WW Disk Storage Revenue Falling at Rates Not Seen Since 2009 – IDC

-7% Y/Y to $5.6 billion in 1Q14, -17% from 4Q13

This is a Press Release edited by StorageNewsletter.com on June 9, 2014 at 3:20 pmWorldwide external disk storage systems factory revenues fell -5.2% year over year to $5.6 billion during the first quarter of 2014 (1Q14), according to the International Data Corporation‘s Worldwide Quarterly Disk Storage Systems Tracker.

For the quarter, the total (internal plus external) disk storage systems market generated $7.3 billion in revenue, representing a decrease of -6.9% from the prior year’s first quarter and a sequential decline of -17% compared to the seasonally stronger 4Q13.

Total disk storage systems capacity shipped was 9.9EB, growing just 19.9% year over year.

“The poor results of the first quarter were driven by several factors, the most important of which was a -25% decline in high-end storage spending,” said Eric Sheppard, research director, IDC storage. “Other important contributors to the market decline include the mainstream adoption of storage optimization technologies, a general trend towards keeping systems longer, economic uncertainty, and the ability of customers to address capacity needs on a micro and short-term basis through public cloud offerings.“

1Q14 External Disk Storage Systems Results

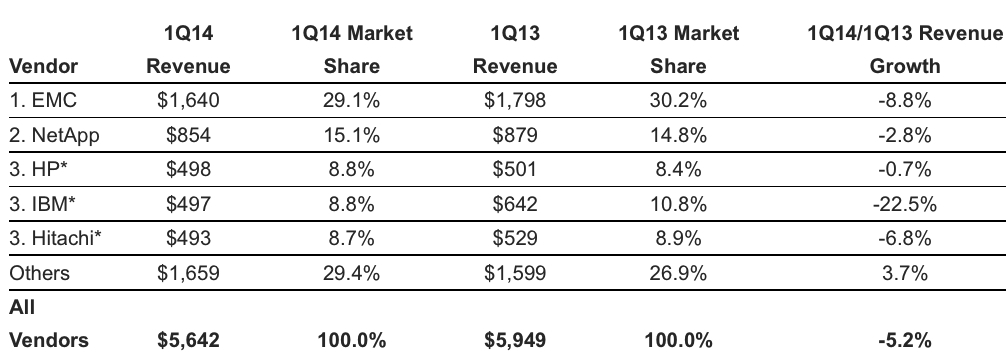

EMC was the largest supplier, but experienced a year-over-year share loss during the quarter. The company captured 29.1% of the external disk storage revenue during the quarter, which was down from 30.2% the year prior. NetApp was the second largest supplier in the market with 15.1% share of external revenue (up from 14.8% in 1Q13). HP, IBM, and Hitachi finished the quarter in a statistical tie* for the third position with shares of 8.8%, 8.8% and 8.7% respectively. Dell was the sixth largest supplier of external storage, generating 7.3% of the revenue during the quarter.

Open Networked Disk Storage Systems Highlights

The total open networked disk storage market (NAS combined with non-mainframe SAN) fell -3.9% year over year to $4.9 billion in revenue. EMC maintained its leadership in the total open networked storage market with 31.5% revenue share, but lost share compared to the 33.4% the company generated in 1Q13. NetApp was the second largest supplier with 17.3% share, followed by HP (8.9%), IBM (8.6%), and Hitachi (8.3%), all of whom tied* for third place.

WW External Disk Storage Systems Market, 1Q14

(in $ million)

(Source: IDC Worldwide Quarterly Disk Storage Systems Tracker, June 5, 2014)

1Q14 Total Disk Storage Systems Market Results

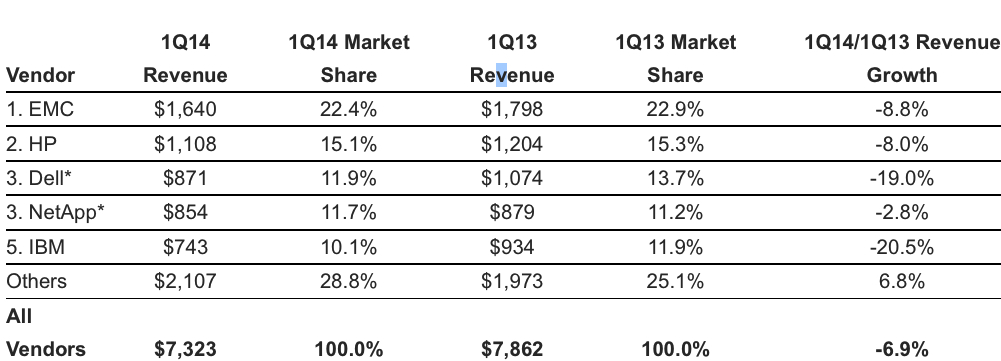

In the total worldwide disk storage systems market, EMC finished in the top position followed by HP with market shares of 22.4% and 15.1% respectively.

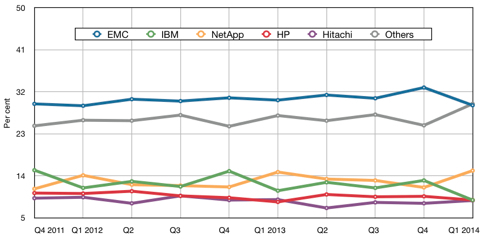

WW External Disk Storage Systems Market, From 4Q11 to 1Q14

(based on revenue)

(Source: IDC Worldwide Quarterly Disk Storage Systems Tracker, June 5, 2014)

WW Total Disk Storage Systems Market, 1Q14

(in $ million)

(Source: IDC Worldwide Quarterly Disk Storage Systems Tracker, June 5, 2014)

* Note: IDC declares a statistical tie in the worldwide disk storage systems market when there is less than 1% difference in the revenue share of two or more vendors.

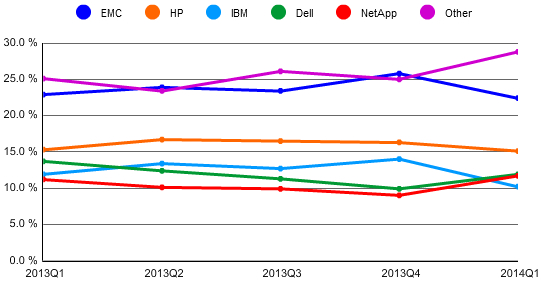

WW Total Disk Storage Systems Market From 1Q13 to 1Q14

(based on revenue)

(Source: IDC Worldwide Quarterly Disk Storage Systems Tracker, June 5, 2014)

Taxonomy Notes:

- IDC defines a Disk Storage System as a set of storage elements, including controllers, cables, and (in some instances) HBAs, associated with three or more disks. A system may be located outside of or within a server cabinet and the average cost of the disk storage systems does not include infrastructure storage hardware (i.e. switches) and non-bundled storage software.

- The information in this quantitative study is based on a branded view of the disk storage systems sale. Revenue associated with the products to the end user is attributed to the seller (brand) of the product, not the manufacturer. OEM sales are not included in this study. In this study, HDS sales do not reflect their OEM sales to Sun Microsystems and Hewlett-Packard.

- Worldwide Disk Storage Systems Quarterly Tracker is a quantitative tool for analyzing the global disk storage market on a quarterly basis. The tracker includes quarterly shipments and revenues (both customer and factory), terabytes, $/gigabyte, gigabyte/Unit, and average selling value. Each criteria can be segmented by location, installation base, OS, vendor, family, model, and region.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter