Imation: Fiscal 4Q13 Financial Results

For first time under $1 billion in annual revenue

This is a Press Release edited by StorageNewsletter.com on February 12, 2014 at 3:10 pm| (in $ million) | 4Q12 | 4Q13 | FY12 | FY13 |

| Revenue | 266.8 | 232.8 | 1,007 | 860.8 |

| Growth | -13% | -15% | ||

| Net income (loss) | (310.2) | 16.7 | (340.7) | (44.4) |

Imation Corp. released financial results for its 2013 fourth quarter and year ended December 31, 2013.

The company also announced that it has divested its XtremeMac business and benefited from certain special items as it continues to execute on its strategic transformation.

Q4 Overview, Including Special Items

For the fourth quarter of 2013, Imation reported net revenue of $232.8 million, down 12.7% from Q4 2012, income from continuing operations of $21.1 million, diluted earnings per share from continuing operations of $0.47 and a cash balance of $132.6 million.

The quarterly results were favorably impacted by $9.5 million of net benefit from special items, primarily a $9.8 million gain on the sale of land at a previously closed facility for which the company received proceeds of approximately $10.0 million. Excluding these items, Q4 2013 income from continuing operations would have been $11.6 million, and diluted earnings per share from continuing operations would have been $0.25. EBITDA for the fourth quarter totaled $26.5 million. In addition, Q4 operating results benefited from an accrual reversal of $9.5 million associated with European copyright levies as a result of a favorable court ruling in France.

For the full year 2013, revenue was $860.8 million, down 14.5% from 2012, and loss from continuing operations was $20.1 million, or $0.60 diluted loss per share. Special charges for the full year were $11.5 million. Excluding these special charges, 2013 loss from continuing operations would have been $8.6 million, and diluted loss per share from continuing operations would have been $0.37. EBITDA for the year totaled $3.6 million. In addition, operating results for the year benefited from accrual reversals of $23.1 million associated with European copyright levies as a result of favorable court rulings in France in Q4 and Italy in Q2.

Imation’s CEO Mark Lucas commented: “We are pleased with our fourth quarter results, which benefited from lower than anticipated revenue declines in our legacy business, solid working capital and cost management, and several one-time gains. While this is encouraging, we have not reached an inflection point in our transformation as our growth products have not yet offset secular revenue declines in our legacy business. We ended 2013 with some of our lowest inventories ever and $132.6 million in cash, which provides us with the financial strength to execute our strategic transformation.”

Sale of Non-Core Business

In the company’s third quarter 2013 release, Imation announced it had signed a letter of intent to sell its XtremeMac consumer electronics business. On January 31, 2014, Imation completed the sale of this business as part of the effort to divest lower margin, non-core businesses.

Business Segment Overview

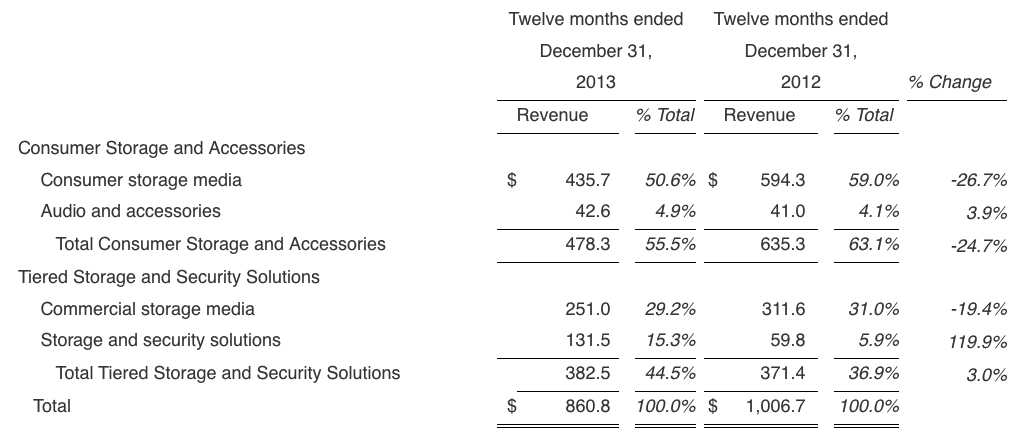

Imation’s Consumer Storage and Accessories (CSA) business revenue decreased 23.0% in Q4 2013 from the prior year, due chiefly to the continued secular declines in optical media products, as noted above. Gross margin remained solid for this segment. Cash generation was particularly strong as a result of improvements in working capital.

According to Lucas, “Our consumer business continues to evolve as the optical market progresses through its life cycle with corresponding revenue declines. Our TDK Life on record audio and accessories business enjoyed strong year over year revenue increases, and we have many new consumer storage products on our roadmap for 2014. While we do not expect CSA to return to revenue growth in the near term, it is expected to continue to be an important contributor of earnings and cash flow to the company.”

Imation’s Tiered Storage and Security Solutions (TSS) business revenue increased 5.4% in Q4 2013 from the prior year, reflecting revenues from the Nexsan acquisition. TSS gross margin rose 4.7 percentage points to 18.2% from 13.5% a year ago, as the product mix moves to higher margin storage and security solutions products. Imation expects this shift in product mix to continue with its focus on Nexsan and IronKey products.

Lucas noted: “In TSS, Imation reported overall revenue and gross margin growth as a result of the Nexsan acquisition. Our magnetic tape business continues to decrease consistent with the overall market, but we have been able to maintain our market share through 2013. The steep revenue decline rates in magnetic tape that we saw through the middle of 2013 leveled off in the fourth quarter. Ongoing emphasis on working capital and cost management will be a key focus in this segment. Within our storage and security solutions portfolio, revenues were constrained by the macro factors that have persisted since the third quarter, such as uncertainty in government spending. We are just now beginning to see improvement in the pipeline for future orders, and longer term we expect robust growth from our storage and security portfolio.”

Lucas concluded: “During 2013, Imation continued to move away from our legacy media businesses to focus on growth categories in both consumer and commercial storage solutions. We also rebalanced our portfolio through the strategic Nexsan acquisition in storage and the divestiture of two lower margin businesses. We continued to right-size our infrastructure, and operating expenses, excluding acquisitions, declined over 30%. We remain committed to our transformation and confident in its ultimate success.“

Detailed Q4 2013 Analysis

As a result of the XtremeMac and Memorex consumer electronics divestitures which occurred on January 31, 2014 and October 15, 2013, respectively, the financial results for those operations are presented as discontinued operations. The following financial results are for continuing operations for the current and prior periods unless otherwise indicated.

Net revenue for Q4 2013 was $232.8 million, down 12.7% from Q4 2012. From a segment perspective, TSS increased 5.4% and CSA declined 23.0 percent. Foreign currency exchange negatively impacted Q4 2013 revenues by 5% when comparing to Q4 2012.

Gross margin for Q4 2013 was 23.8 percent, up 7.7 percentage points from 16.1% in Q4 2012. Gross margin for Q4 2013 includes the reversal of a portion of the company’s European levy accrual of $9.5 million, triggered by a favorable French court ruling received during Q4 2013. While this levy benefit improved gross margin by 4.1% in Q4 2013, the remainder of the improvement was due to operating factors. TSS gross margin for Q4 2013 was 18.2%, up from 13.5% in Q4 2012. CSA gross margin for Q4 2013 was 28.0 percent, up from 18.9% in Q4 2012, benefiting from the aforementioned levy reversal.

Selling, general and administrative (SG&A) expenses in Q4 2013 were $39.5 million, down $6.2 million compared with Q4 2012 expenses of $45.7 million. Imation reduced SG&A expenses by approximately $13.7 million due to cost reduction efforts and lower amortization expense as a result of intangible write-offs in 2012, which more than offset the Nexsan operating expenses added as a result of the acquisition that took place on December 31, 2012.

R&D (R&D) expenses in Q4 2013 were $4.1 million, down slightly from $4.7 million in Q4 2012. The company has reduced legacy R&D spending and has channeled its investments into higher margin projects in TSS, primarily through Nexsan.

Special items netted to $9.5 million of income in Q4 2013 and were primarily related to a $9.8 million gain on the sale of land at a previously closed facility and a $2.5 million gain from a litigation settlement, partially offset by restructuring and other charges. This is compared with special charges of $296.5 million in Q4 2012 primarily consisting of intangible asset and goodwill impairments.

Operating income was $21.1 million in Q4 2013 compared with an operating loss of $301.6 million in Q4 2012. Excluding the impact of special charges described above, adjusted operating income would have been $11.6 million in Q4 2013 compared with adjusted operating loss on the same basis of $5.1 million in Q4 2012.

Income tax provision was $1.9 million in Q4 2013 compared with income tax benefit of $0.1 million in Q4 2012. The company maintains a valuation allowance related to its U.S. deferred tax assets and, therefore, no tax provision or benefit was recorded related to its U.S. results in either period.

Discontinued operations loss for the quarter totaled $2.5 million (after-tax) and included a gain of $0.9 million on the sale of the Memorex consumer electronics business. Discontinued Operations includes both the results of the XtremeMac and Memorex consumer electronics businesses as well as a charge of approximately $1.2 million recorded in Q4 2013 to adjust the carrying value of the XtremeMac assets associated with the discontinued operations, based on proceeds expected to be received for the sale of the businesses.

Earnings per diluted share from continuing operations was $0.47 in Q4 2013 compared with a loss per diluted share of $8.13 in Q4 2012. Excluding the impact of special items, adjusted earnings per diluted share would have been $0.25 in Q4 2013 compared with a loss per diluted share of $0.16 in Q4 2012.

Cash and cash equivalents balance was $132.6 million as of December 31, 2013, up $24 million during the quarter, driven by improvements in working capital and the sale of land at a previously closed facility.

Year-To-Date Summary

For the full year ended December 31, 2013, the company reported net revenue of $860.8 million, down 14.5% compared with 2012, an operating loss of $20.1 million, including special charges of $11.5 million, and a diluted loss per share of $0.60 from continuing operations. Excluding special charges, the operating loss for the year ended December 31, 2013 would have been $8.6 million and diluted loss per share would have been $0.37 from continuing operations. For the year ended December 31, 2012, Imation reported net revenue of $1,006.7 million, an operating loss of $318.4 million, and a diluted loss per share of $8.67 from continuing operations. Excluding special charges, the operating loss for the year ended December 31, 2012 would have been $19.9 million and diluted loss per share would have been $0.70 from continuing operations.

Operating results for the year ended December 31, 2013 include the reversal of accruals of $23.1 million for copyright levies as a result of favorable court rulings in both Italy and France.

Comments

In 5 years, revenue of Imation were divided by two and, for the first time historically, reached under $1 billion in 2013, at only $861 million, even with the addition of Nexsan during the last fiscal year.

Imation's annual revenue from 2006 to 2013

(in $ million)

| Fiscal Year | Revenue | Y/Y growth |

| 2006 | 1,585 | NA |

| 2007 | 2,062 | 30% |

| 2008 | 1,981 | -4% |

| 2009 | 1,650 | -17% |

| 2010 | 1,461 | -11% |

| 2011 | 1,290 | -12% |

| 2012 | 1,007 | -22% |

| 2013 | 861 | -15% |

Imation was a pioneer in computer floppies and tape, at the origin being 3M, but these activities decreased drastically and obliged the spin-off to find new businesses.

It's participation to optical disc industry was a nightmare. It also invests notably in security, RDX removable disk subsystems and in some strange products like audio accessories for audio and Mac smartphones, tablets and computers (XtremMac now divested and Memorex in October 2013). But all together, these new activities were far to compensate its legacy business.

Imation most serious diversification was the acquisition of Nexsan for $120 million just one year ago. The only public most recent figure published on acquired privately-held disk array manufacturer was $82 million revenue in 2011 but Imation didn't reveal if Nexsan was profitable.

What does Nexsan represent for Imation? No revenue for Nexsan only has been published. This activity is integrated into Imation's Tiered Storage and Security Solutions (TSS) that also include small IronKey product business. TSS sales were at $131.5 million in 2013 vs. $59.8 million without Nexsan in 2012. The difference, $73.7 million, then probably represents Nexsan. It's a decrease compared to $82 million two years ago.

TSS business revenue, representing 44% of total sales in 4Q13, increased 5.4% from the prior year, reflecting revenues from the Nexsan acquisition, according to Imation.

We doubt that the addition of Nexsan, with a lot of competitors including all the storage giants and many others, will stop in the short term the continuing loss and decreased revenue of Imation since at least six years. The company didn't give any outlook for the quarter and year.

During the earnings call following 4FQ13, Mark Lucas, president and CEO, confirmed: "We have not yet reached an inflection point in our transformation as sales in our growth products have not yet offset secular revenue decreases in our legacy businesses."

But good news is the recent contract with giant distributor Ingram Micro to resell Nexsan storage subsystems. Imation couldn't count on its own sales force and its traditional channel for products completely different.

Lucas also added: "By the end of 2014, our (Nexsan) sales force will probably be in the neighborhood of 30% larger than it is today."

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter