segment saw good growth in the higher capacity portable devices as well as personal cloud devices. With the former, consumers are looking for ways to expand their storage and backup options beyond their laptops, while the latter, along with mobile devices, address the storage and file sharing needs of an entire household. The entry-level segment saw strong growth in higher bay products (6-12 bays) as vendors introduce higher capacity offerings with more enterprise features at a more SMB-friendly cost.”

HDD vendors continued to increase their share in PELS units shipped, gaining 1.5%%age points Y/Y to grow to 78.7% market share. Although the entry-level storage market continued to be dominated by the mainstream non-HDD vendors, with 50.6% unit shipment market share, their market share continued to shrink by 14.5 points year over year.

WW Personal and Entry-Level Storage Shipment Value

(in $ million)

(Source: IDC Worldwide Quarterly Personal and Entry Level Storage Tracker, November 2014)

Market Highlights

- The entry-level storage market continued to experience significant growth in unit shipments this quarter, up by 15.1% Y/Y, based primarily on the 4-bay market. The entry-level market continued to see strong growth in the higher bay devices (6, 8, and 12 bays), which saw units shipped grow by 35.7% Y/Y.

- In 3Q14 the personal storage market saw growth for dual-bay products, where unit shipments were up by 7.1% Y/Y. Single-bay personal storage devices continued to remain the most popular choice, representing 97.5% of the personal storage units shipped in 3Q14.

- Personal storage represents 98.9% of the PELS unit shipped and 87.2% of the shipment value in 3Q14.

Technology Highlights

- Form Factor – The 3.5″ form factor experienced a decline of -7.1% Y/Y in units shipped, while the 2.5″ form factor saw units shipped up 8% Y/Y. The more portable 2.5″ form factor continued to encroach into the market space of the 3.5″ form factor, with 3.5″ losing 2.4%%age points of unit market share Y/Y in 3Q14.

- Capacity Range – End users continue to migrate to higher capacity points to meet their storage needs. In the 3.5″ personal storage market, 2TB devices represented 41.6% of unit shipments in the quarter. For the 2.5″ personal storage market, 1TB devices captured 60.7% market share. For the entry-level market, capacity ranges are more varied due to multiple bays and vendors’ ability to partially populate devices. However, 4TB devices hold the most market share with 23.4% of units shipped.

- Interface – USB continued to be the interface of choice for the PELS market. Its units shipped were up by 4.7% Y/Y this quarter. Ethernet remained the interface of choice for the entry-level market, capturing 94.8% of market share. Thunderbolt continued to ramp up, posting a Y/Y shipment growth rate of 7.3%, albeit off a very small base.

Notes:

- The PELS market includes storage products and solutions with a single bay through twelve bay configurations that are manufactured and marketed for individuals, small offices/home offices, and small businesses.

- IDC defines personal storage as having 1-2 bays and Entry-Level Storage as having 3-12 bays.

- IDC defines an HDD vendor as a vendor who manufactures their own HDD drive, in addition to branded external storage.

- IDC defines a mainstream non-HDD vendor as a major PELS vendor who does not manufacture its own HDD drives.

- Data for the PELS market is reported for calendar periods.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter