WW Personal and Entry Level Storage Shipments Grew 13.6% Y/Y – IDC

And 6.2% to $6.7 billion in value from 2012 to 2013

This is a Press Release edited by StorageNewsletter.com on February 18, 2014 at 3:14 pmWorldwide personal and entry-level storage (PELS) shipments grew 13.6% year over year in 2013, finishing the year with 75.2 million units, according to the International Data Corporation‘s Worldwide Personal and Entry Level Storage Tracker.

Annual shipment values were up year over year, growing 6.2% to $6.7 billion. Unit shipments were down slightly in 4Q13, declining -4.2% year over year to 20.4 million units while 4Q13 shipment values were also down year over year, declining -10.3% to $1.8 billion.

“The personal and entry-level storage market finished 2013 strong even with the difficult comparison with a strong second half from a year ago,” said Liz Conner, research manager, storage systems. “In 2012, the fourth quarter showed exceptionally strong growth as the PELS market was in full recovery mode after the Thailand floods, which led to HDD shortages. Despite the resulting slight decline in 4Q13, the PELS market was able post year-over-year growth for all of 2013. This continued annual growth is driven by on-going consumer education, better marketing by vendors, and progressing product evolution to address items such as higher capacity, faster transfer speeds, and mobile device integration.“

HDD vendors continue to increase share in PELS units shipped, gaining 6.6 points year over year to grow to 76.9% market share. However the entry-level storage market continues to be dominated by the mainstream non-HDD vendors with 60.6% unit shipment market share, down 11.9 points year over year.

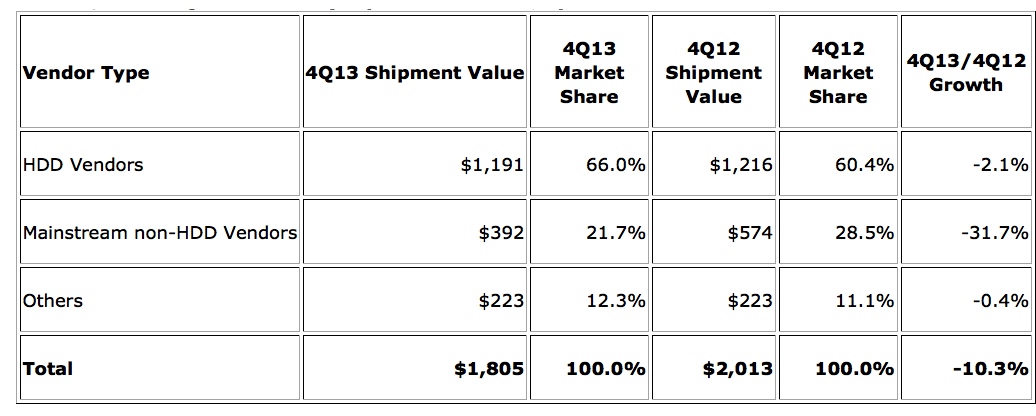

WW Personal and Entry-Level Storage Shipment Value, Market Share, and Y/Y Growth, 4Q13

(shipment value in $ million)

(Source: IDC Worldwide Quarterly Personal and Entry Level Storage Tracker, February 2014)

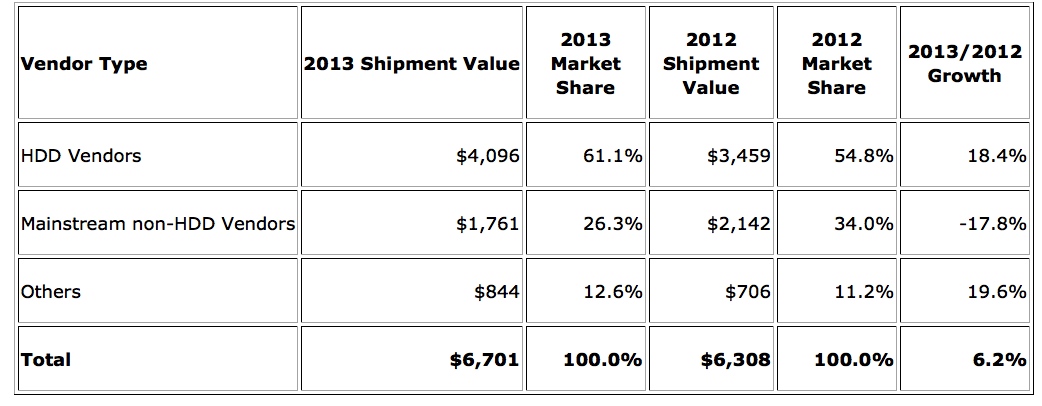

WW Personal and Entry-Level Storage Shipment Value, Market Share, and Y/Y Growth, 2013

(shipment value in $ million)

(Source: IDC Worldwide Quarterly Personal and Entry Level Storage Tracker, February 2014)

Market Highlights

- The entry-level storage market experienced a growth in unit shipments, gaining 6.8% year over year, based primarily on the 4-bay market, which acts as an easy entry point for vendors to introduce an entry level product. The entry-level market saw unit shipments for the higher bay devices (6, 8, and 12 bays) remain flat with 0.7% year-over-year growth.

- In 4Q13 the personal storage market saw continued decline in growth for dual-bay products, where unit shipments were down -32.2% year over year. Single-bay personal storage devices remain the most popular choice, representing 98.0% of the personal storage units shipped in 4Q13.

- Personal storage represents 98.8% of the PELS units shipped and 86.9% of the shipment value in 4Q13.

Technology Highlights

- Form Factor – The 3.5″ form factor saw a decline of -18.8% year over year in units shipped, while the 2.5″ form factor saw units shipped remained flat, growing 0.8% year over year. The 3.5″ form factor continues to give way to the more portable 2.5″ form factor, with 3.5″ losing 3.9 percentage points year over year.

- Capacity Range – End users continue to migrate to higher capacity points to meet storage needs. In the 3.5″ personal storage market, 2TB devices represented 48.3% of unit shipments in the quarter. For the 2.5″ personal storage market, 1TB devices captured 58.2% market share. For the entry-level market, capacity ranges are more varied due to multiple bays and vendors’ ability to partially populate devices. However, 4TB devices hold the most market share with 28.2% of units shipped.

- Interface – USB continues to be the interface of choice for the PELS market, with 93.3% market share. Ethernet remains the interface of choice for the entry-level market, capturing 95.1% market share. Thunderbolt continues to ramp up, posting a year-over-year shipment growth rate of 282.8%, albeit off a small base.

Notes:

- The PELS market includes storage products and solutions with a single bay through twelve bay configurations that are manufactured and marketed for individuals, small offices/home offices, and small businesses.

- IDC defines personal storage as having 1-2 bays and entry-level Storage as having 3-12 bays.

- IDC defines an HDD vendor as a vendor who manufactures their own HDD drive, in addition to branded external storage.

- IDC defines a mainstream non-HDD vendor as a major PELS vendor who does not manufacture its own HDD drives.

- Data for the PELS market is reported for calendar periods.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter