Marvell: Fiscal 3Q14 Financial Results

Storage grew 3% sequantially, better than expected.

This is a Press Release edited by StorageNewsletter.com on November 22, 2013 at 2:34 pm| (in US$ million) | 3Q13 | 3Q14 | 9 mo. 13 | 9 mo. 14 |

| Revenues | 780.9 | 931.2 | 2,393 | 2,473 |

| Growth | 19% | 3% | ||

| Net income (loss) | 68.8 | 103.2 | 256.4 | 218.2 |

Marvell Technology Group Ltd reported financial results for the third quarter of fiscal year 2014, ended November 2, 2013.

Key 3Q FY2014 Financial Highlights

- Revenue: $931 Million

- GAAP Net Income: $103 Million

- GAAP EPS (diluted): $0.21

- Non-GAAP Net Income: $163 Million

- Non-GAAP EPS (diluted): $0.32

- Free Cash Flow: $157 Million

4Q FY2014 Financial Outlook

Marvell’s financial outlook does not include the potential impact of future share repurchases, pending litigation matters, business combinations, asset acquisitions or other investments that may be completed after November 21, 2013.

- Revenue is expected to be in the range of $880 to $920 Million.

- GAAP Gross Margin is expected to be in the range of 49.7% +/- 100 bps. Non-GAAP Gross Margin is expected to be in the range of 50% +/- 100 bps.

- GAAP Operating Expenses are expected to be in the range of $360 Million +/- $10 Million. Non-GAAP Operating Expenses to be in the range of $315 Million +/- $10 Million.

- GAAP EPS (diluted) expected to be in the range of $0.16 +/- $0.02. Non-GAAP EPS (diluted) expected to be in the range of $0.25 +/- $0.02.

3Q FY2014 Summary

Revenue for the third quarter of fiscal 2014 was $931 million, a 15% sequential increase from $807 million in the second quarter of fiscal 2014, ended August 3, 2013, and a 19% increase from revenue of $781 million in the third quarter of fiscal 2013, ended October 27, 2012.

GAAP net income for the third quarter of fiscal 2014 was $103 million, or $0.21 per share (diluted), compared with GAAP net income of $62 million, or $0.12 per share (diluted), for the second quarter of fiscal 2014, and $69 million, or $0.12 per share (diluted), for the third quarter of fiscal 2013.

Non-GAAP net income was $163 million, or $0.32 per share (diluted), for the third quarter of fiscal 2014, compared with non-GAAP net income of $118 million, or $0.23 per share (diluted), for the second quarter of fiscal 2014, and $113 million, or $0.20 per share (diluted), for the third quarter of fiscal 2013.

“Our results in the third quarter were above the high-end of our guidance mainly due to better demand from our mobile, wireless and storage customers,” said Dr. Sehat Sutardja, Marvell’s chairman and CEO. “We continue to make excellent progress in our end markets with new innovative products and remain committed to delivering above industry revenue and profit growth as we head into next year.”

GAAP gross margin for the third quarter of fiscal 2014 was 50.1%, compared to 52.2% for the second quarter of fiscal 2014 and 52% for the third quarter of fiscal 2013.

Non-GAAP gross margin for the third quarter of fiscal 2014 was 50.3%, compared to 53.0% for the second quarter of fiscal 2014 and 52.3% for the third quarter of fiscal 2013.

Shares used to compute GAAP net income per diluted share for the third quarter of fiscal 2014 were 501 million shares, compared with 501 million shares in the second quarter of fiscal 2014 and 559 million shares in the third quarter of fiscal 2013. Shares used to compute non-GAAP net income per diluted share for the third quarter of fiscal 2014 were 514 million shares, compared with 516 million shares for the second quarter of fiscal 2014 and 578 million shares for the third quarter of fiscal 2013. The decrease in shares used to compute both Marvell’s GAAP and non-GAAP net income per diluted share was primarily due to Marvell’s share repurchase program.

Cash flow from operations for the third quarter of fiscal 2014 was $177 million, compared to the $86 million reported in the second quarter of fiscal 2014 and the $137 million reported in the third quarter of fiscal 2013. Free cash flow for the third quarter of fiscal 2014 was $157 million, compared to the $65 million reported in the second quarter of fiscal 2014 and the $113 million reported in the third quarter of fiscal 2013. Free cash flow as presented above is defined as cash flow from operations, less capital expenditures and purchases of technology licenses reported under investing and financing activities in the consolidated statement of cash flows.

Under the share repurchase program, Marvell repurchased approximately 6.1 million shares for a total of $71 million in the third quarter of fiscal 2014. Over the past 13 quarters, Marvell has repurchased and retired approximately 217 million shares, or about 31% of its outstanding shares.

Marvell also paid a quarterly dividend of $0.06 per share on October 3, 2013 to all shareholders of record as of September 12, 2013. Marvell intends to pay its next quarterly dividend of $0.06 per share on December 23, 2013 to all shareholders of record as of December 12, 2013. Developments in on-going litigation could affect Marvell’s ability to pay the dividend on December 23, 2013 under Bermuda law, where Marvell is incorporated. In such an event, the dividend payment could be delayed until such time as Marvell can meet statutory requirements under Bermuda law

Comments

End Markets: Storage

Abstracts the earnings call transcript:

Sehat Sutardja, chairman and CEO:

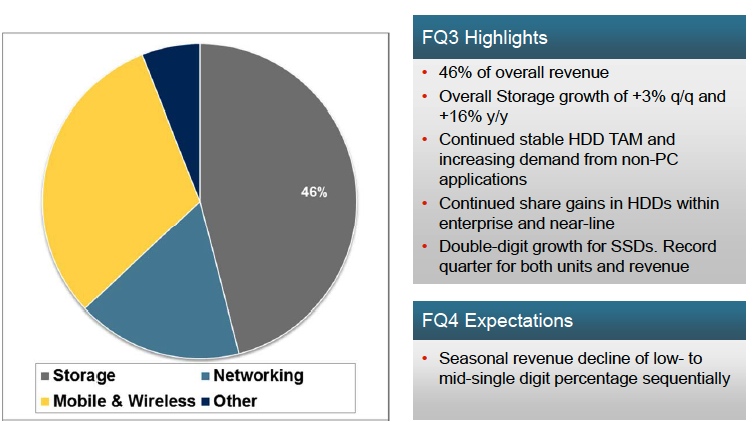

"In storage, we continue to execute well despite a tepid year end - tepid PC end market. For Q3, revenue from our storage and market was better than initially expected and grew 3% sequentially. Starting with HDDs, we continue to outperform due to share gains and increased demand from our customers. As many of our HDD customers have indicated publicly, the overall drive industry seems to have stabilized. We believe our customers are seeing good demand for non-PC applications, which is offsetting weakness in the traditional PC market.

"In the enterprise space, we continue to see steady share gains at a top-notch America-based HDD customer. In Q3, our enterprise drive shipments to this customer grew by over 20% sequentially. And we do expect continued traction and share gains in the enterprise device heading into calendar 2014. In addition, we are making some progress in gaining new design wins for traditional 3.5-inch desktop and nearline applications.

"Next in SSDs. Q3 was a record quarter for both units and revenue, and we delivered another quarter of strong double-digit sequential growth. Our PCI-E-based SSD solutions are now in mass production, and we have a significant lead in the market. We are also shipping our fourth generation SATA SSD products in production and multiple top-tier NAND OEMs. Furthermore, we are winning designs for our next-generation SSD solutions across a broad-based - customer base and believe this will further increase our leadership position. As a result, we expect our SSD business to, once again, grow strongly in the next fiscal year.

"We are also well positioned for the hybrid market and should benefit when the market starts to grow. Specifically for hybrids, we are leveraging our technology leadership in HDDs and SSDs, we have a single-chip solution that should drive lower price points. This is an important driver for market adoption. For Q4, we expect our storage end market to seasonally decline low- to mid-single digit percentage points."

Brad Feller, interim CFO:

"The growth in storage is mainly due to a combination of steady share gains and increased demand in our customers in anticipation of the holiday season. Storage represented 46% of overall sales in the quarter."

Abstracts the earnings call transcript:

Sehat Sutardja, chairman and CEO:

"In storage, we continue to execute well despite a tepid year end - tepid PC end market. For Q3, revenue from our storage and market was better than initially expected and grew 3% sequentially. Starting with HDDs, we continue to outperform due to share gains and increased demand from our customers. As many of our HDD customers have indicated publicly, the overall drive industry seems to have stabilized. We believe our customers are seeing good demand for non-PC applications, which is offsetting weakness in the traditional PC market.

"In the enterprise space, we continue to see steady share gains at a top-notch America-based HDD customer. In Q3, our enterprise drive shipments to this customer grew by over 20% sequentially. And we do expect continued traction and share gains in the enterprise device heading into calendar 2014. In addition, we are making some progress in gaining new design wins for traditional 3.5-inch desktop and nearline applications.

"Next in SSDs. Q3 was a record quarter for both units and revenue, and we delivered another quarter of strong double-digit sequential growth. Our PCI-E-based SSD solutions are now in mass production, and we have a significant lead in the market. We are also shipping our fourth generation SATA SSD products in production and multiple top-tier NAND OEMs. Furthermore, we are winning designs for our next-generation SSD solutions across a broad-based - customer base and believe this will further increase our leadership position. As a result, we expect our SSD business to, once again, grow strongly in the next fiscal year.

"We are also well positioned for the hybrid market and should benefit when the market starts to grow. Specifically for hybrids, we are leveraging our technology leadership in HDDs and SSDs, we have a single-chip solution that should drive lower price points. This is an important driver for market adoption. For Q4, we expect our storage end market to seasonally decline low- to mid-single digit percentage points."

Brad Feller, interim CFO:

"The growth in storage is mainly due to a combination of steady share gains and increased demand in our customers in anticipation of the holiday season. Storage represented 46% of overall sales in the quarter."

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter